As predicted previously, Petron Malaysia Refining & Marketing delivered superior financial performance for its 3QFY2017.

Let us explore key factors to assess whether Petron can continue to do well in 4QFY2017.

1) Surge in Brent Crude Oil Price

Year 2017:

Jan - $53.59

Feb - $54.35

Mar - $50.90

1QFY17 Profits: rm108.54m

Apr - $52.16

May - $49.89

Jun - $46.17

2QFY17 Profits: rm90.99m (rm39m gains on disposal of service stations for MRT development)

Jul - $47.66 (FY16: $44.13); Difference: $3.53

Aug - $49.94 (FY16: $44.87); Difference: $5.07

Sep - $52.95 (FY16: 45.04); Difference: $7.91

3QFY17 Profits: rm106.07m

Oct - $54.92 (FY16: $49.29); Difference: $5.63

Nov - $59.93 (FY16: $45.26); Difference: $14.67

Dec - $??.?? (FY16: $52.62); Difference: $???

4QFY17 Profits: rm??.??m

As there is some correlation of Petron's profits to crude oil prices,it is key to monitor its movement. Brent Crude Oil has settled above $50 / barrel for October and November. We would need to monitor Brent Crude Oil price movement for the remaining days of December to have a better overall picture. Time will tell. So far it is settling above $60 / barrel, with OPEC / NON-OPEC extending its production cuts deal till December 2018 with the inclusion of Libya & Nigeria, the risk of a surprise build up in supply is reduced. Let us hope Brent Crude can settle above $60 / barrel for the rest of December.

If u take notice, you will realize the Brent Crude difference (Q4FY17 vs Q4FY16) is actually much larger for Q4FY17, compared to Q4FY16.

2) Surge in Brent Crack Spread

Product cracks continue to improve, holding steady above $9 / barrel in November ($5 to $6.50: Q4FY16). I am aware there are many other crack spread to refer, but I would just use this as a reference. Please conduct your own due diligence.

3) Sales Volume

2016:

Q1 - 8.2 million barrels

Q2 - 7.8 million barrels

Q3 - 7.8 million barrels

Q4 - 8.3 million barrels

2017:

Q1 - 8.3 million barrels

Q2 - 8.5 million barrels

Q3 - 9.0 million barrels

Q4 - ?.? million barrels

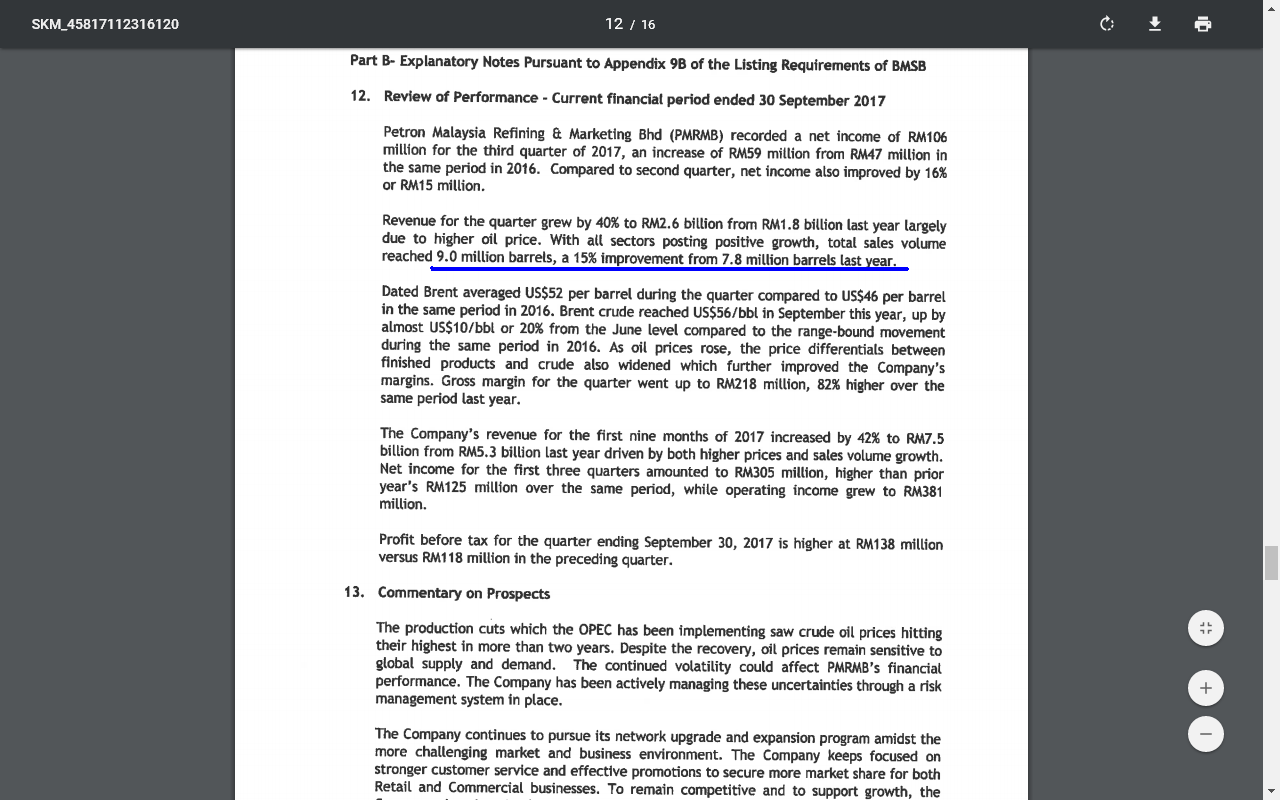

In Petron's 3QFY17 report, the company registered 9.0 million barrels of total sales volume, a 15% improvement from previous corresponding period. I am of the view that Petron will continue to register higher total sales volume in coming period. For Q4FY17, Petron Malaysia is expected to register sales volume of 9.0 million barrels or above, beating Q4FY16 sales volume of 8.3 million barrels.

4) Healthy Cash Level

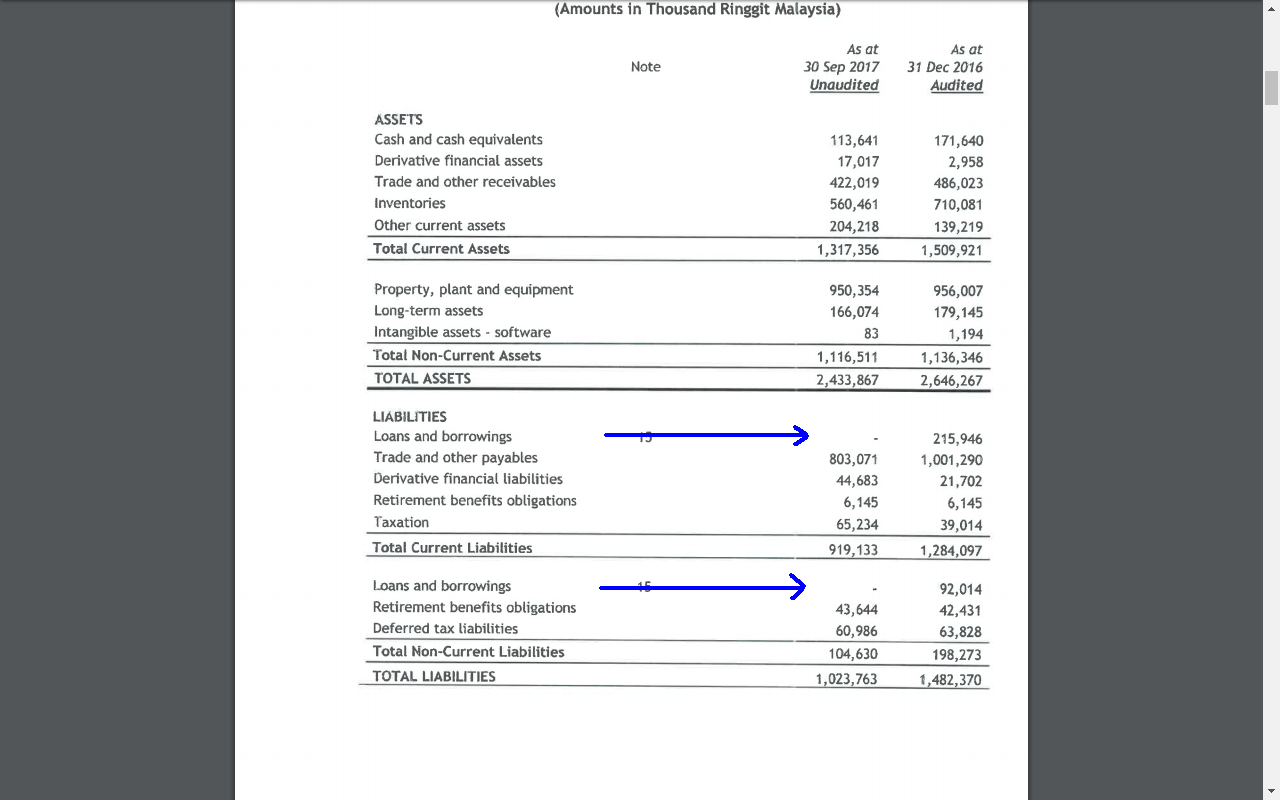

As of Q3FY17 financial report, Petron Malaysia has a healthy cash level of RM113 million (RM0.42 per share). What is amazing is, the company is able to CLEAR OFF all of its debts. It is now a DEBT FREE company. Petron has a net cash position of RM113 million.

Do take notice of its cash and debt level at 31 December 2016, it has a cash level of RM172 million, while its total debts amount to RM308 million, contributing to a net debt position of RM136 million.

In just 9 months, it has improved from a net debt position of RM136 million, to a net cash position of RM113 million, a DEBT FREE company with strong free cash flow (FCF). It is not surprising if Petron Malaysia can have a net cash position of RM200 million by 31 December 2017, with over RM250 million to RM300 million cash level, sufficient to undertake any major plant upgrades and expansion, via internally-generated funds.

5) Valuations:

If Petron Malaysia could record rm130 million net profits for its 4QFY17 (rm112m, 4QFY16), its immediate 4 rolling quarters Earnings Per Share (EPS) would stand at rm1.61. With a Price Earnings Multiple of 8.5x (conservative estimate), Petron Malaysia should be trading at rm13.71. From current price of rm11.90, there is 15% upside for this stock.

A number of research centres gave a higher PE of 11 to 12.5x for Petron Malaysia, I would stick to PE of 8.5x. Any re-rating would be a further boost to the company, and could trade above current target price of RM13.71

Any downside risk would be the fall in crude oil prices, product cracks and mishaps / maintenance shutdown in its refinery plant in Port Dickson. Further downside risks would be a deep surge in US Oil Production that would flood the market with crude oil supply.

On a another note, Petronas Dagangan produced good financial result, netting rm761m in net profits for its 3QFY2017, y-o-y jump of 206%. In addition, Heng Yuan Refining also perform well for its 3QFY2017 result, with rm361m profits, y-o-y jump of 547%. I would like to congratulate Petronas Dagangan, Petron Malaysia Refining & Marketing & Hengyuan Refining company shareholders. May all of us end the year 2017 well.

Note: Please "LIKE" this page in Facebook ("Financial Education for Youth"), to support! https://www.facebook.com/financialeducation4youth/

Disclaimer: The above is for educational purposes only, please conduct your own due diligence before buying / selling a stock.

http://klse.i3investor.com/blogs/investmentopportunity/139148.jsp