Thong Guan has again released a set of superb quarterly result. Being one of the shareholders, i'm very very pleased with Thong Guan.

I will not go into the Triple-Excellent grade balance sheet which have already been discussed in my earlier articles.

But i would like to point out several key findings that i extracted out from the income statement and trying to guesstimate what is going to happen to Thong Guan in near future.

Key Observation:

1) Thong Guan has commissioned its first unit of 33-layerNano Film in mid of 1st quater 2016.

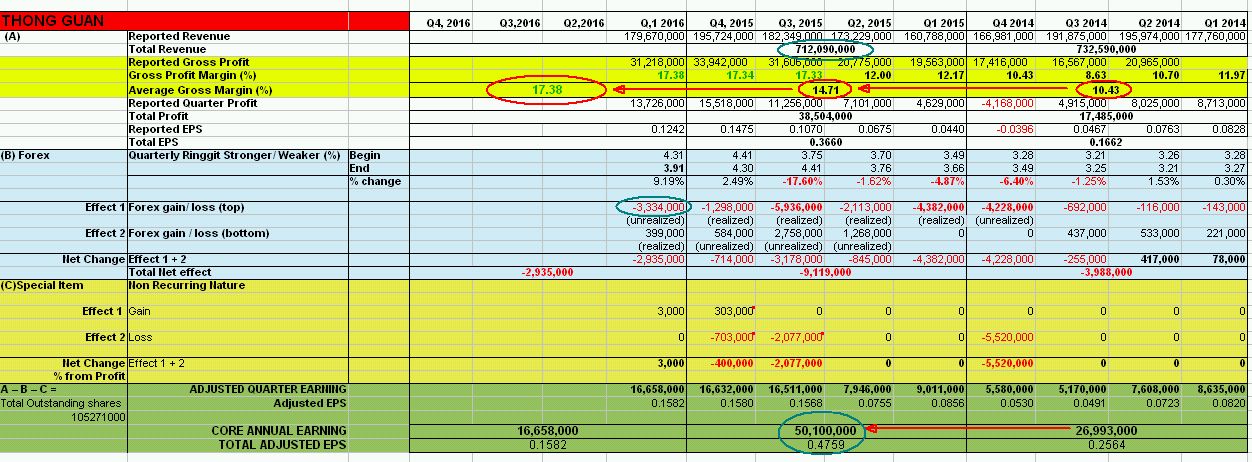

2) Look at the gross margin of Q1 2016, it is at 17.38% compared to average of 14.7% in 2015 and 10.4% in 2014. This gross margin is one of the important key to the success in Thong Guan RM 100 mil expansion plan where thong guan is targeting to continue generate value to its customers . Please also take note that 17.38% is a mixture of old machine (75%??) + new nano layer machine (25%??), I'm expecting the gross margin to go higher when more customers switch to nano film for savings. Plus, one additional new 33-nanolayer machine in pipeline.

3)With new 33 layer Nano Tech Machine, I hope Thong Guan able to achieve average of 18% or above gross margin in view of the new machine has just started running in mid of 1st Q 2016, raw material cost is still very low making plastic product a favaurable choice, Ringgit is weaken and weaken to propel the export.

4) Let assume that 2016 Thong Guan Revenue remained flat as per 2015 (RM 712 mi), the 2.67% gross margin (17.38 - 14.71) is potentially adding RM 19 million per year to the total profit or +18 sen EPS to 2015 total EPS. (2015's 37sen + 18 sen = 55 sen EPS <= Target 2016 total EPS). If average gross margin can hit 18% ( probably the only 33-layer Nano Machine in Asia), additional 3.29% gross margin is potentially additing RM 23.4 million or 22 sen EPS per year to annual profit. (2015's EPS 37 sen + 22 sen = 59 sen EPS <= Potential)

5) Thong Guan's 10% capacity expansion plan is still on going. Compared Q1 2016 vs Q1 2015, the revenue has increased for about 12%. Let be aggressive to use 10% revenue increment of 2015 RM 712 mil again, a 10% increase to 2015 revenue is RM 783.2 mil. With 2.67% to 3.29% additional margin, it potentially up the profit by additional 21 million to total of RM 59.5 million (or 56.8 sen eps) to additional 26 mil or RM 64.5 million (@ 61.2 sen eps) for full year 2016.

6) The above results are all excluding expansion that going on in the FOOD & Beverage Segment. In the latest quarter report, Thong Guan highligted that the capacity expansion is done. By looking at the numbers, the contribution of the noodle segment is still not obvious. Perhaps a bigger significant contribution can only be seen when JV with COFCO is materialized.

7) 2015 is a year with forex fluctuate a lot. 2016 should be relatively stable. I have tabulated the CORE NET PROFIT of Thong Guan. RM 60 million of full year 2016 is kind of possible if the forex losses of 9 mil do not repeat again in 2016.

All in all, being a shareholder of Thong Guan, I'm not only optimistic, but also excited about prospect of Thong Guan in very near future.

Cheers,

YiStock

Note: I again have comment regarding below:

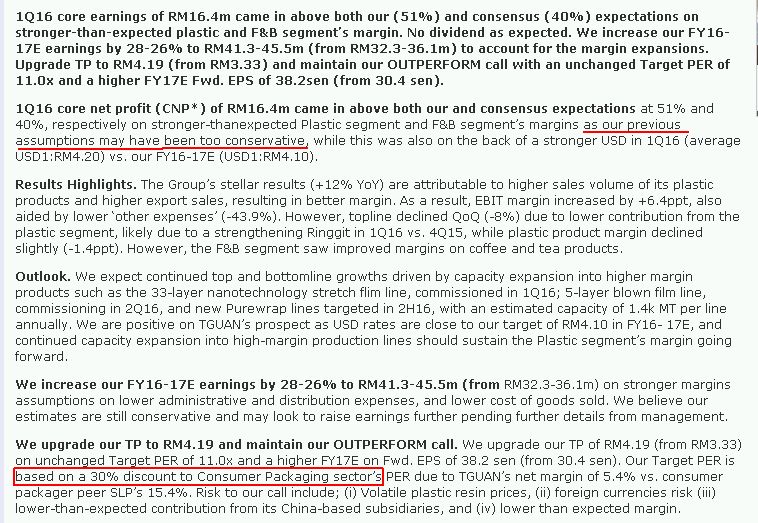

1) indeed the previous assumption is too conservative.

2) Still the 30% discount? I'm an small investor that looking for "return". Thong Guan TTM EPS is currently at 44.6 sen per share. It means that every RM 1.00 i invested, i earn 44.6 sen (Par Value RM1). SLP EPS is 45.16 (Par Value 0.25 x 4 = RM 1). Both earn same amount of money and likely Thong Guan is going to earn more money. I think they should trade at same PER.

TGUAN (7034) - Thong Guan - Growth Trajectory (8)- YiStock

http://klse.i3investor.com/blogs/thongguan/97471.jsp