1. Company Background

FIBON Bhd is

principally engaged in the business of investment holding.The principal

activities are the formulation, manufacturing and sales of polymer

matrix fiber composite materials and products for the Electrical,

Electronic, Petrochemical and Automotive industries.

It deals in manufacturing and sales of electrical insulators, electrical enclosures and meter boards. Fibon bhd is based in Johor Darul Takzim, Malaysia.

It deals in manufacturing and sales of electrical insulators, electrical enclosures and meter boards. Fibon bhd is based in Johor Darul Takzim, Malaysia.

2. Financial Performance

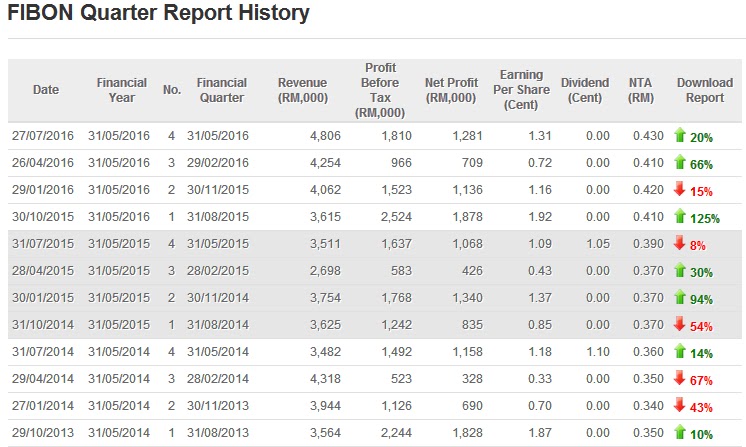

In the current

quarter ended 31 May 2016, the Group registered higher revenue of

RM4,806,000 compared to previous corresponding quarter ended 31 May 2015

of RM3,511,000 as a result of both increase in manufacturing and

trading sales.

Profit before tax has increased from RM1,611,000 to RM1,810,000 as a

result of higher sales and higher other income. Last 6 Quarters have

registered steady revenue increment with potential higher coming high dividend.

Despite facing various general economic challenges, the Board of

Directors of Fibon Berhad is of the opinion that the performance of the

Group for the financial year ending 31 May 2017 will not be severely

affected.

3. Basic FA

Fibon has a healthy balance sheet since listing. It

never had to borrow any money as there is adequate amount of free cash

flow every year. Total equity attributed to shareholders has been

increasing every year . Its cash holding also increases every year.

In recent quarter, the cash holding is RM28.26 Million or around half of market capitalization. If we exclude the cash holding, the adjusted PE will be 5.87 instead of current 11.65. The business quality is undeniably good with net profit margin at 31%.

At the price of 59.5 sen, the adjusted PE ratio is 5.87 and Enterprise value/ EBIT is trading below 5 (which is very attractive). This may be due to its small market capitalization and hence not a liquid stock. There are also not much analysts covering this company.

In recent quarter, the cash holding is RM28.26 Million or around half of market capitalization. If we exclude the cash holding, the adjusted PE will be 5.87 instead of current 11.65. The business quality is undeniably good with net profit margin at 31%.

At the price of 59.5 sen, the adjusted PE ratio is 5.87 and Enterprise value/ EBIT is trading below 5 (which is very attractive). This may be due to its small market capitalization and hence not a liquid stock. There are also not much analysts covering this company.

EPS : 5.11

NTA :0.43

PE : 11.65

ROE :12.08

Net income margin: 31%

M.Capitalization: RM58M

EBIT : 6.8M

Deposit/cash : 28.26M

Short term bank borrowing: 0

T.Asset : RM44.3M

T.Liability: RM2.57

T. Equity :RM41.8

Current Ratio: 25.72

DY:1.65%

EV: 29.7

Current Ratio: 25.72

DY:1.65%

EV: 29.7

4. Basic TA

For above chart, the trading price for Fibon is close to upper band which shows buyer's interest is relatively strong. Parabolic indicator also shows Fibon on uptrending trend with strong Force Index to reinforce bullish trend.

In conclusion, Fibon is just on early up-trending phase and there is likely further upside for its share price.

5. Catalyst

Electricity Demand is Growing

According to market research firm NRG Expert, the demand of electricity is growing, hence demand for cables, insulators, transmission towers will also be growing with it. The increase in the global energy demand are encouraging the demand for electrical insulator for power transmission and distribution application. The electrical insulator market is projected to grow at a CAGR of 6.5% in between 2014 to 2019.

On the local outlook, the massive development in Johor, ranging from property to massive industrial development continue to push the demand in building related components, such as cabling, piping, insulation and wiring.

With Fibon stationed at Johor, it will stand to benefit from all these massive development. Continuation of infrastructure upgrade in Singapore will also continue to benefit Fibon.

For recent news, FIBON Group has decided to expand into the service sector (acquisition of BEEPS), as a service platform for the exports of unregistered used vehicles from Japan to the worldwide market.

6. Ownership Summary

For ownership summary, we can note that insider tightly controls 83% of total share and public shareholding less than 10%. One may wonder on why not much funds are interested in investing in Fibon? Small cap with low liquidity probably?

7. Valuation:

Based on EV/EBIT=8 projection: FV= RM0.85

(Projection is based on 10% minimum growth)

|

(22.5*EPS*Book value per share)^0.5 :RM 0.7 TP: RM0.78 ( from above average) |

8. Strategy

Based on current price (30 July 2016),

Entry :RM0.595

TP :RM0.78

Stop loss : Below RM0.55 (with high volume)

Potential gain : 44%

Potential loss : 7.6%

Kindly like our FB page if you find above information useful at,

Related article,

Kcchong on FIbon

http://klse.i3investor.com/blogs/stock_pick_challenge_2013_2h/34374.jsp

Disclaimer: This is a personal weblog, reflecting my personal views and not the views of anyone or any organization, which I may be affiliated to. All information provided here, including recommendations (if any), should be treated for informational purposes only. The author should not be held liable for any informational errors, incompleteness, or delays, or for any actions taken in reliance on information contained herein.

FIBON (0149) - FIBON Berhad- A neglected quality counter

http://klse.i3investor.com/blogs/walau2u/101029.jsp