2020

came and went. Whilst it is a watershed year, it is nonetheless a year

that investors in the stock market will never forget. Apart from myself,

many have studied, analysed and commented on the glove sector including

specific glove companies. Amongst all sectors, the glove sector is the

most crowded in terms of analysis and scrutiny. After all, it is a

uniquely Malaysian Cinderella story. I have read many wonderful

observations & analysis, am thankful for the sharing. I can tell

from the articles, voluminous amount of work have been done by fellow

writers. There is one author I particularly fancy, Ben Tan. The amount

of detail and work done is impressive.

As per my past writing, my favourite Glove stocks which I deemed are long term value stocks would be Riverstone Holdings Ltd, Hartalega Holdings Berhad and Sri Trang Agro. Each of these stocks are listed respectively on SGX, Bursa and SGX / SET (dual listed). Rest assure, this article is not about their wonderful results and record breaking earnings or cash position. Instead, I will spent this article mostly showing readers the performance of the stock price in the past 1 year since the start of the pandemic, towards its peak and its selldown.

1. Riverstone (Adjusted for 1 for 1 bonus)

2. Hartalega

3. Sri Trang Agro Industry PCL

For ease of reference, I took the stock price of each glove companies from mid April to today's closing market price.

- Riverstone rose from SGD 62 sens to SGD 1.31 - An increase of 111%

- Hartalega rose from RM 7.25 to RM 9.41 - An increase of 30%

- Sri Trang Agro rose from THB 11.70 to THB 48 - An increase of 310%

How about the profits and cash position increment for each of this company?

- Riverstone revenue rose 85%, net profit rose 396%, dividend rose 6X and cash position rose 398%

- Hartalega revenue rose 123%, net profit 536%, dividend rose 6X and cash position rose 1211% (conservative estimate using similar revenue (RM6.5 billion), net profit (RM 2.76 billion), dividend (48 sens) and cash position (RM 4 billion) based on Q3 FY 21

- Sri Trang Agro revenue rose 25%, net profit rose (loss of THB 149 million to THB 9.5 billion), dividend rose 5x and cash position rose 1010%.

Because

the companies have different reporting timeline, so it is hard to

compute full year results as comparison. However, based on what I

provided above, record results (best have yet to come, likely the next

quarter), you can use it as a gauge to compare the valuation vs the

current share price. Well, surely seasoned analysts or those with

contradicting view will surely argue, 2020/2021 is a one off event due

to the century pandemic. Hence, must discount it and not factor the

calculation in such manner. Also must compute it against 2022 or even

2023. This is where I would like to point out an important distinction

which some failed to appreciate.

Every stock

has a company behind it, and every company has an intrinsic value. The

intrinsic value is what determine what the company is worth. In essence,

the stock price is a manifestation of the intrinsic value. The argument

then lies with how to compute the intrinsic value. Of course, it is

somewhat a mixture of science and art. One thing is for sure and most

would agree, an important metric to look at is earnings. For me, to

know the intrinsic value, it is important to value the company based on

(Assets - Liabilities = Equity) + Ability to earn / grow profits +

Ability to sustain profits + Ability to pay dividends. Apart from that,

Retained Earnings which is part of Equity is an aspect that is

overlooked by investors. In short, we can conclude the higher the

company's retained earnings, the more valuable the company is. This is

in fact, highlighted not by me, but by Warren Buffet in his recent

Annual Letter to Berkshire Shareholders 2021. You can read this passage

here -

So

this is where I would like to draw your attention. Whenever I read

articles saying "gloves are overvalued", I am often bemused by the

ignorance of individuals who make such shallow comments. The value of

a company does not diminish or gets eradicated once supernormal profits

disappears. This is simply because when a company makes profits, the

profits translate to retained earnings and of course the retained

earnings can then be used for other things like paying dividend,

investments or future capital expenditure. The supernormal profits may

reduce like how Covid-19 reduces but the value of the company does not

reduce unless it starts making losses overnight. The higher the profit,

the higher the retained earnings, the higher the value of the company.

In essence, the company's value holds itself and that is why share

price maintains at a certain level. Even if next year or following year

the earnings fall, the value built and accumulated do not get wiped out

unless the retained earnings are deployed egregiously resulting in

losses to the company. It is absolutely wrong to equate the share price

chart of gloves, to the Covid pandemic infection & death rate chart

in direct correlation and absolute terms.

Owens

& Minors is one of the notable PPE maker and supplier in US. It has

a history of over 100 years. Despite the vaccine roll out and all the

talks of pandemic being over, the share price continue to perform and

sustain in tandem with the earnings. This is due to the structural

change and hygiene behaviour pattern following Covid-19. Investors are

knows the importance of such company now and appreciates its retained

earnings, future earnings visibility and accord it higher value compared

to before. None is rushing to take profit the way it is happening in

Bursa. In fact, the performance of Owen & Minors shows the major

flaw in the thesis of a Foreign IB research report.

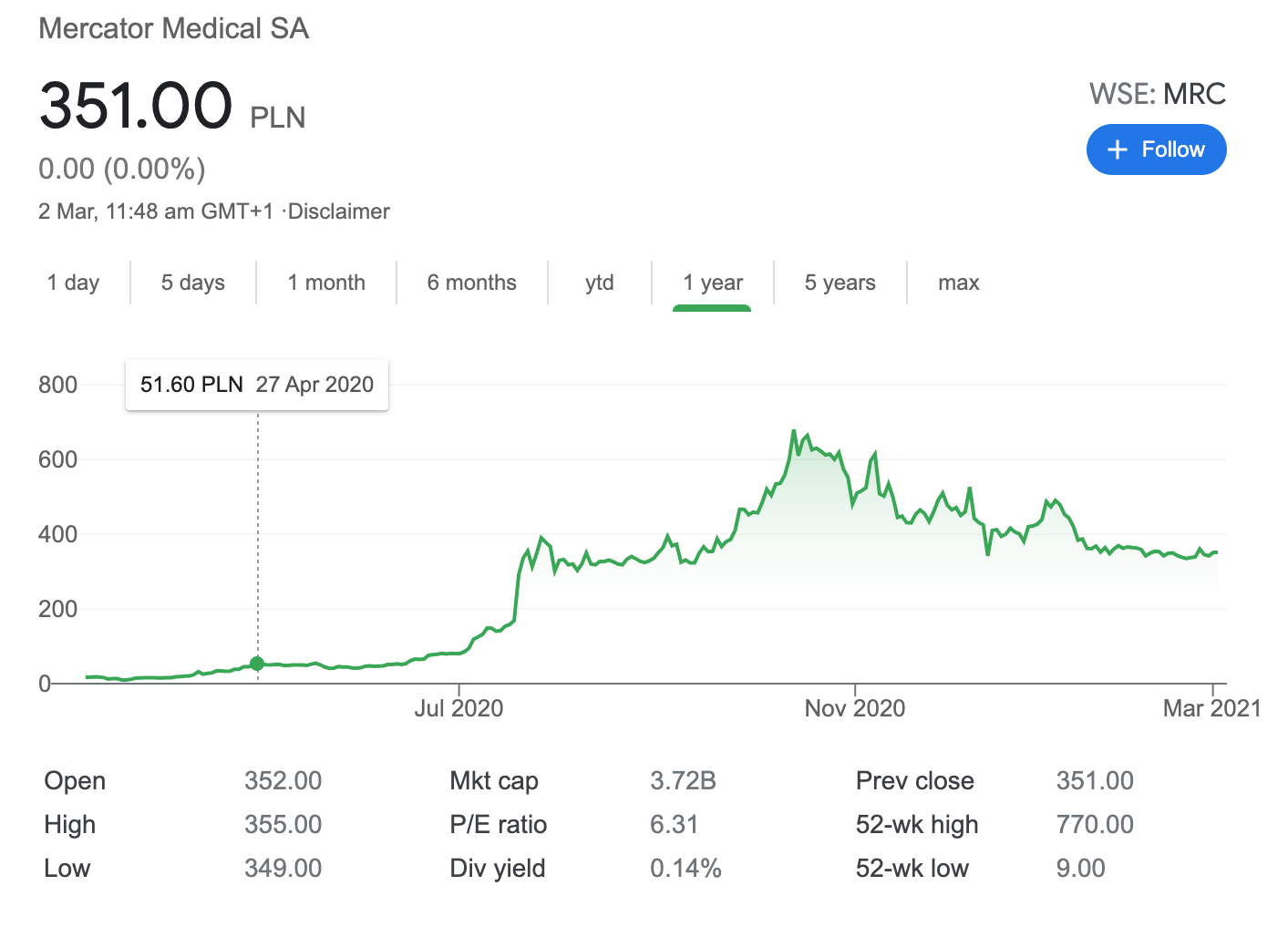

Mercator

Medical, the superstar polish glove maker that rose to fame on the back

of the pandemic is still 7X its stock price back in April 2020 and

sustaining well even after falling from the peak of PLN 770 to what it

is today. We must remember, Mercator unlike our Big 4 did not even enjoy

the same level of global reputation and standing yet it is sustaining

much better than the price action of our local glove makers.

Intco

Medical needs no introduction anymore. It is one of the top two glove

players in China which have recently came on the news touting to build

190 billion glove capacity factory in the coming years. As a background,

Intco traditionally is a vinyl glove maker and one of the largest in

the world. Vinyl gloves are also known as "poison plastic". Seeing the

demand and value paid for nitrile gloves, Intco is venturing big and

even raising US 1 Billion on a secondary listing in Hong Kong to achieve

this. Although its capacity is only 20+ billion now with more than 60%

production in Vinyl gloves, the stock price have continue to risen and

sustained very well. To put things into perspective, Intco Medical

market cap today is bigger than Top Glove and Hartalega. It is also

bigger than Supermax + Kossan + Riverstone + Comfort + Careplus + UG

healthcare combined. Is Intco medical such a good glove player and ours

so inferior to China’s glove maker? Does this make sense?

Looking

at the stock price performance of other glove makers which have been

through a superb record shattering 2020, for the stock price to revert

almost back to where it was despite the profits, cash and balance sheet

strength defies logic. The irrationality and emotions flooding the

market is not only retail investors. In fact, I think the retail

investors in Malaysia have done very well and held on to the conviction

in the face of huge RSS selling, institutional selling. I take my hats

off to them as it is extremely tough to go up against such adversity. The age old adage which states, "the market can stay irrational longer than you can stay solvent" is absolutely true.

Zoom was one of the hottest tech stock which captured everyone attention due to the pandemic too. It was the poster boy of pandemic so much so the stock itself went up 7 times to a peak of US 588 with a market cap US 172 billion. It even helped Li Ka-Shing recapture his title of Hong Kong's richest despite the impact that rampage through his notable companies CK Hutchinson, CK Assets and others. Why I am sharing this is to show you even though Zoom was regarded as the face of Covid-19 beneficiaries due to the work for home need for video conferencing, it still managed to stave off the plunge when the vaccine was developed and funds rotated towards recovery plays. Even outside of the sector, stocks like this can retain its value due to the "new normal" and "value of the company" which was brought to light resulting from the pandemic. Otherwise, Zoom may still take its time to jostle for attention of major funds and investors.

One

of my favourite boxing movie is Cinderella Man, by Russell Crowe. It is

based on the real life story of James Bradock who was injured and had

to work in the docks during the Great Depression just to survive. He

returned to competitive boxing in order to make a living for the family

during the most challenging time and despite being an underdog, he rose

to the occasion to dethrone the incumbent and became the heavyweight

champion. His nickname was the "Cinderella Man". The glove makers in

Malaysia are tales of Cinderella, rags to riches and underdogs to world

domination. It took 30 years to get to where they are. When the time

came for them to rise to the occasion, they performed and delivered

extraordinarily.

History have shown, whenever the glove sector retraces, it has never gone back to previous low and it forms a higher low each time. However, most people painted doomsday scenario such as price war and oversupply yet in the end the sector prove them time and time again they were wrong. Indeed, China capacity may be scary but ultimately they don't have the expertise. In terms of efficiency, our glove makers still have at the upper hand. Glove making especially Tier 1 quality is not as simple as making mask. As for the US wanting to build their capacity, at the first place back in the days, their manufacturers chose to disposed all these assets as they they find it low value in nature and could not compete hence adopting the OEM model.

History have shown, whenever the glove sector retraces, it has never gone back to previous low and it forms a higher low each time. However, most people painted doomsday scenario such as price war and oversupply yet in the end the sector prove them time and time again they were wrong. Indeed, China capacity may be scary but ultimately they don't have the expertise. In terms of efficiency, our glove makers still have at the upper hand. Glove making especially Tier 1 quality is not as simple as making mask. As for the US wanting to build their capacity, at the first place back in the days, their manufacturers chose to disposed all these assets as they they find it low value in nature and could not compete hence adopting the OEM model.

I

believe investors need to ask themselves what is their investment

horizon, ability to hold (no margin, no leverage) and stomach the

emotional rollercoaster. I do not deny sentiment plays a part in

investing. Herd mentality, fear and greed swings share price. However,

as a true fundamentalist, I invest based on the value I see in the

company. I have great faith in Riverstone and Hartalega for the reasons I

have shared before and have a long investment horizon. Ultimately,

investors must know the value of the company behind the stock price in

order to determine the best course of action.

_______________________________________________________________

Telegram channel : https://telegram.me/tradeview101

Website / Blog : https://www.tradeview.my/

Facebook : https://www.facebook.com/tradeview101/or

Email me to sign up as private exclusive subscriber : tradeview101@gmail.com

Food for thought:

https://www.tradeview.my/2021/03/tradeview-2021-should-investors-take.html

1