Inventory and Factory outlook

Since I am going to talk about oil Inventory, let us first have a look at this Google satellite image below which gives a good overview on the facilities or storage capacity of Hengyuan in Port Dickson, N. Sembilan.

Source: Google map

From the above image, we can see that HY plant has many storage tanks ranging from giants (having thousands of oil barrel storage capacity), medium tanks and smaller sizes of tanks (more than 100 units from my calculations).

These tanks are important for HY to store crude oils and refined product. Current inventory of HY is valued at RM 1.263 Billion consisting of their crude feed oil and refined products which are stored in these tanks. All these tanks and pipes (pipes too small to be seen from Google photo unless you zoom in to max) are super expensive to build nowadays not even bringing the cost of the Plant & Machinery, i.e the Refinery Complex consisting of Distillation Units and Catalytic Crackers (will share more on this on my next section on Petronm new upgrade project)

Why inventory and storage are important? Huge inventory (especially refined products) can serve as buffer when HY undergo shut down in Q3’2018 or make sure sales of their products to Shell Malaysia as sustained as usual during minor unplanned shut down. Actually we can observe that HY slowly raise their inventory level in the past 3 quarters.

Another advantage of huge inventory during crude oil uptrend time is it can book considerable inventory gain. Let us go through recent Brent oil price, Mogas 95 and Diesel price charts as below to know the possible inventory gain and profit margin as below:

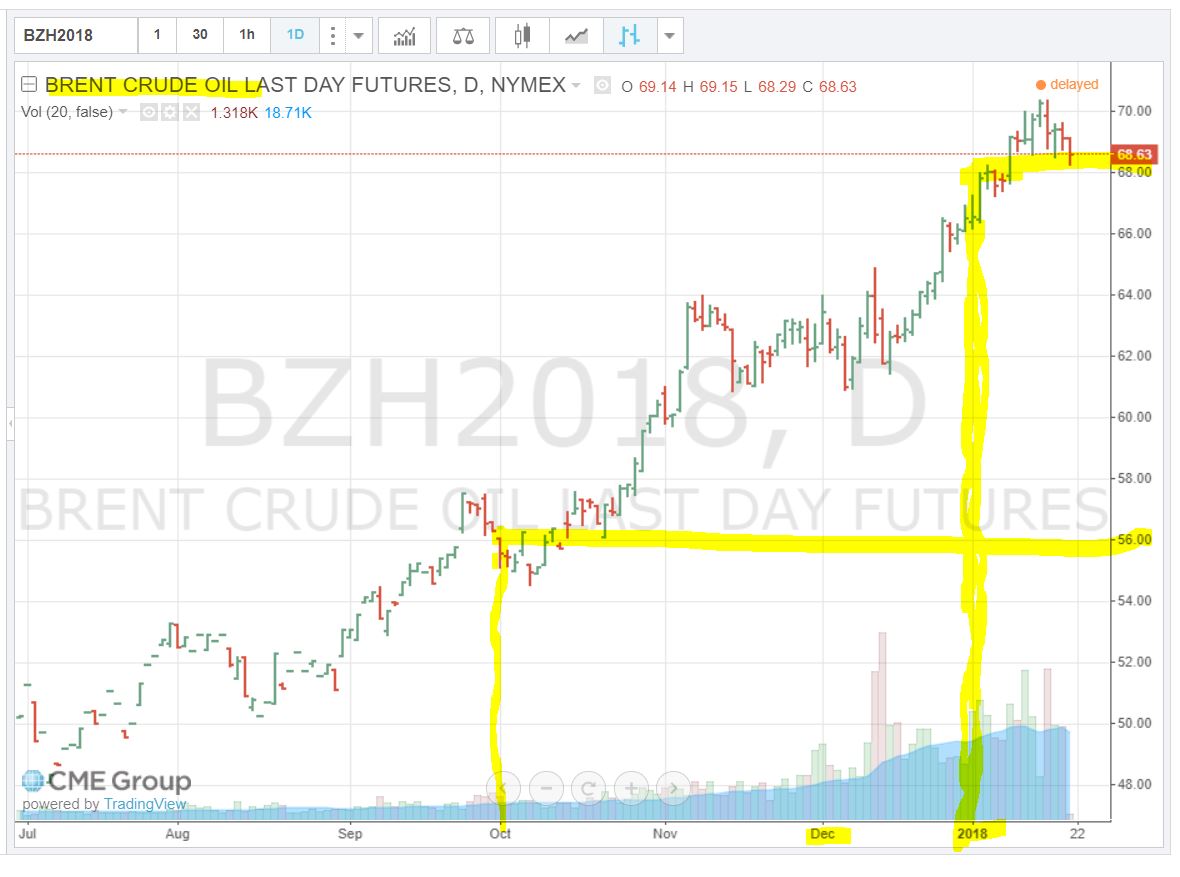

Chart 1 : Brent oil (Souce: CME website)

Chart 1 : Brent oil (Souce: CME website)

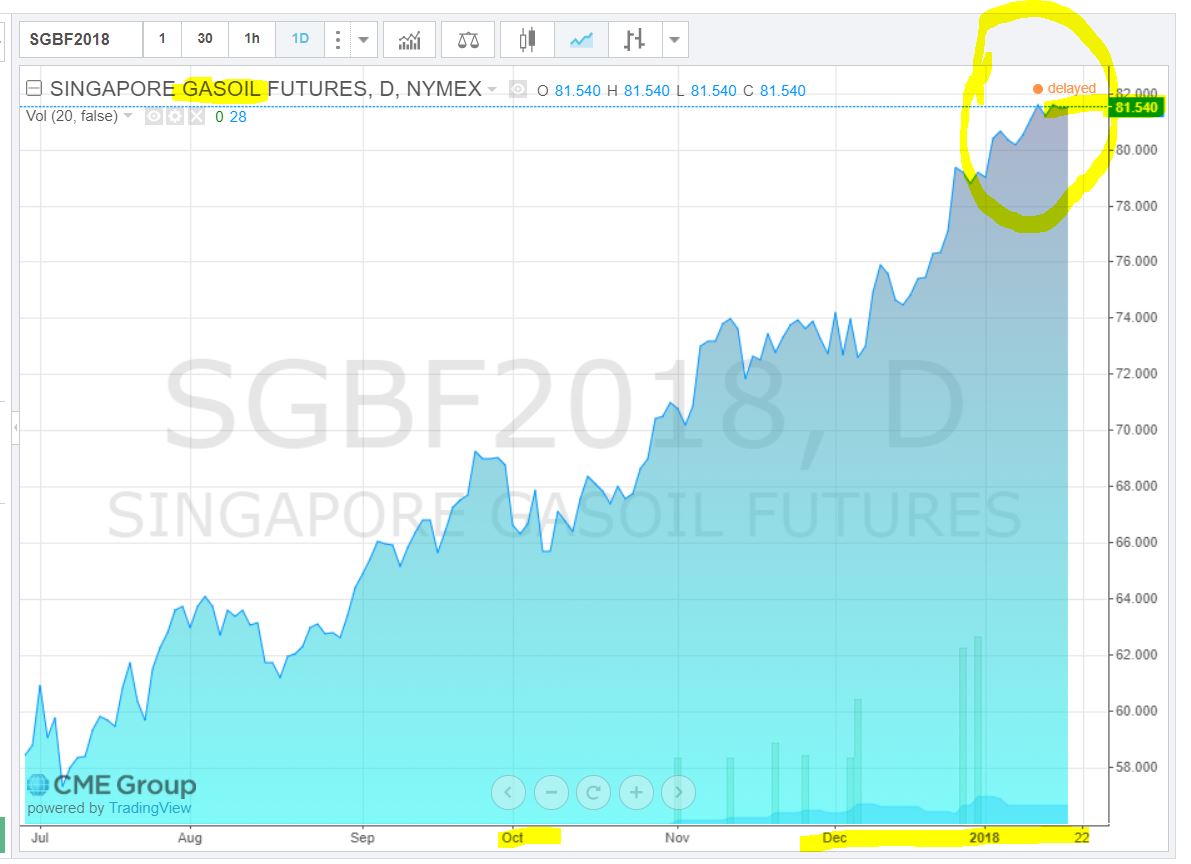

Chart 2 : Diesel = Gasoil (Souce: CME website)

Chart 2 : Diesel = Gasoil (Souce: CME website)

Chart 3 : Mogas 95 = petrol (Souce: CME website)

Crude oil theoretical Inventory Gain = [67 (30 Dec price) – 56 (30 Sept price) ] /3 = USD3.7 per barrel.

I divide inventory gain by 3 is based on backward calculation of past record of USD1.67 inventory gain as per Q3 report.

HY keep around 3.5 million barrels crude oil (info form hrc.com.my).

Estimated inventory gain from Crude oil = 3.5M X 3.7 X 4 = RM51.8 mil

Their refined products inventory gain maybe include in the sales to its customer. For example, their old stock of inventory cost of refined products maybe USD65 (due to that time crude is cheaper), their selling price in Dec may reach USD78, as a result, HY may enjoy USD12 profit margin per barrel. This is called First-in-First out.

Q4’17 and Q1’18 profit margin

Two main products of HY are Diesel (Gasoil) and Gasoline (Mogas 95) which constitute about 80% of the revenue.

Refer chart below:

Typical yield as per below:

Typical yield as per below:

Diesel = 43%

Kerosene, LPG and others = 21%

Petrol (Mogas95) = 36%

Diesel product gross profit margin is obtained from subtraction of daily data of chart no 1 by chart no 2 as below:

Diesel Crack spread (margin) = Diesel selling price (chart 2) – Brent oil price (chart 1) [Eg. 81.56 – 69.3]

Mogas 95 product gross profit margin is obtained from subtraction of daily data of chart no 1 by chart no 3 as below:

Mogas 95 Crack spread (margin) = Mogas 95 selling price – Brent oil price

Average Mogas 95, jet fuel and diesel spread in Q4’2017 based on my previous article is around USD11.2. (https://klse.i3investor.com/blogs/davidtslim/143634.jsp). If we include LPG, Naphtha, propylene, fuel oil, average crack spread or profit margin per barrel maybe around USD9.5 - USD10

(Note: As per their respective yields, its average refining margin is much higher. However, for conservative reasons I am not using these values.)

As far as I survey from online, most of the refinery plants running on 24 X 7 days (including holiday).

Let us calculate how much gross profit (GP) per day for HY based on USD9.5 average crack spread

GP = USD9.5 X 4 X 112k = RM4.26 mil per day

Q4 contain 92 days. Let assume 2 days down time in Q4, then

GP = RM4.26 mil X 90 days = RM383 mil

Total gross profit = 383 + 51.8 mil = RM435.2

Estimated admin cost, depreciation, manufacturing expenses and Finance cost = 127 mil (based on Q3 figure)

There is high possibility of forex gain and small amount of other income in Q4 (as per Q3 report)

Let assume similar forex gain as per Q3 forex gain (50 mil as RM actually strengthen in Q4 more than Q3), and same other income of 9 mil.

Estimated Net income before tax in Q4 = 435.2 – 127 +50 + 9 = 367 mil.

Profit before tax of RM367 mil translated to EPS of 122.6 sen in Q4.

Some of you may worry of Q1’18 Mogas 95 spread is dropping. But HY main product consist of Diesel which has relative higher spread (range from USD11 to 12++) in past 15 days of Jan 2018. This actually can compensate the drop in Mogas 95 spread which lead the average spread of these two products is still more than USD10 based on my data collected.

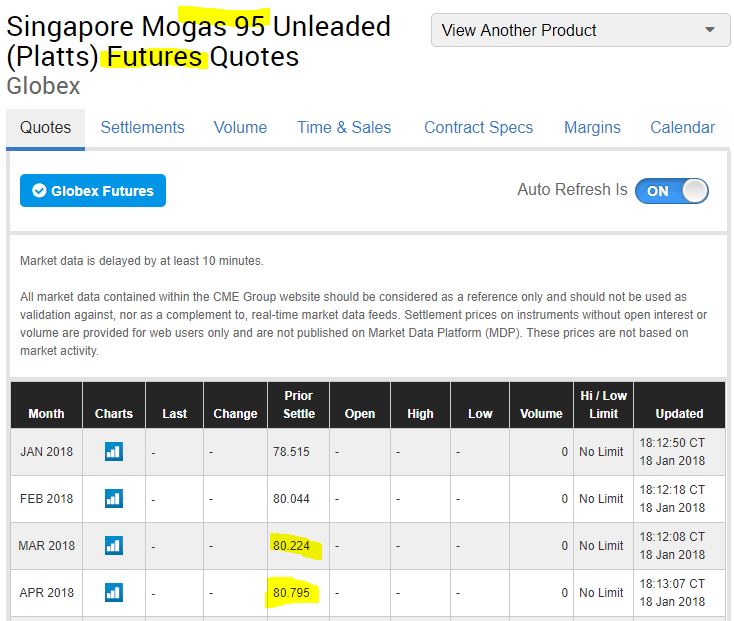

Still worry about Mogas 95 spread in Q1'18? Let us go through the future crack spread data of Mogas 95 in Feb, Mar and April as below:

Source: CME website

The future contract of Mogas 95 is trading at USD80.04 (feb) to 80.795 (April). The higher selling price of Mogas 95 may due to ending of winter season in March which the demands of gasoline is anticipated to be higher in Spring season (higher travelling). If you checked the future data of Brent oil in CME (Mar and April), brent oil is trading at USD69 – 68++ which indicate the Mogas 95 spread at that time may increase to a level of USD10++.

Cost of new refinery upgrade and Simple Valuation

As highlighted in my HY part 6 article, oil refinery is a capital-intensive business. Planning, designing, permitting and building a new medium-sized refinery is a 2-5 year process.

Let see how much the budget for coming Petronm refinery upgrade as per news below:

https://businessmirror.com.ph/petron-refinery-expansion-seen-completed-by-2020/

Let me summarize the cost for building new and upgrade exiting refineries in Asia and South East Asia as table below

Average cost for building new refinery (Petron Corp Philippines)

= (8+14 billion / (90) kbpd

= RM0.16 billion or RM160 mil per 1kbpd

Average cost for upgrade existing refinery (Petronm)

= 14 billion / 90 kbpd

= RM0.16 billion or RM160 mil per 1kbpd

HY current market cap is RM4.29 billion. If we calculate its valuation for its kilo barrel per day (kbpd):

Market Valuation of 1 kilo barrel capacity of HY (based on HY current whole market capital on 19 Jan, RM14.30 per share price)

= 4290mil / 125 = RM34.32 mil for every 1kbpd.

Let see another news on Saudi Arabia possible investment in China refinery plant as below:

https://oilprice.com/Latest-Energy-News/World-News/Saudi-Aramco-In-Talks-To-Buy-2B-Stake-In-PetroChina-Refinery.html

Aramco (one of the world biggest oil companies) willing to pay USD2 billion for 30% stake of 260 kbpd refinery plant in china (normally can be built at lower cost than other countries using China technology).

30% of 260 kbpd is 78kbpd. USD2 billion = RM8 billion for a new refinery plant in China.

Hengyuan current market capital is RM4.29 billion (based on current price of RM14.30) for a rated capacity of 125k bpd.

The beauty of HY refinery is it is a complex refinery with possible earning capability of RM1 billion per year (base on 2017 spread, HY has earned 752 mil in 3 quarters of 2017).

Free cash flow also strong in 2017 (predicted can be maintained in Q1 and Q2 of 2018) which currently they has level of cash in hand of RM898 mil as per 30 Sept 2017. Total share base of HY is just 300 mil. To pay 50 sen dividend, HY just need to come out of RM150 mil. Hengyuan may become NET CASH company after Q4'2017 or Q1'2018 if their cash pile can further increase to more than 1.2 billion (supported by strong earning).

Actually current market capital of Petronm is just RM3.56 billion but they need to invest RM14 billion for just 90 kpbd upgrade.

If we compare Petronm big 14 billion upgrade with HY RM580 mil upgrade cost, (this excluding the 2-3 year times cost for Petronm), considerable long shut down time, new inventory cost (for additional 90k bpd), then we will find HY Euro 4M upgrade is way cheaper and just needs 2.5 months shut down (include maintenence time).

Petronm would needs to proceed with this big investment is due to their current refinery plant is too old (simple refinery) which their Diesel and Gasoline yields are relatively low. One of the simple refinery main products is heavy Fuel oil which actually has Negative spread or margin (based on CME data). Refer to the below news for dropping of fuel oil margin.

https://www.bloomberg.com/news/articles/2018-01-17/oil-at-70-proves-too-hot-to-handle-for-some-european-refineries

If RM14 billion investment cost is obtained through borrowing, the interest cost base on 5% rate will lead to RM700mil per year. Anyway, based on current high crack spread data, the yield estimated by Petron President is relative high at USD600 mil (but that is to assume current high spread need to be maintained in 2020-2021 as the new plant only ready in 2020).

If Petronm proceed with the upgrade, there will be Big deprecation per year from the RM14 billion upgrade which will greatly affect their future accounting profit.

It is like if you bought a Toyota Camry under a company asset, first 3 years will have relatively high depreciation in accounting. After 3 years, the vehicle value may close to zero in term of asset but the vehicle (Toyota camry) still can work fine for company activities (sales or delivery of goods).

Let me have a SWOT analysis on HengYuan as below:

SWOT analysis (S-strengths, W-weaknesses, O-opportunities, and T-threats)

Risk

1. Unplanned shut down due to unexpected machines or refinery system break down.

2. Fire or explosion due to accident.

3. Delay in Euro 4 project upgrade.

Summary

1. HY’s profit visibility in Q4 still good based on current spread data on Diesel and Gasoline.

2. Forward 3-month PE of Hengyuan could be very attractive (below PEX4.5) even based on current price of RM14.00.

3. The high quality of Hengyuan’s earning is supported by strong ROIC (48.1%), ROE (56.3%), and strong cash flow generation from operation.

4. There is inventory gain for HY in Q4 as current Brent oil price stay above USD67 on 30 Dec 2017.

5. Recent RMUSD rate appreciation will further benefit HY as its material cost will be lower. Besides, it also may have forex gain as it has over RM1.3 billion of USD denominated loan.

6. The outlook for refined products is still bright in 2018 as in view of many refiners are scheduled to maintenance shut down, increasing demands from growing vehicle populations

If you interested on my analysis report, please contact me at davidlimtsi3@gmail.com

Since I am going to talk about oil Inventory, let us first have a look at this Google satellite image below which gives a good overview on the facilities or storage capacity of Hengyuan in Port Dickson, N. Sembilan.

Source: Google map

From the above image, we can see that HY plant has many storage tanks ranging from giants (having thousands of oil barrel storage capacity), medium tanks and smaller sizes of tanks (more than 100 units from my calculations).

These tanks are important for HY to store crude oils and refined product. Current inventory of HY is valued at RM 1.263 Billion consisting of their crude feed oil and refined products which are stored in these tanks. All these tanks and pipes (pipes too small to be seen from Google photo unless you zoom in to max) are super expensive to build nowadays not even bringing the cost of the Plant & Machinery, i.e the Refinery Complex consisting of Distillation Units and Catalytic Crackers (will share more on this on my next section on Petronm new upgrade project)

Why inventory and storage are important? Huge inventory (especially refined products) can serve as buffer when HY undergo shut down in Q3’2018 or make sure sales of their products to Shell Malaysia as sustained as usual during minor unplanned shut down. Actually we can observe that HY slowly raise their inventory level in the past 3 quarters.

Another advantage of huge inventory during crude oil uptrend time is it can book considerable inventory gain. Let us go through recent Brent oil price, Mogas 95 and Diesel price charts as below to know the possible inventory gain and profit margin as below:

Chart 1 : Brent oil (Souce: CME website) Chart 2 : Diesel = Gasoil (Souce: CME website)Chart 3 : Mogas 95 = petrol (Souce: CME website)

Crude oil theoretical Inventory Gain = [67 (30 Dec price) – 56 (30 Sept price) ] /3 = USD3.7 per barrel.

I divide inventory gain by 3 is based on backward calculation of past record of USD1.67 inventory gain as per Q3 report.

HY keep around 3.5 million barrels crude oil (info form hrc.com.my).

Estimated inventory gain from Crude oil = 3.5M X 3.7 X 4 = RM51.8 mil

Their refined products inventory gain maybe include in the sales to its customer. For example, their old stock of inventory cost of refined products maybe USD65 (due to that time crude is cheaper), their selling price in Dec may reach USD78, as a result, HY may enjoy USD12 profit margin per barrel. This is called First-in-First out.

Q4’17 and Q1’18 profit margin

Two main products of HY are Diesel (Gasoil) and Gasoline (Mogas 95) which constitute about 80% of the revenue.

Refer chart below:

Typical yield as per below:Diesel = 43%

Kerosene, LPG and others = 21%

Petrol (Mogas95) = 36%

Diesel product gross profit margin is obtained from subtraction of daily data of chart no 1 by chart no 2 as below:

Diesel Crack spread (margin) = Diesel selling price (chart 2) – Brent oil price (chart 1) [Eg. 81.56 – 69.3]

Mogas 95 product gross profit margin is obtained from subtraction of daily data of chart no 1 by chart no 3 as below:

Mogas 95 Crack spread (margin) = Mogas 95 selling price – Brent oil price

Average Mogas 95, jet fuel and diesel spread in Q4’2017 based on my previous article is around USD11.2. (https://klse.i3investor.com/blogs/davidtslim/143634.jsp). If we include LPG, Naphtha, propylene, fuel oil, average crack spread or profit margin per barrel maybe around USD9.5 - USD10

(Note: As per their respective yields, its average refining margin is much higher. However, for conservative reasons I am not using these values.)

As far as I survey from online, most of the refinery plants running on 24 X 7 days (including holiday).

Let us calculate how much gross profit (GP) per day for HY based on USD9.5 average crack spread

GP = USD9.5 X 4 X 112k = RM4.26 mil per day

Q4 contain 92 days. Let assume 2 days down time in Q4, then

GP = RM4.26 mil X 90 days = RM383 mil

Total gross profit = 383 + 51.8 mil = RM435.2

Estimated admin cost, depreciation, manufacturing expenses and Finance cost = 127 mil (based on Q3 figure)

There is high possibility of forex gain and small amount of other income in Q4 (as per Q3 report)

Let assume similar forex gain as per Q3 forex gain (50 mil as RM actually strengthen in Q4 more than Q3), and same other income of 9 mil.

Estimated Net income before tax in Q4 = 435.2 – 127 +50 + 9 = 367 mil.

Profit before tax of RM367 mil translated to EPS of 122.6 sen in Q4.

Some of you may worry of Q1’18 Mogas 95 spread is dropping. But HY main product consist of Diesel which has relative higher spread (range from USD11 to 12++) in past 15 days of Jan 2018. This actually can compensate the drop in Mogas 95 spread which lead the average spread of these two products is still more than USD10 based on my data collected.

Still worry about Mogas 95 spread in Q1'18? Let us go through the future crack spread data of Mogas 95 in Feb, Mar and April as below:

Source: CME website

The future contract of Mogas 95 is trading at USD80.04 (feb) to 80.795 (April). The higher selling price of Mogas 95 may due to ending of winter season in March which the demands of gasoline is anticipated to be higher in Spring season (higher travelling). If you checked the future data of Brent oil in CME (Mar and April), brent oil is trading at USD69 – 68++ which indicate the Mogas 95 spread at that time may increase to a level of USD10++.

Cost of new refinery upgrade and Simple Valuation

As highlighted in my HY part 6 article, oil refinery is a capital-intensive business. Planning, designing, permitting and building a new medium-sized refinery is a 2-5 year process.

Let see how much the budget for coming Petronm refinery upgrade as per news below:

https://businessmirror.com.ph/petron-refinery-expansion-seen-completed-by-2020/

Let me summarize the cost for building new and upgrade exiting refineries in Asia and South East Asia as table below

|

|

Estimated Cost |

Remarks |

|

Petron Corp Philippines |

USD3.5billion (upgrade existing to 270k from 180kbpd) |

Going to start in Q1’18 |

|

Petronm Upgrade from 88kbpd to 180 kbpd |

RM14 billion (USD3.5 B) |

Final proposal stage |

|

HengYuan |

4.29 billion for license capacity of 156k but rated capacity of 125k bpd |

Euro 4M upgrade maybe further increase HY capacity |

= (8+14 billion / (90) kbpd

= RM0.16 billion or RM160 mil per 1kbpd

Average cost for upgrade existing refinery (Petronm)

= 14 billion / 90 kbpd

= RM0.16 billion or RM160 mil per 1kbpd

HY current market cap is RM4.29 billion. If we calculate its valuation for its kilo barrel per day (kbpd):

Market Valuation of 1 kilo barrel capacity of HY (based on HY current whole market capital on 19 Jan, RM14.30 per share price)

= 4290mil / 125 = RM34.32 mil for every 1kbpd.

Let see another news on Saudi Arabia possible investment in China refinery plant as below:

https://oilprice.com/Latest-Energy-News/World-News/Saudi-Aramco-In-Talks-To-Buy-2B-Stake-In-PetroChina-Refinery.html

Aramco (one of the world biggest oil companies) willing to pay USD2 billion for 30% stake of 260 kbpd refinery plant in china (normally can be built at lower cost than other countries using China technology).

30% of 260 kbpd is 78kbpd. USD2 billion = RM8 billion for a new refinery plant in China.

Hengyuan current market capital is RM4.29 billion (based on current price of RM14.30) for a rated capacity of 125k bpd.

The beauty of HY refinery is it is a complex refinery with possible earning capability of RM1 billion per year (base on 2017 spread, HY has earned 752 mil in 3 quarters of 2017).

Free cash flow also strong in 2017 (predicted can be maintained in Q1 and Q2 of 2018) which currently they has level of cash in hand of RM898 mil as per 30 Sept 2017. Total share base of HY is just 300 mil. To pay 50 sen dividend, HY just need to come out of RM150 mil. Hengyuan may become NET CASH company after Q4'2017 or Q1'2018 if their cash pile can further increase to more than 1.2 billion (supported by strong earning).

Actually current market capital of Petronm is just RM3.56 billion but they need to invest RM14 billion for just 90 kpbd upgrade.

If we compare Petronm big 14 billion upgrade with HY RM580 mil upgrade cost, (this excluding the 2-3 year times cost for Petronm), considerable long shut down time, new inventory cost (for additional 90k bpd), then we will find HY Euro 4M upgrade is way cheaper and just needs 2.5 months shut down (include maintenence time).

Petronm would needs to proceed with this big investment is due to their current refinery plant is too old (simple refinery) which their Diesel and Gasoline yields are relatively low. One of the simple refinery main products is heavy Fuel oil which actually has Negative spread or margin (based on CME data). Refer to the below news for dropping of fuel oil margin.

https://www.bloomberg.com/news/articles/2018-01-17/oil-at-70-proves-too-hot-to-handle-for-some-european-refineries

If RM14 billion investment cost is obtained through borrowing, the interest cost base on 5% rate will lead to RM700mil per year. Anyway, based on current high crack spread data, the yield estimated by Petron President is relative high at USD600 mil (but that is to assume current high spread need to be maintained in 2020-2021 as the new plant only ready in 2020).

If Petronm proceed with the upgrade, there will be Big deprecation per year from the RM14 billion upgrade which will greatly affect their future accounting profit.

It is like if you bought a Toyota Camry under a company asset, first 3 years will have relatively high depreciation in accounting. After 3 years, the vehicle value may close to zero in term of asset but the vehicle (Toyota camry) still can work fine for company activities (sales or delivery of goods).

Let me have a SWOT analysis on HengYuan as below:

SWOT analysis (S-strengths, W-weaknesses, O-opportunities, and T-threats)

|

Strengths |

Weaknesses |

|

1.Highest profit margin (high spread from 2017 to 2018)

2.Strong cash flow generation

3.Their refinery system has depreciation

of RM200 mil per year for many years which the value already closed to

fair value. Their system still works fine and after upgrade may has

higher efficiency – mean accounting profit not affected too much by

depreciation

4. High inventory level

5. Highest ROE and ROIC, ROA

6.Flexibility of their refinery system to

tweak for different crude oil and different refined product slate (may

tweak to higher profit margin products)

|

1. Big capital expenditure for upgrade (but 580 mil is far or way cheaper than peer petronm 14 Billion upgrade)

2. Fluctuation of crack spread or refined

margin may affect profit margin. (Many refinery plants scheduled shut

down in 2018 should lead to stable crack spread based on my estimation)

3. High debt of 1.3

billion but the strong earnings in 1.2 year OR high inventory (highly

liquidable) can paid off 95% of the debt.

|

|

Opportunities |

Threats |

|

1.ASEAN and Asia vehicle population growth will provide support for the stable crack spread or margin

2. 2020 IMO global bunker fuel regulation will be a

opportunity for complex refiner like Hengyuan (Refining capacity might

fall short of demand after 2020 -Varo CEO https://www.reuters.com/article/refineries-oil/refining-capacity-might...

Diesel or low sulfur gasoil demands may increase due to IMO implementation in 2020.

High sulfur fuel oil demand may drop in 2020 which maybe one of the reasons of Petronm upgrade.

|

1.High crude oil price increase the material cost (but will have inventory gain)

|

1. Unplanned shut down due to unexpected machines or refinery system break down.

2. Fire or explosion due to accident.

3. Delay in Euro 4 project upgrade.

Summary

1. HY’s profit visibility in Q4 still good based on current spread data on Diesel and Gasoline.

2. Forward 3-month PE of Hengyuan could be very attractive (below PEX4.5) even based on current price of RM14.00.

3. The high quality of Hengyuan’s earning is supported by strong ROIC (48.1%), ROE (56.3%), and strong cash flow generation from operation.

4. There is inventory gain for HY in Q4 as current Brent oil price stay above USD67 on 30 Dec 2017.

5. Recent RMUSD rate appreciation will further benefit HY as its material cost will be lower. Besides, it also may have forex gain as it has over RM1.3 billion of USD denominated loan.

6. The outlook for refined products is still bright in 2018 as in view of many refiners are scheduled to maintenance shut down, increasing demands from growing vehicle populations

If you interested on my analysis report, please contact me at davidlimtsi3@gmail.com

You can get my latest update on share analysis at Telegram Channel ==> https://t.me/davidshare

Disclaimer:

This writing is based on my own assumptions and estimations. It is

strictly for sharing purpose, not a buy or sell call of the company.