This is it!

It is up to you to believe SUMATEC will RALLY to 25sen at least by this month; depends on annoucement of its 4QFY17 results. It is expected to be announced this week or next week. If they announce next week, the share price of SUMATEC will rally until early of March.

This 4QFY17 results is important to indicate another strong earnings in FY18 and onwards, and this will help the share price to reflect my FY18 current valuation of 56sen.

My FY18 TP of 56sen remains intact, based on my FY18 DCF assumption and has not fully reflected in the share price yet.

Remember that as long as oil prices maintain at and above USD60/b, my FY18 valuation remains unchanged at 56sen because my average oil price forecast is at USD60/b and in fact, poised for more upside but then could be offsett by weaker USD.

So far, oil prices has become a push factor for SUMATEC. According to the Company, they can make net of USD30-35/b even though oil prices at USD50/b.

The rally will be on the back of its potential exponential earnings episodes. It will start with sequential strong 4Q earnings. Quarterly, its financial results has started to turnaround in 3QFY17.

Given favourable oil prices in 4Q2017, its 4QFY17 earnings would be surely registered even higher.

On production, recall that SUMATEC has commenced an oil production enhancement program back in April 2017, which encompasses the improvement / repairing of existing wells that include rehabilitation and rejunevation works, drilling of new wells for appraisal and production, construction of oilfield surface facilities and upgrading of the central processing facilities.

Now, the flow results of the initial wells have been encouraging and they expect total oil production to improve further.

SUMATEC has reactivated the oil production enhancement program in 2H2017.

The oil production is expected to reach 1500bbl/d by end of March 2018.

Another 1000bbl/d can be added to the oil production after the completion of 12 well workovers by end of August 2018.

The

total oil production can further increase to about 7500bbl/d with the

drilling of two new deep Triassic wells by end of 2018.

As oil prices has stabilised and recorded high this year since 2015, we can expect SUMATEC is poised to register even stronger earnings this year and onwards.

[J. P. Morgan has raised its forecast for Brent crude oil prices to an AVERAGE USD70 a barrel on its view that growth in economies around the world will boost demand for energy.

Stronger-than-anticipated business activity, economic growth and consumer spending convinced that oil demand will be better than expected in the first half of 2018. Brent prices will rise toward USD78 a barrel in the first or second quarter of the year, JP Morgan forecast in a research note released late January 2018.

To put that oil price call in context, Merrill Lynch recently upped its Brent target to USD64 a barrel, the bank also raised its estimate for U.S. crude by USD10.70 to USD65.63 a barrel.]

Yet, I have been conservative in my earnings forecast and this TP of 56sen.

In fact, my current valuation is also still based on 50% stake of Rakuschechnoye asset and excluding gas’ contribution, apart from current conservative production forecast and oil price assumptions.

Maybe some of you still don’t understand their business. Let's recall again!

SUMATEC is currently an investor and operator of the O&G Rakuschechnoye field, Khazakhstan as per previous joint agreement in 2012.

Meanwhile, the BEST part to come and on-going corporate exercise is SUMATEC has proposed to acquire 100% stake in Karaturun field, another O&G asset in Khazakhstan, which has also been included into recent multiple proposals.

Essentially, the proposal of aquisition of Karaturun asset has been on-going BEFORE this recent multiple proposals. That’s why I included this asset into my valuation!

This Karaturun asset will be HUGE earnings accretive to SUMATEC’s FY18 and onwards once it consolidated everything later this year, and it will increase SUMATEC’s valuation further.

In other words, my valuation of 56sen is SUMATEC as being current role at Rakuschechnoye and potential assets value of Karaturun asset to be injected into.

Karaturun asset is not new oil wells/field and has been operating for many years over there. Meanwhile, Rakuschechnoye field is quite new and need to be explored and develop further.

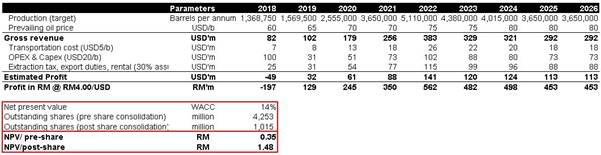

This is Rakushechnoye asset, worth of 21sen pre-share consolidation.

This is Karaturun asset, worth of 35sen pre-share consolidation

* Note that terms of "profit in RM" means cash flow. So, negative cash flow in FY18 for Karaturun asset will not reflect in FY18 earnings as it is including capex. To see real earnings for FY18 and the rest, deduct capex.

In total, its assets in Khazakhstan is worth 56sen as of FY18 DCF valuation.

This valuation excluding gas production (currently contract billing recognized based on the progress of the work program for the development).

Should I include this (as they just recently signed pre-sale agreement with their customer), the valuation would be even higher!

Another best part to come and on-going, together with the acquisition proposals, the Company has proposed to restructure its balance sheet to eliminate accumulated losses and settle all litigations.

They have also proposed to consolidate the number of shares from 4 billion plus of shares currently to 1 billion plus.

Post-completion of all proposals, the Company will achieve as following:

Although the Company also proposed to raise funds from rights issue to funding the acquisition of abovementioned asset, the valuation of SUMATEC will remain attractive post-acquisition even though it may dilute its earnings.

Final say

That is why I have said many times and remind everyone again and again that market has underestimated potential value in SUMATEC, and this is why the share price has yet to react to its potential value.

People buy into story, once the proposal completed, share price might be priced in everything that time.

As of now, I maintain my pre-share consolidation valuation of 56sen for FY18 until the completion of all proposals later this year.

DON'T REGRET LATER!