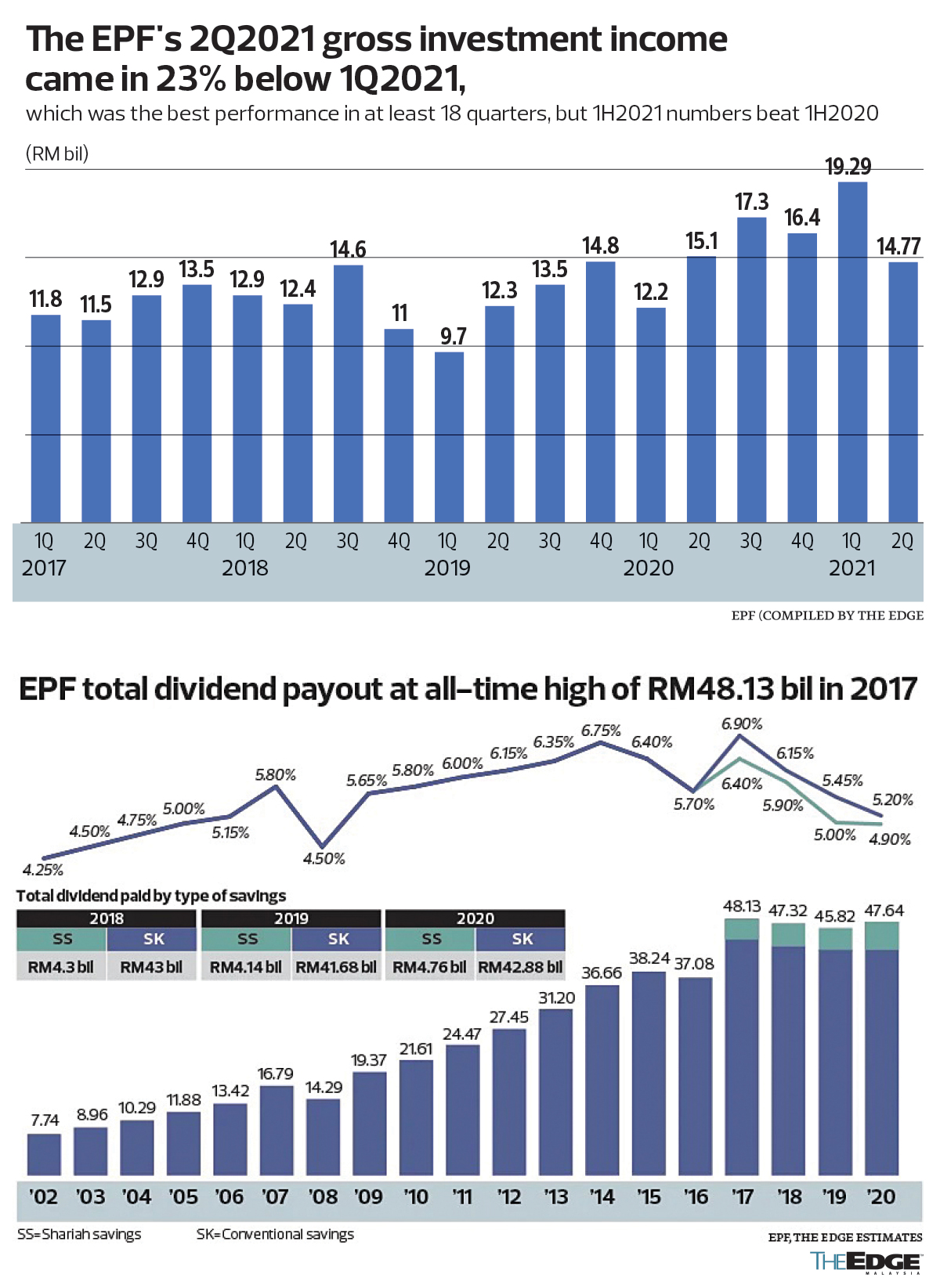

THE Employees Provident Fund’s RM14.77 billion gross investment income for the second quarter ended June 30, 2021 (2Q2021) came in 23% or RM4.52 billion below a record-high quarterly result of RM19.29 billion in 1Q2021.

The EPF’s total investment assets — which grew 7.9% or RM73 billion year on year (y-o-y) last year to end 2020 at RM998 billion — slipped 0.9% or RM8.86 billion in the first half of the year to RM989.14 billion as at end-June.

Yet, there is a good chance of the EPF paying a higher dividend for the whole of 2021 than the 5.2% paid for Conventional Savings (SK) and 4.9% paid for Shariah Savings (SS) last year if there continues to be little reason for write-downs.

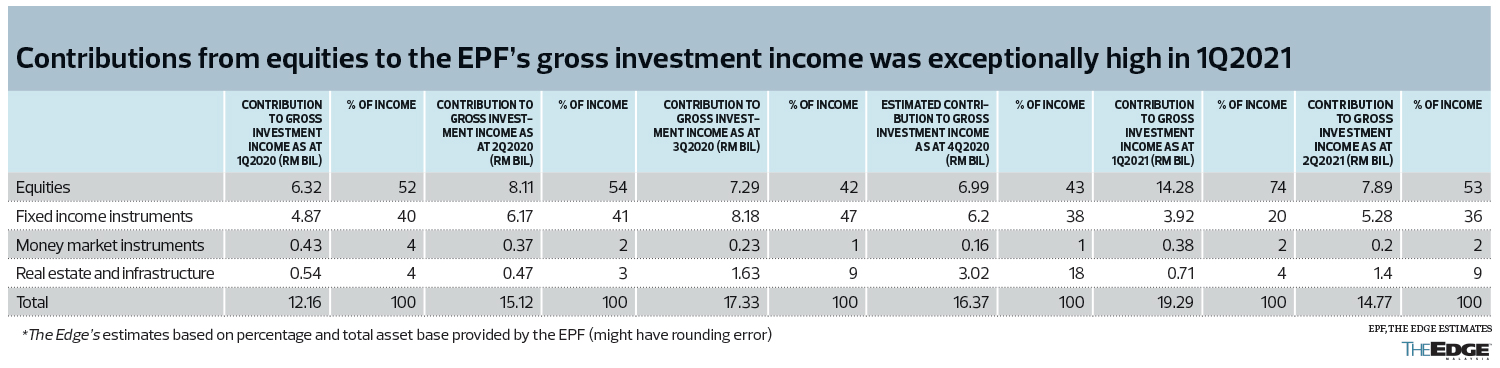

Thanks to exceptionally strong income contributions from equities in 1Q2021 of RM14.28 billion or 74% of the RM19.29 billion in gross investment income earned in the first three months of 2021, total gross investment income in the first half of 2021 (1H2021) was RM34.06 billion or 24.9% more than the RM27.28 billion booked in 1H2020.

Equities usually bring in RM6 billion to RM8 billion income per quarter, with contribution rarely above 60% of overall income while accounting for 35% to 45% of total assets (36%, according to its strategic asset allocation), The Edge’s compilation of EPF data shows. It is not immediately certain whether the strong performance was helped by equity write-backs.

“The EPF delivered a resilient performance in 1H2021, driven by the progressive recovery of the equity markets and most asset classes amid the global rebound,” EPF CEO Datuk Seri Amir Hamzah Azizan said in the Sept 24 statement accompanying the 2Q2021 performance release.

The EPF did not provide specific guidance on dividend but noted that its “diversification into different asset classes continued to provide income stability and added value to its overall return”. Some 37% of its RM989.14 billion investment assets as at end-June were overseas. They generated RM8.71 billion or 59% of total gross investment income in 2Q2021 and RM11.15 billion or 58% of total gross investment income in 1Q2021.

Exceptional 1Q2021

What we know is that the EPF’s net investment income of RM33.8 billion in 1H2021 was 61.3% more than the RM20.96 billion in 1H2020 — with only RM0.26 billion write-down largely from listed equities in 1H2021 compared with RM9.16 billion in 1H2020, of which RM7.5 billion took place in 1Q2020.

The 1H2021 performance is significant given that the EPF paid out RM47.64 billion in dividend in 2020 (RM42.88 billion for Conventional Savings and RM4.76 billion for Shariah Savings.

If indeed the amount to pay 1% of dividend to members for 2021 stays roughly unchanged at around the RM9.2 billion needed to pay 1% of dividend in 2020 as its total fund size stays roughly unchanged y-o-y owing to larger-than-usual withdrawals, the EPF only needs to earn about RM14 billion more net investment income for the rest of 2021 to be able to match the dividend it paid in 2020. This is why beating last year’s dividend payout should not be difficult, going by its past performance.

There is even a chance of 2021 dividend hitting 6% or close to it, if the EPF makes at least RM11 billion net investment income per quarter in the second half of the year, which is not impossible if there is no need for large write-downs, our back-of-the-envelope calculation shows. Annualising the RM33.8 billion net investment income for 1H2021 would point to even higher dividend, which may not be realistic given that it would be tough to repeat its feat in 1Q2021.

Amir told The Edge in June that “the threshold [to pay the same amount of dividend this year] will probably be about the same as last year”. Under a “normal” growth trajectory, the amount the EPF needs to pay 1% of dividend would have risen close to RM10 billion in 2021 from RM9.2 billion in 2020 and RM8.5 billion in 2019, according to The Edge’s estimates.

That means the EPF needs closer to RM46 billion (rather than RM50 billion) to pay 5% dividend for 2021 and closer to RM55.2 billion (rather than RM60 billion) to pay a 6% dividend. The EPF’s highest dividend payout to date was RM48.13 billion in 2017, where a dividend of 6.9% was declared for Conventional Savings and 6.4% for Shariah Savings and the amount to pay 1% of dividend was just over RM7 billion.

The y-o-y decline in the EPF’s total investment assets from RM998 billion as at end-December 2020 to RM989.14 billion as at end-June 2021 had much to do with the Covid-19-related special withdrawals. Of the RM79.6 billion approved under the i-Sinar Account 1 (RM58.8 billion approved for 6.6 billion applicants) and i-Citra Accounts 1 and 2 (RM20.8 billion approved for five million members) schemes, some RM67.6 billion had been disbursed (RM9.1 billion under i-Citra and RM58.5 billion under i-Sinar), according to the EPF’s statement.

About RM6 billion had also been taken out this year by members from Account 2 via the i-Lestari programme, which saw a total of RM20.8 billion withdrawn between April 2020 and March this year.

This was why The Edge wrote that the EPF may see a rare net withdrawal for the whole of 2021 based on approvals given to date this year (see “EPF returns intact, but policy change needed as i-Citra depletes more members’ savings” [Issue 1383, Aug 16, 2021]). This remains true, despite i-Citra withdrawals coming in smaller than the RM30 billion initially estimated by the EPF.

Disproportionate hit

When releasing 2Q2021 numbers, the EPF said about 89% of applicants under i-Sinar and 86% under i-Citra had stated that the money being taken out from their retirement kitty was used for daily expenses or urgent financial needs.

These Covid-19-related withdrawals also caused the number of people meeting the EPF’s Basic Savings threshold (RM240,000 at age 55 to have RM1,000 to spend a month for 20 years post-retirement) to drop from 36% to 27%. Some 5.8 million or 46% of 12.63 million EPF members below the age of 55 had less than RM10,000 in their account as at Aug 31, 2021.

“The pandemic also triggered a dramatic rise in the number of gig workers in the country, and while that has helped workers survive, many of these workers are falling back on their retirement security due to the irregular and unstable income. Additionally, they are facing vulnerabilities in terms of employees’ benefit and coverage on social protection. There will be far-reaching repercussions not only on their future well-being but also on the government, which will have to carry that financial burden,” Amir said in the statement, reiterating the need to have a coordinated solution for the long term to ensure better social protection for all Malaysians.

“As we recover from the crisis, the EPF’s focus is to help members restore and rebuild their retirement savings to ensure that they are able to secure a dignified retirement. We will remain focused on our strategic asset allocation and continue to be cognisant of the risk profiles of the markets as they develop so we are able to shift along the way. While we are doing that, our fundamental purpose of providing returns and protection for our members’ future well-being will continue to be preserved,” he added.

http://www.theedgemarkets.com/article/epfs-1h-performance-points-higher-2021-dividend