Recently, I bought Hengyuan and Petronm. And I did it without even checking the crack spread.

Why ? Isn't crack spread an important determinant of their profitability ?

Yes, of course it is. But it is only important if you are a short term player.

If you put on the cap of a long term investor, you will think like this :-

(a) Hengyuan and Petronm are currently trading near their recent years low, so it is a good time to enter (less susceptible to sell down by early birds as there is simply no excesses there);

(b) PER is low (based on earning power);

(c) Crack spread goes up and down all the time. Why should you be bothered ? If it comes down and causes the company's profitability to drop drastically, it is likely to be a temporary blip. History shows that crackspread never stay depressed or elevated indefinitely. In a few quarters time, earning is likely to recover when spread reverses to the mean.

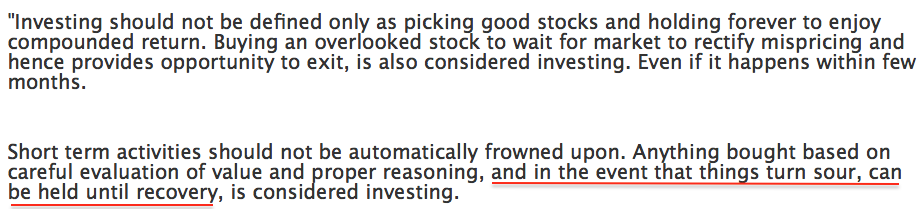

By saying so, I am putting what I have been preaching recently into practice : "Investing involves buying something that in the event that things turn sour, will ultimately recover if you hold on for a reasonable period of time." (something to that effect)

(d) But what are the criterias for picking Hengyuan and Petronm out of so many stocks in Bursa ?

Because they are established players in a robust industry. The quality is there (as far as I am concerned). Instead of putting my money in an ACE counter selling tickets to the moon, I am buying into companies with many years of track record, sizeable in scale, high entry barriers, well regulated by the government and plenty of room to grow (driven by demographics and growth in per capita income). The ACE counter might not be there in 3 years' time, but Hengyuan and Petronm will very likely still be there.

In short, they are of investment grade quality.

(e) What is the gameplan ? How do you intend to make money out of them ?

Through organic growth !!! Crackspread will cause their profitability to fluctuate from quarter to quarter. In certain quarters, they might even dip into the red. But who cares ? Earning will ultimately rebound when spread normalised. Just ignore the volatility. It is merely paper loss, if it happens.

Over an extended period of time, they will reinvest their earning, expand their network and capacity. If you come back 10 years later, they might have grown into sizes beyond your recognition. So will their profitability.

We are talking about investing mah.

(f) How about moat ? Don't you want to check whether they have moat ?

Nah... moat is overrated. Many companies in Bursa do not have visible sign of moat. But many investors still make money out of them. As long as you have a good feel of how the company can evolve and grow over an extended period of time (in this case, together with the economy, without insane competition), they are good for investment.

Concluding Remarks

First of all, the major reason I bought into Hengyuan and Petronm is because they are trading at very low PER (based on earning power).

By taking a long term view, I cease to worry about the coming quarters result. Meaning I can just put them aside and get busy with other things in my life. This is the most basic definition of investing, isn't it ?

However, this is not applicable to all companies in Bursa. If you take exposure in a fly by night ACE counter, you better monitor it closely, because it can eventually go kaput.

Happy investing !!!

https://klse.i3investor.com/blogs/icon8888/190935.jsp

Why ? Isn't crack spread an important determinant of their profitability ?

Yes, of course it is. But it is only important if you are a short term player.

If you put on the cap of a long term investor, you will think like this :-

(a) Hengyuan and Petronm are currently trading near their recent years low, so it is a good time to enter (less susceptible to sell down by early birds as there is simply no excesses there);

(b) PER is low (based on earning power);

(c) Crack spread goes up and down all the time. Why should you be bothered ? If it comes down and causes the company's profitability to drop drastically, it is likely to be a temporary blip. History shows that crackspread never stay depressed or elevated indefinitely. In a few quarters time, earning is likely to recover when spread reverses to the mean.

By saying so, I am putting what I have been preaching recently into practice : "Investing involves buying something that in the event that things turn sour, will ultimately recover if you hold on for a reasonable period of time." (something to that effect)

(d) But what are the criterias for picking Hengyuan and Petronm out of so many stocks in Bursa ?

Because they are established players in a robust industry. The quality is there (as far as I am concerned). Instead of putting my money in an ACE counter selling tickets to the moon, I am buying into companies with many years of track record, sizeable in scale, high entry barriers, well regulated by the government and plenty of room to grow (driven by demographics and growth in per capita income). The ACE counter might not be there in 3 years' time, but Hengyuan and Petronm will very likely still be there.

In short, they are of investment grade quality.

(e) What is the gameplan ? How do you intend to make money out of them ?

Through organic growth !!! Crackspread will cause their profitability to fluctuate from quarter to quarter. In certain quarters, they might even dip into the red. But who cares ? Earning will ultimately rebound when spread normalised. Just ignore the volatility. It is merely paper loss, if it happens.

Over an extended period of time, they will reinvest their earning, expand their network and capacity. If you come back 10 years later, they might have grown into sizes beyond your recognition. So will their profitability.

We are talking about investing mah.

(f) How about moat ? Don't you want to check whether they have moat ?

Nah... moat is overrated. Many companies in Bursa do not have visible sign of moat. But many investors still make money out of them. As long as you have a good feel of how the company can evolve and grow over an extended period of time (in this case, together with the economy, without insane competition), they are good for investment.

Concluding Remarks

First of all, the major reason I bought into Hengyuan and Petronm is because they are trading at very low PER (based on earning power).

By taking a long term view, I cease to worry about the coming quarters result. Meaning I can just put them aside and get busy with other things in my life. This is the most basic definition of investing, isn't it ?

However, this is not applicable to all companies in Bursa. If you take exposure in a fly by night ACE counter, you better monitor it closely, because it can eventually go kaput.

Happy investing !!!

https://klse.i3investor.com/blogs/icon8888/190935.jsp