2QFY18Quarterly Result at a glance.

- Market Capitalization: RM752.3m, PE 7.3, DY 2.6%, NTA RM0.99

- TTM Earnings +2.3%, Revenue -18.5%

- Earnings YoY +1.7% , QoQ +54.7%, EPS 4.3 sen

- Revenue YoY -3.4%, QoQ +22.4%

Key Highlights

1. Pre-tax profit margin for current quarter is 26.8%, up from 24.4% YoY.

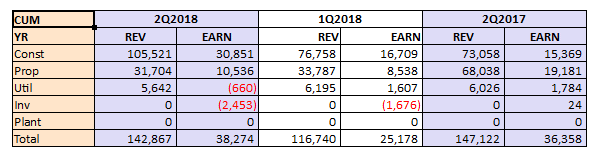

2. Construction revenue rebounds 44.4% YoY and 37.5% QoQ, indicating reacceleration of construction segment after a few soft quarter due to gap between projects completion and new projects

3. Importantly, construction pretax margin is 29.2% for the quarter which compares favorably with 21.7% in 1Q2018 and 21.0% in 2Q2017. This is despite an operating environment where cost pressures due to rising labour costs, energy and raw materials are cited repeatedly by peers for margin contraction.

4. YTD, Free Cash Flow (FCF) reduced to -RM29.2m. Negative cash flow was due to accelerated spending of RM75.9m to bulk up the utility segment.

5. Debt /Equity ratio increased to ~5.0% from a net cash position of RM9.9m in 2QFY17.

6. There will be no more loss from the plantation division after disposal of palm oil plantation at a loss of RM1.6m

Outlook

1. Moving forward, RAPID package 301/402 are expected to complete by June 2018 and future revenue streams will be mainly from MRT2, TRX project and Cyberjaya Hospital. Book order to date is RM1.62b, which is roughly 3.8 year based on current quarter’s runrate

2. Management remarked in Nov 17 AGM that there is a balance of RM260m to be recognized from Capital 21 (to be opened in Aug 2018) for the next 2 years. Of which majority of RM260m should be profit given that the only contribution by Gadang to the JV is the land which is valued at ~RM30m and all other expenses will be borne by JV’s partner. Only a meagre RM10.5m is recognized from Property Segment in 2Q2018, meaning the bulk of profit still waiting to be recognized within the next 2 quarters.

3. On the flip side, current recurring income is negligible compare to up to 50% by Gamuda. In long run, recurring income is critical to counter the cyclical nature of Construction and Property segment, which is precisely what the management is doing as seen in Key Highlight (4) above.

Moving forward, 2H2018 earning are expected to remain buoyant with the construction segment's profit to pick up in tandem with re-acceleration of the consruction revenue and the property segment's outsized profit from Capital 21, which will more than offset any slowdown in property sector. A bullish outlook supported by a huge order book, a brilliant execution as displayed in superior cost control and timely delivery, a forward-thinking management as evidenced in the long-term counter cyclical strategy in place and a TTM PE of 7.3 only. Guess which one is out of place?

Disclaimer:

A sharing of personal investment idea and thought and is not a recommendation to buy or sell.

http://klse.i3investor.com/blogs/20102017/145303.jsp

http://klse.i3investor.com/blogs/20102017/145303.jsp