Market vulnerable to uncertainties in 2Q as valuation remains high

GLOBAL markets managed to keep relatively stable in the first quarter despite Russia’s invasion of Ukraine, which caught investors by surprise.

Coming on the heels of a nascent economic recovery in global markets, the war now poses an upside risk to inflation, fuelled by soaring energy prices and supply disruptions.

Analysts The Edge spoke to peg the Russia-Ukraine conflict as the key market determinant in 2Q and caution investors to be nimble in response to news flow. The reopening of Malaysia’s borders is expected to boost a number of sectors including tourism, aviation and retail.

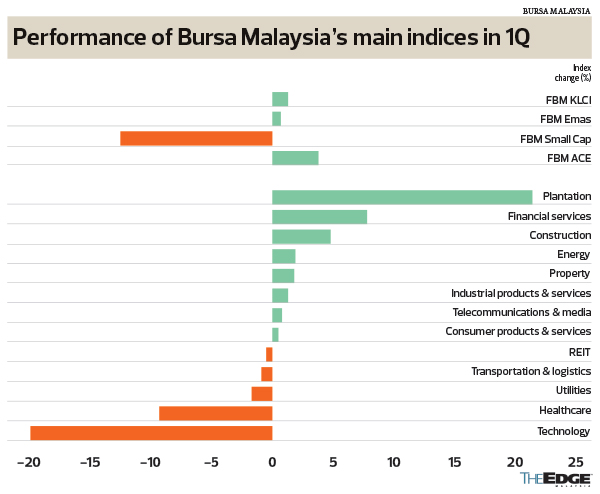

In the first quarter, Bursa Malaysia’s 13 sectors turned in mixed financial performances, with plantation the runaway performer (+21.4%), followed by financial (+7.8%) and construction (4.8%).

At the other end of the scale was technology (-19.9%), healthcare (-9.3%) and utilities (-1.7%).

The benchmark FBM KLCI ended the quarter with a 1.3% gain, against a 3.8% rise in small-cap stocks and a 12.5% decline in ACE Market stocks.

Against the backdrop of dealing with inflation, rate hikes and geopolitical uncertainties, PublicInvest Research head Ching Weng Jin says the risk has increased especially as the market has made robust gains since the pandemic.

“In terms of valuation, it is at the higher end. It doesn’t take much for the market to come off, [it] just needs a bit more fears and concerns, then the market will react in that manner. Definitely, it will be more volatile,” he tells The Edge.

As a result, he stresses that investors have to be very nimble in this news flow-driven market.

Loui Low, head of research at Malacca Securities, expects recovery theme stocks to be more actively traded because of the reopening of Malaysia’s borders.

“Most tourism stocks will benefit from the reopening of borders and they should gain momentum. It should be more positive for Genting Malaysia Bhd (GenM), Malaysia Airports Holdings Bhd (MAHB) as well as the aviation, consumer discretionary and REIT sectors.”

In the first four days of last week, shares in MAHB and Capital A Bhd gained 7.4% and 9.7% respectively, while GenM and Genting Bhd rose 0.7% and 0.6%.

Retailers Berjaya Food Bhd, Aeon Co (M) Bhd and Padini Holdings Bhd were up 5.3%, 3.3% and 4.9% each over the same period.

Low says the unresolved geopolitical tensions between Russia and Ukraine could exert more inflationary pressures because of elevated commodity prices.

“That will be the potential risk towards the second half (2H) and margin erosion might come in. Companies will still register growth in 2Q, but inflationary pressures will be closely monitored to gauge the ability to pass on costs to customers.”

He cautions that inflationary concerns may have a knock-on effect on consumer stocks in 2H.

Although the travel and food and beverage segments will reap the benefits of open borders, Ching says much still depends on whether it will translate into earnings for industry players.

Lee Chung Cheng, head of research at JF Apex Securities, expects to see more sideway trading in 2Q, with cost being a main concern for corporates. While the reopening of borders is positive for stocks under the recovery theme, he opines that the outlook remains tough for the aviation sector owing to soaring jet fuel prices.

“Quarter on quarter, corporate earnings may come in lower in 2Q. Because of rising raw materials and shortage of workers, most probably, it will hurt manufacturing and construction,” he cautions.

Banking, O&G and plantation stocks in focus

Last Thursday, oil prices slipped on news reports that US President Joe Biden’s administration was considering the release of some one million barrels of oil per day from strategic reserves for a few months to stem surging oil prices.

Low is of the view that crude oil and crude palm oil (CPO) prices will consolidate in April and May, but are unlikely to reverse to levels prior to the Russia-Ukraine war a month ago.

“As tensions still persist, crude oil and CPO should remain in a good position. Furthermore, lockdowns in China might weigh on demand for these commodities.”

He says plantation stocks could see another push ahead of the corporate results season in May. “Earnings are still strong and will support share prices after the consolidation phase, similar to what happened in February.”

Ching stresses that the situation in Ukraine will be very critical over the next couple of weeks. “If the war persists, there could be an embargo on Russian oil and prices will shoot up, given that Russia supplies 10% of global oil. If Russian President Vladimir Putin pulls back forces from Ukraine, then oil prices will reverse quickly.”

Brent oil was down 5.1% to US$107.68 a barrel as at 5pm last Thursday.

Lee projects that oil prices will continue to be resilient in 1H, but that contract flow among O&G firms will only get stronger in 2H, as oil majors await oil prices to stabilise in 2H before committing to capital expenditure spending.

As for CPO, he observes that some European nations have started using palm oil to address the shortage of sunflower and soybean oil. This, in turn, will support CPO prices at least in 1H before potentially tapering off in 2H.

Technology stocks are not out of the dumps yet, Low warns, as they may face another selloff on the back of interest rate hikes and geopolitical tensions. Despite growth in earnings, it remains to be seen if investors are willing to pay a premium for technology stocks.

“There could be another dip in technology stocks but it won’t be as severe as the recent one. They should be well supported for now,” Low says.

Over in the US, stocks listed on Nasdaq have proven to be susceptible to the rising interest rate environment. Ching notes that the valuation of Malaysian technology stocks are supported by strong earnings growth.

“However, as US technology stocks are more services-driven, they are susceptible to reduction in consumption. Their earnings are also more sensitive to rate hikes due to rising interest expenses.”

He advises investors to be more selective in picking technology stocks, especially those that have fallen sharply and with strong business models. His top picks are Inari Amertron Bhd and D&O Green Technologies Bhd, which will benefit from the 5G rollout and automotive LED segments respectively.

In the O&G space, Ching sees buying opportunities in Hibiscus Petroleum Bhd, a strong proxy to high oil prices. And in plantation, he prefers pure upstream players such as Sarawak Plantation Bhd.

“For those that have [a] downstream business, while they will benefit from high CPO prices, margins will be affected by their downstream business. On a net-net basis, they may not benefit as much as pure upstream players,” he adds.

US rate hike implication

Elaborating on the impact of US rate hikes, Low says the market will react positively if the number of rate hikes is lower than projected.

“My view is that seven times is a bit too many, but the market already expected that to happen. If it is more than seven times, it will spook the market and trigger a selloff.”

Given the rate hike expectation, banking stocks are being held out for their upside and may attract investors looking for yield play, says Low.

He reiterates the key risks in 2Q are prolonged Russia-Ukraine tensions, as well as inflationary pressures that could hit corporate earnings.

While banks are the beneficiaries of rate hikes, Ching cautions that if the global economy weakens, it will weigh on bank earnings as well. Likewise, demand in the O&G and plantation space may also slump should the economy soften.

Given that banking, O&G and plantation stocks have moved up recently, he notes that the risk-reward is skewed more towards the downside rather than the upside.

“A lot of uncertainties in 2Q. It is dependent on whether the war will end soon. Then we can focus on fundamentals and tackle inflation without any distractions. Right now, you have pressures on the demand side and supply side,” observes Ching.

Low highlights that a construction rally may take place should parliament be dissolved (in the event of a snap poll). Attention will turn to the political landscape when a memorandum on political transformation and stability inked between the federal coalition and the Pakatan Harapan opposition expires in July. “My view is that the election will only happen next year,” he says.

As the local bourse is a major laggard in the region, foreign funds have been nibbling and are net buyers of Malaysian equities this year, with a net inflow of RM6.12 billion, according to MIDF Research.

“This is partly due to the reorientation of funds into emerging markets because of what’s happening in the West. But bear in mind, it is very much hot money in Malaysian equities and not long-term investors who buy and hold,” Ching warns.

http://www.theedgemarkets.com/article/market-vulnerable-uncertainties-2q-valuation-remains-high

Singapore Investment

-

-

-

Big (Tech) Week17 hours ago

-

-

-

-

-

Reduced Exposure1 day ago

-

-

-

-

-

-

-

-

-

-

-

-

-

Portfolio (April 30, 2026)2 days ago

-

Portfolio (April 30, 2026)2 days ago

-

-

-

April 2026 Updates2 days ago

-

-

-

-

Month of April 20262 days ago

-

-

-

-

-

-

-

Portfolio at 283 days ago

-

-

-

-

-

-

-

-

-

-

-

SIA share price in trouble6 days ago

-

-

When the Market Humbles You.6 days ago

-

-

Quiet times1 week ago

-

Side Income Update 20251 week ago

-

-

-

-

-

Mapping China’s biotech titans1 week ago

-

-

Portfolio Returns for Apr 20261 week ago

-

-

-

-

-

Special Dividend Anyone?2 weeks ago

-

-

-

-

-

-

A Case for Mindful Consumption3 weeks ago

-

-

-

-

1Q 2026 Investment Strategy Update4 weeks ago

-

Portfolio -- Mar 20264 weeks ago

-

Some thoughts on my portfolio4 weeks ago

-

-

March 20265 weeks ago

-

-

Farewell careyourpresent.com1 month ago

-

-

-

A new year, a new workplace, a new start2 months ago

-

-

-

-

-

Weekly Flow show report, Feb 15 20262 months ago

-

-

-

-

The 2026 HDB “MOP Wave” & Upgrading Strategy3 months ago

-

Cory Diary : Family Expense Dec'253 months ago

-

-

-

Best Countries to Invest in 20263 months ago

-

-

FG Year in Review 20254 months ago

-

Restarting on Substack...4 months ago

-

-

-

Loopholes Singapore is on YOUTUBE!5 months ago

-

What Shall We Do About VERS?5 months ago

-

-

-

-

-

-

-

Been a while!8 months ago

-

-

-

-

-

-

-

-

FAQ on Quantitative Investing Part 21 year ago

-

-

-

-

-

-

Top 10 Highlights of 20241 year ago

-

-

STI ETF1 year ago

-

-

-

Unibet Casino Bonus Codes 20241 year ago

-

-

-

-

Monthly IBKR Update – June 20241 year ago

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Monthly Summary of November 20232 years ago

-

Migration of website2 years ago

-

-

-

-

-

Hello SP Group, I'm Back!2 years ago

-

-

-

A New Light2 years ago

-

-

-

-

2022 Thoughts, Hello 2023!3 years ago

-

Series of Defaults for Maple Finance3 years ago

-

Takeaways from “Sea Change”3 years ago

-

Greed is Coming Back3 years ago

-

-

-

-

-

-

-

-

What is Overemployment3 years ago

-

Terra Hill Condo (former Flynn Park)3 years ago

-

Alibaba VS Tencent: The Battle Royale3 years ago

-

-

-

-

-

-

-

-

-

-

-

-

-

Home

AEON

AIRPORT

BJFOOD

BURSA

CAPITALA

D&O

FBMKLCI

GENM

GENTING

HIBISCS

INARI

PADINI

reit

SWKPLNT

Market vulnerable to uncertainties in 2Q as valuation remains high