KNM (7164) KNM GROUP BHD — a new chapter or asset stripping?

SINCE last month, KNM Group Bhd’s share price has been climbing steadily, amid speculation that it is in the midst of unlocking asset values, including hiving off its crown jewel Borsig GmbH in Germany. The debt-laden company is also said to be working on the long-delayed sale of its 36mw waste-to-energy plant in the UK.

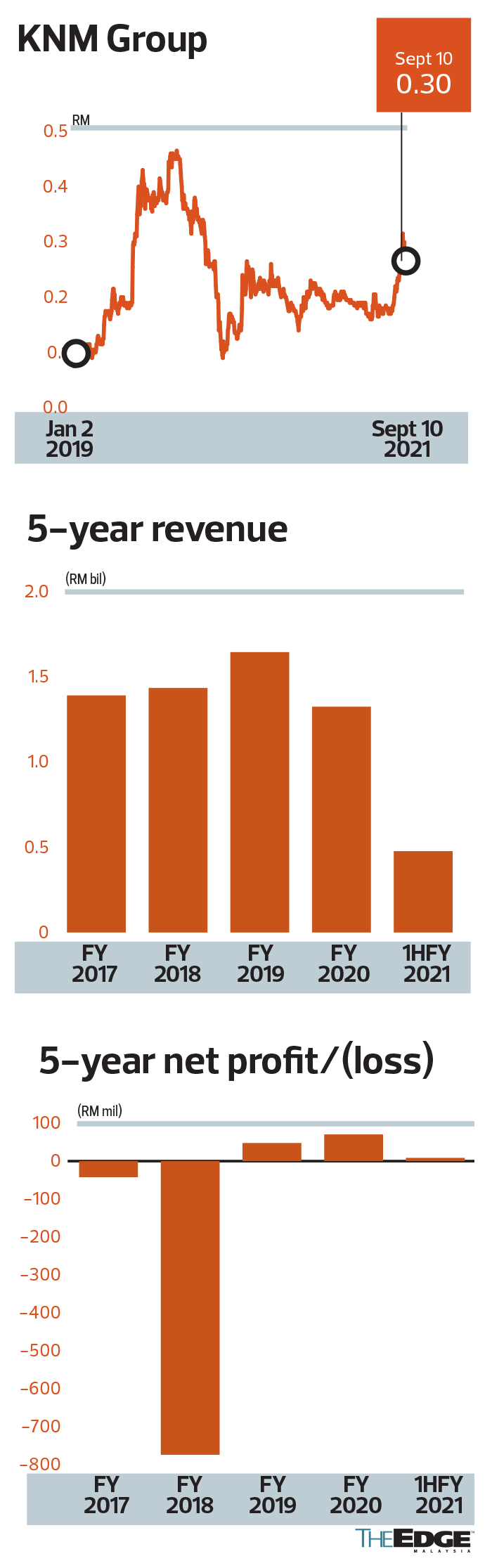

Despite the group’s stretched balance sheet and poor results for the first half of 2021, its share price soared from 18 sen at the start of August to a 17-month high of 32 sen on Sept 7.

It was high up on the list of most traded counters on Bursa Malaysia as its daily trading volume surged threefold to more than 200 million shares. It retreated from the peak to close at 30 sen last Friday, giving the company a market capitalisation of RM998.41 million.

Its CEO Terrence Tan, when contacted, was tight-lipped about any upcoming corporate proposals.

Bluntly put, the tale of unlocking asset values is not new to the investing fraternity. Whether the plan will pan out this time around is yet to be seen.

But one thing is certain — investors who bought shares from the company’s placements should be jumping for joy now. The three rounds of share placements since June 2019 were priced at between 16 sen and 17.5 sen.

That said, the difference this time is that KNM’s founder and long-time shareholder Lee Swee Eng is no longer in the driver’s seat, although he holds a 7.91% stake.

Also, cash-rich MAA Group Bhd, which has hived off its insurance business, sprung a surprise by acquiring an 8% stake in the industrial process equipment manufacturer, becoming the largest shareholder. Interestingly, MAA bought slightly less than 2% equity interest from Lee via an off-market deal.

MAA emerged as a substantial shareholder two month after a slew of boardroom changes at KNM, including the resignation of Lee’s spouse Gan Siew Liat as executive vice-chairman.

It is understood that several high-net-worth investors have also taken up positions in the company, including private equity fund manager Brahmal Vasudevan, who is founder and CEO of Creador. But it is not known if Brahmal’s investment is in his own capacity.

KNM’s shareholding is fragmented, with its single largest shareholder, MAA, holding only 8%, followed by Lee with 7.91%.

Why did MAA go into KNM?

The new entries have also given rise to rumours of a tussle in the company, which needs to streamline its core operations and trim its bloated borrowings.

The speculation was quickly dismissed by KNM’s management. Similarly, MAA executive chairman and controlling shareholder Tunku Datuk Yaacob Khyra brushed off the rumours when contacted by The Edge.

Yaacob says KNM came on MAA’s radar screen after Lee resigned from the board as there was no new major shareholder leading the firm. “I’m not aware of any tussle. I have spoken with Lee. He is taking a back seat and is very keen for MAA to take the leadership role in KNM.

“Of course, Lee will vote in our support if we were in need to have his vote for the right resolutions,” he says.

“And [KNM CEO] Terrence Tan has my full support. I think he’s doing a good job … But I think they can do with a few more [directors].

“Usually, yes [MAA would like to have board representation], so I’m hoping the existing board will be agreeable for us to have some [board] reps there. If they say no, we shall ask the shareholders to decide [at an EGM],” Yaacob says, showing MAA’s seriousness in the foray.

MAA had been sitting on a cash pile following the disposal of its Malaysian insurance business and after an unsuccessful bid by Yaacob in 2019 to take the company private.

The investment in KNM is MAA’s second corporate exercise this year. It offered to take over machinery and chemicals manufacturer Turiya Bhd in June.

MAA’s purchase into KNM was made for two reasons. “The company’s NAV is 53 sen per share. MAA started buying the shares at 18 sen. As an investment company, we see significant value and we have to make sure the company runs well for the benefit of all shareholders.”

The other, Yaacob says, is KNM’s prospects in anticipation of better activity outlook in sectors like oil and gas as capital expenditure improves.

“With oil prices at current levels [of above US$70/bbl], my view is that when you see the order book of equipment companies filling up, you start to see their [KNM’s] share price go beyond their NAV. They have good operating assets,” he adds.

To ride the recovery of the oil and gas sector as well as those of other sectors, KNM needs Borsig, its largest income contributor.

However, the Germany-based firm was put up for sale by the previous KNM board. In the background is a tranche of RM370 million bond that is due in November in Thailand. Hence, the previous board wanted to raise money for the bond redemption.

Yaacob’s view is that KNM should not let the bondholders hold it to ransom to sell Borsig at low price. Borsig is a major contributor to KNM’s bottom line, he says, adding that he believes it will be able to fetch a higher valuation when the industry’s outlook improves.

“I understand they are talking to a German buyer. My only issue is what’s the final price? The price must be good, or we can find another buyer.

“We should not let the Thai bond situation force us to sell Borsig at a cheap price. We can renegotiate or refinance the Thai bond,” says Yaacob, adding that the bond is guaranteed by Asian Development Bank (ADB).

Having MAA as a substantial shareholder, some quarters say, will help give KNM credibility at the negotiating table.

Nonetheless, it is worth noting that €126 million (RM616.7 million) of KNM’s debts are tied to Borsig. In short, selling Borsig will significantly improve its balance sheet.

Besides selling the crown jewel, another option for KNM is to monetise the waste-to-energy project in Peterborough, the UK, which is supposed to be completed next June. The renewable energy project was started more than 10 years ago.

“Keeping it is one option — if you can afford to. If not, KNM’s key activity is engineering, and the first key issue is to reduce borrowings, by a lot,” Yaacob says.

“Many of these renewable projects have very low IRRs (internal rates of return) of single digits. If you borrow at 3% to 4%, that’s not so attractive.

“I think people get over-excited about the ESG (environmental, social and governance) story, but [stakeholders] still want value for money. It will be good to sell at a profit. We can always find another project,” Yaacob says.

Assets and debts

KNM had been profitable in the past two financial years, save for a loss-making 1QFY2021. For the financial year ended Dec 31, 2020, its net profit rose nearly 55% to RM70.47 million or 2.63 sen per share, although revenue fell 19% to RM1.32 billion, from RM1.63 billion.

Borsig — which was acquired for €350 million or RM1.67 billion in 2008, prior to the oil price crash — generates pre-tax profit of around RM100 million annually.

KNM also has a bio-ethanol plant in Thailand parked under Impress Ethanol Co Ltd, which is en route to a capacity of 500,000 litres per day, from 200,000 litres per day currently. However, rising material costs resulted in operating losses through 2020.

On the other side of the balance sheet, KNM had total borrowings of RM1.33 billion at end-June, of which some RM711.68 million were short-term liabilities. Its cash balance stood at RM256.47 million.

It is understood that the previous board was seeking a minimum price tag of €300 million (RM1.47 billion) for Borsig. An attempt to sell two of Borsig’s subsidiaries fell through this year.

Notably, KNM managed to churn out RM116 million in net operating cash flow (after deducting interest paid and lease liabilities) in FY2020, compared with negative cash flow in the year before.

A sale of the nearly completed UK plant is estimated to give KNM about RM350 million, which would reduce its debts to RM985 million and net gearing to 0.4 times, from 0.6 times.

The sale may also help reduce its finance costs of around RM60 million or slightly above 40% of FY2020 group operating profit.

It should be noted that the gearing level is supported by equity, which has been expanded by three share placements between June 2019 and January this year. Notably, around RM425 million of its borrowings are conditional on a consolidated debt-to-equity ratio not exceeding 100% at all times. A total of 800.71 million shares were issued to raise RM134 million.

The placements alone represent 24% of the group’s current share base. Minority shareholders in June rejected a fourth private placement, which aimed to raise up to RM167.8 million to repay debts.

KNM currently has a share base comprising 3.33 billion shares after the placements and the series of employee share option schemes offered to its directors.

Given the steady recovery in oil price, the craze for renewable energy, and its heap of debts, like it or not, KNM could be a target for asset stripping.

It will be interesting to see whether the new shareholders have an ace up their sleeve that will make a difference this time round.

http://www.theedgemarkets.com/article/knm-%E2%80%94-new-chapter-or-asset-stripping