Cover Story: Will ATE stocks continue to outperform OSAT counters?

THE share price performance of Bursa Malaysia-listed semiconductor and semiconductor-related firms have been nothing but spectacular in the past five years.

In fact, during the mid-year stock market rally in 2020, the tech stocks were overshadowed only by rubber glove counters, which lost their shine after the roll-out of Covid-19 vaccines at the year-end.

Amid the ongoing global chip crunch and US-China trade war, the tech stocks’ performance remained largely intact, albeit slightly below their historical highs.

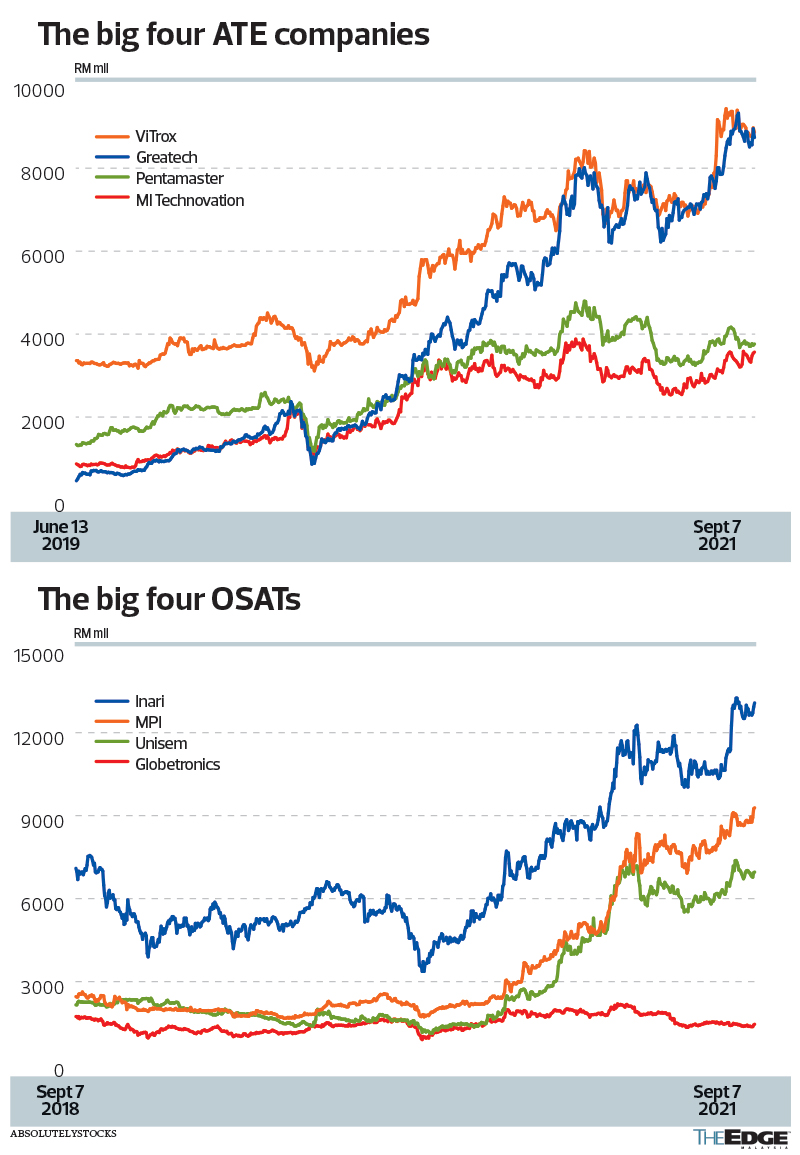

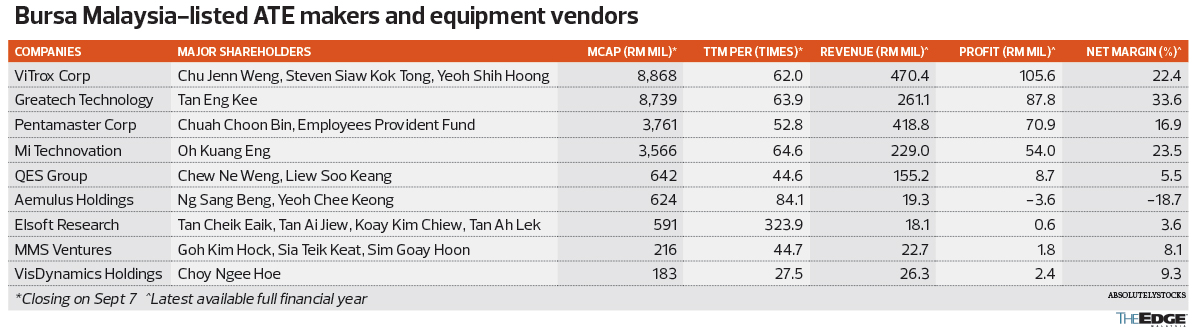

And if investors were to take a deep dive into the semiconductor sector, they would realise that in terms of share price gain, the automated test equipment (ATE) manufacturers and technology equipment vendors have been outperforming the outsourced semiconductor assembly and test (OSAT) companies in recent years.

For instance, equipment giants ViTrox Corp Bhd and Pentamaster Corp Bhd saw their stock prices jump 10 and 19 times respectively over the last five years, while Greatech Technology Bhd has surged 16 times since its listing in 2019.

In comparison, the major OSAT players — Inari Amertron Bhd, Unisem (M) Bhd and Malaysian Pacific Industries Bhd (MPI) — saw their share prices increase by three to five times, which was still remarkable, considering they had been growing from a higher base.

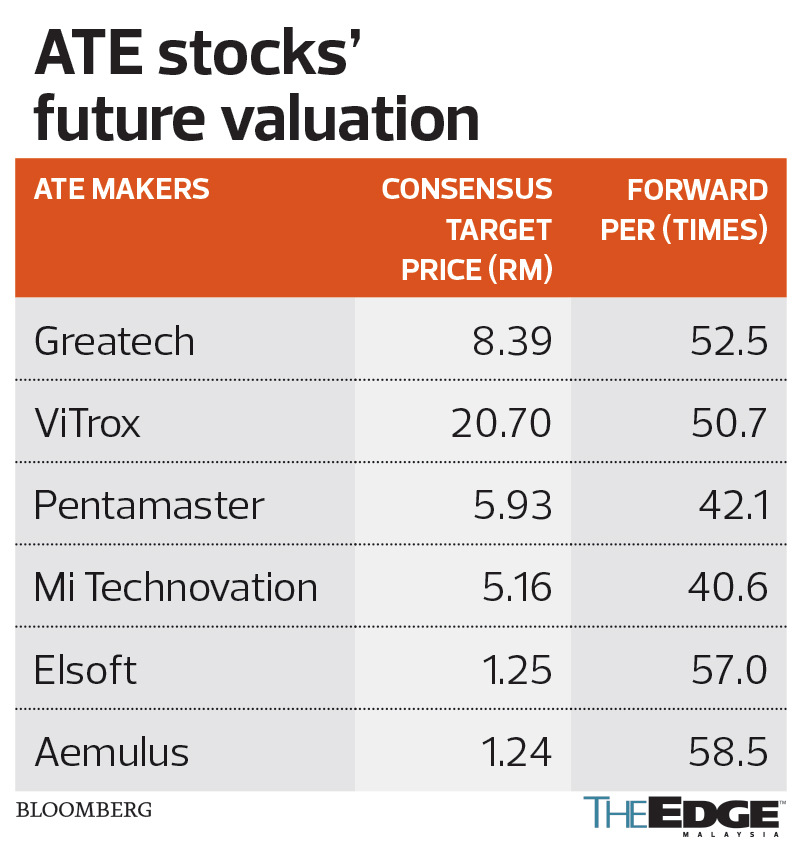

But judging from their forward price-earnings ratios (PERs) and, for that matter, their historical PERs, the fact remains that investors are paying a premium for ATE stocks over OSAT counters.

Based on Bloomberg data, Inari, Unisem, MPI, and their smaller peer Globetronics Technology Bhd are trading at forward PERs of between 25 and 32 times, whereas those for ATE companies such as ViTrox, Pentamaster, Greatech, MI Technovation Bhd, Aemulus Holdings Bhd and Elsoft Research Bhd are between 40 and 60 times.

What are the reasons for the divergence? More importantly, for investors keen to invest in tech stocks, which subsector is a better buy?

ViTrox co-founder and executive vice-president Yeoh Shih Hoong points out that ATE involves more technical and research and development (R&D) elements, thus creating a high-income society in line with the government’s objectives.

“It is also an industry that has proven that Malaysia may have an edge in the world market. Generally, ATE has a higher profit margin as compared to OSAT because we [mostly do] our own R&D and marketing — the two ends of the smiling curve,” he tells The Edge.

Yeoh goes on to say that the Fourth Industrial Revolution and the Covid-19 pandemic will push the demand for automated vision inspection equipment and ATE to an unprecedented level.

“Nowadays, manufacturers are more willing to invest in machines than people, to increase the productivity, continuity and yield of manufacturing,” he remarks.

Greatech CEO Tan Eng Kee believes that the most important element investors should focus on is a company’s innovation platform, and not just the industries it is in.

“A company with strong R&D activities, that produces good products and has a globalised market, will project a better share price for sure. Basically, Malaysian investors love to invest in tech stocks, paving the way for a lot of local small and medium enterprises to enter the market, thus creating stiff but healthy competition among the local players. In the long run, when every player strives to give its best, this will expand growth and benefit the country’s economy,” he observes.

MI Technovation CEO Oh Kuang Eng also highlights that the profit margins of ATE companies are overall better than that of OSAT firms. That’s because the former own the equipment technology whereas the latter buy equipment and provide services to their clients.

“OSAT players are competing on prices, but ATE players are competing on technology. If you ask me, the prospects for both ATE and OSAT players will remain bright in the next 10 to 20 years because semiconductors is an expanding sector, not a shrinking sector. As an investor, I would buy into equipment companies that are heavily involved in technology, and those with diversified product portfolios.

“In the semiconductor industry, the winner takes all. Everyone wants to buy the proven best product. So, if we are successful in a certain area, our clients will only buy our equipment in that area. In the ATE industry, you must be No 1 in a certain area,” Oh elaborates.

Pentamaster chairman Chuah Choon Bin concurs that local OSAT players will continue to grow in the next few years, given that front-end semiconductor equipment investments have doubled over the last few years, especially in the area of Internet of Things, electric vehicles and fifth generation connectivity.

He acknowledges that China is still the biggest market and the country has many far bigger OSAT players for its internal supply chain market. Realistically, it is tough to compete with the Chinese OSAT players as they are very cost competitive and have a bigger scale in set-up.

“I would say the ATE market is sexier because when technology keeps changing, manufacturing requirements [also change], so there will be more business opportunities for us,” Chuah explains.

According to MMS Ventures Bhd (MMSV) co-founder and CEO Sia Teik Keat, most ATE companies have good potential for growth. But he believes those that have grown to a certain size will find it tough to sustain high growth rates.

“As for those who are relatively smaller, their growth potential is higher. I would like to think that MMSV still has good upside potential. Our difficulty is sales and marketing. We have a lot of products, but we have not been able to sell enough. We need to venture into new markets and to secure new clients.

“In a nutshell, I think ATE has bright prospects, and I believe the ATE companies should be able to grow faster than the OSAT players,” Sia concludes.

A check on Bloomberg shows that both ATE and OSAT players still have fairly attractive upside potential. If the research analysts are not wrong, OSATs such as Inari, MPI, Unisem and Globetronics could go up as much as 10% to 25% in the next 12 months.

As for ATE, the likes of Greatech, Aemulus, MI Technovation, and Elsoft have potential upside of 20% to 50%, whereas ViTrox and Pentamaster’s is lower at 8% to 13%.

http://www.theedgemarkets.com/article/cover-story-will-ate-stocks-continue-outperform-osat-counters