BAT (4162) - BAT’s FY16 profit growth seen to be flattish at 0.4%

By Kenanga Research / The Edge Financial Daily | April 30, 2015 : 10:56 AM MYT

British American Tobacco (M) Bhd (BAT)

(April 29, RM67)

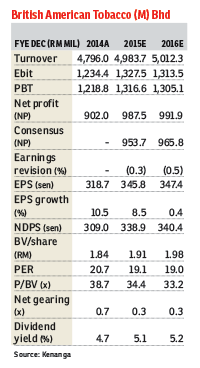

Maintain market perform with a target price (TP) of RM67.40: BAT’s revenue rose 10.4% to RM1.3 billion year-on-year for the first quarter ended March (1QFY15), despite a 0.4% decline in domestic and duty-free volume, thanks to the 12% to 14.3% excise duty-led price increase in November 2014. However, higher operating expenses (22.5%) translated into slower growth in operating profit of 7.6%, mainly due to the timing of the recognition of marketing expenses. As a result, net profit grew 8% to RM243.4 million.

Quarter-on-quarter, revenue grew 5.7%, reflecting the full effect of the price increase in November last year, which was also aided by the stocking up activities in March before the goods and services tax (GST).

Operating expenses shrank 28.9% compared with the previous quarter again due to the timing of the recognition of marketing expenses. With that, net profit was 24.5% higher compared with 4QFY14, further helped by the normalisation of the effective tax rate (25% versus 29.5%).

The industry volume decline of 0.9% was lower than the 3.5% we are assuming, probably due to the pre-GST buying in anticipation of higher prices as well as the enforcement efforts by the authorities.

However, the latest study shows that the illicit market share recovered to 32.8% in 4QFY14 from 32.3% in 3QFY14. Thus, we conservatively think that the mild rate of decline in the industry volume might not be sustained moving forward.

We maintain our “neutral” stance on the stock as the company has continued to deliver earnings on the back of declining volume as well as persistent weak local consumer sentiment. On the flip side, with regards to the Anti-Profiteering Act, we do not expect to see another round of price increases (which is the attractive selling point of BAT) until 3QFY16. Thus, net profit growth in FY16 is forecast to be flattish at 0.4%.

We made housekeeping changes to our earnings forecast after updating the annual report figures. As a result FY15 to FY16 estimated net profits were revised downward by 0.3% and 0.5% respectively.

We roll over our valuation to FY16E and derive a lower TP of RM67.40 (previously: RM69.40), based on a lower price-earnings ratio of 19.4 times (from 20.5 times), which implied a five-year mean instead of +0.5 standard deviation five-year mean.

We opt to be more conservative on valuation as the results of the enforcement are not as good as initially expected, while the recent reversal of price increases post-GST has also cast a doubt on the appeal of BAT being the dominant player in the industry.

Risks to our call are the increase in excise duty or taxes and worse-than-expected enforcement efforts by the authorities. — Kenanga Research, April 29

http://www.theedgemarkets.com

By Kenanga Research / The Edge Financial Daily | April 30, 2015 : 10:56 AM MYT

British American Tobacco (M) Bhd (BAT)

(April 29, RM67)

Maintain market perform with a target price (TP) of RM67.40: BAT’s revenue rose 10.4% to RM1.3 billion year-on-year for the first quarter ended March (1QFY15), despite a 0.4% decline in domestic and duty-free volume, thanks to the 12% to 14.3% excise duty-led price increase in November 2014. However, higher operating expenses (22.5%) translated into slower growth in operating profit of 7.6%, mainly due to the timing of the recognition of marketing expenses. As a result, net profit grew 8% to RM243.4 million.

Quarter-on-quarter, revenue grew 5.7%, reflecting the full effect of the price increase in November last year, which was also aided by the stocking up activities in March before the goods and services tax (GST).

Operating expenses shrank 28.9% compared with the previous quarter again due to the timing of the recognition of marketing expenses. With that, net profit was 24.5% higher compared with 4QFY14, further helped by the normalisation of the effective tax rate (25% versus 29.5%).

The industry volume decline of 0.9% was lower than the 3.5% we are assuming, probably due to the pre-GST buying in anticipation of higher prices as well as the enforcement efforts by the authorities.

However, the latest study shows that the illicit market share recovered to 32.8% in 4QFY14 from 32.3% in 3QFY14. Thus, we conservatively think that the mild rate of decline in the industry volume might not be sustained moving forward.

We maintain our “neutral” stance on the stock as the company has continued to deliver earnings on the back of declining volume as well as persistent weak local consumer sentiment. On the flip side, with regards to the Anti-Profiteering Act, we do not expect to see another round of price increases (which is the attractive selling point of BAT) until 3QFY16. Thus, net profit growth in FY16 is forecast to be flattish at 0.4%.

We made housekeeping changes to our earnings forecast after updating the annual report figures. As a result FY15 to FY16 estimated net profits were revised downward by 0.3% and 0.5% respectively.

We roll over our valuation to FY16E and derive a lower TP of RM67.40 (previously: RM69.40), based on a lower price-earnings ratio of 19.4 times (from 20.5 times), which implied a five-year mean instead of +0.5 standard deviation five-year mean.

We opt to be more conservative on valuation as the results of the enforcement are not as good as initially expected, while the recent reversal of price increases post-GST has also cast a doubt on the appeal of BAT being the dominant player in the industry.

Risks to our call are the increase in excise duty or taxes and worse-than-expected enforcement efforts by the authorities. — Kenanga Research, April 29

http://www.theedgemarkets.com