Hi All,

i wrote about above topic as per below link:

http://klse.i3investor.com/blogs/thongguan/90695.jsp

Thereafter, i did not dig further into it. Untill recently i saw a post talking about Resin by a blogger from mr. KCCHONG's class. I find it a very important piece of information. Subsequently, the post was removed.

Anyway, i managed to contact that person and get a copy of the write up. With his permission, i will cut and paste some of the important key points. Reason is because a forummer has raised a "warning" on possible impact of the rising Oil Price and Ringgit to Thong Guan. i find this caution is important because i have the same doubt before.

To share my understanding about the above doubt, i will split into PART A (resin) & PART B - currency (again)

PART A: Resin

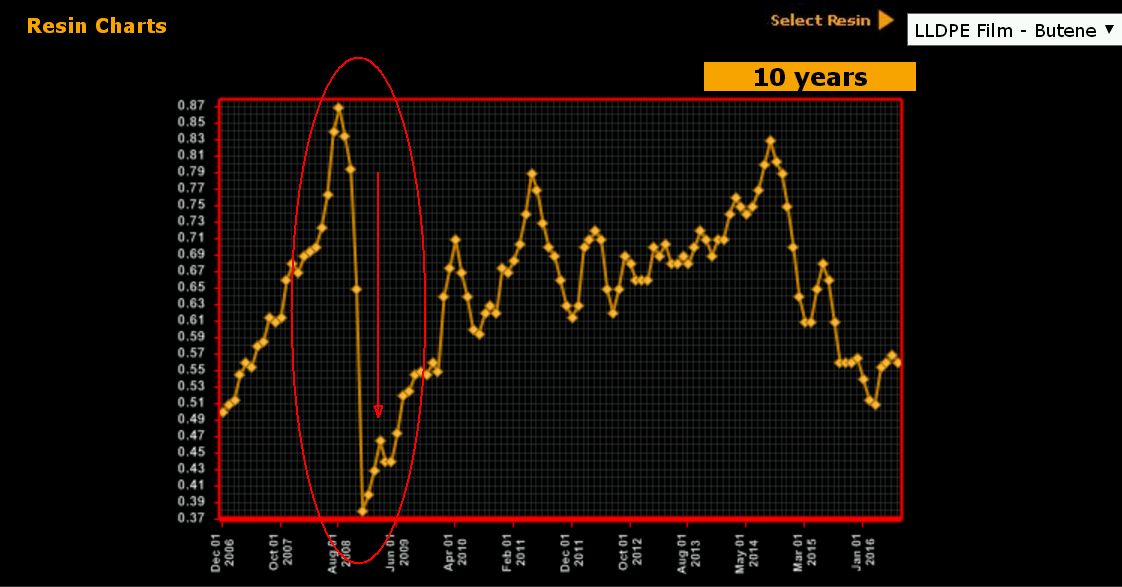

Now, it has been widely assumed that resin price is well related to crude oil. The relationship was rather strong, at least till, 2012. Resin price is important, because almost 80% of Tguan cost is resin.

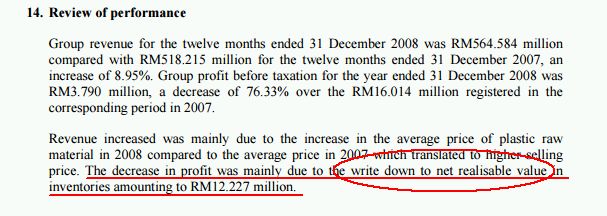

To see how great the relationship was, you might want to search back Tguan's quarterly report back in Q4, 2008. This is the only quarter for the past 10 years that suffer loss, RM 10.1 million. The main reason for the loss was due to oil price plunged which indirectly causing the pluged on resin price.

How is this net realisable works? Well, i think basically it is like you bought the Resin at X price in early 2008, then due to the sudden resin market price crash of more than 50%, so the resin now is worth (X - 50%). It is "vapourised" just like that. Such loss is not recoverable.

Below is the cut and paste:

Based on above piece of important information:

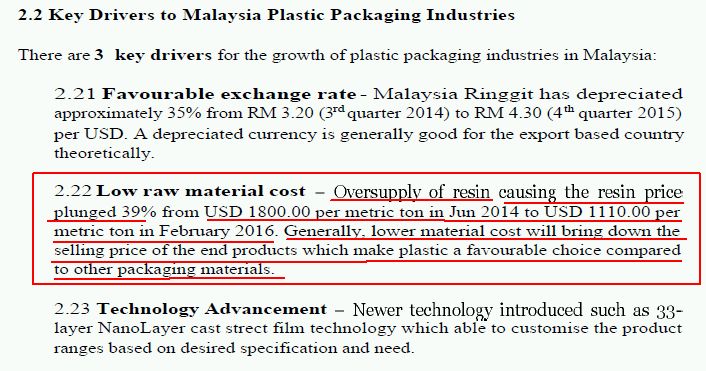

1) Over supply issue will likely be there for long long time. ThongGuan and other players will continue to enjoy low raw mat cost. Need to note that Thong Guan selling price is closely associated with resin price, higher resin price = higher selling price. Lower resin price = lower selling price.

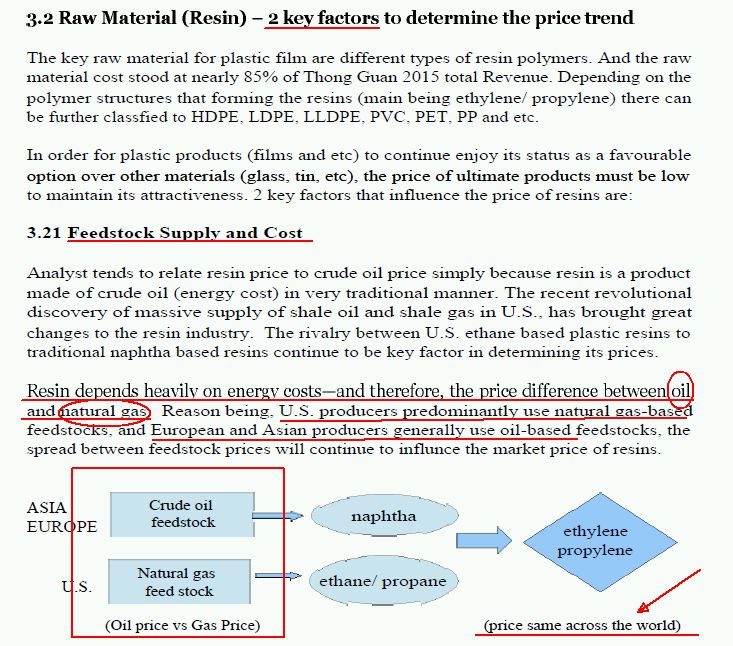

2) resin price is no longer link closely to crude oil price, but i assume it is now closely associated with natural gas price because US resin player has the advantage now. The margin of Asia resin player maybe squeezed due to recover of oil price. Remember, there is only one standard resin selling price accross the world.

3) "rising oil price" is no longer a concern to Thong Guan. Perhaps investor should start tracking natural gas price.

For those who are interested to have many good piece of information, you may want to join Mr KCCHONG's class. There are many good research report in the group.

PART II: RINGGIT

I want to talk about this again as i find that currency fluctuation is one of the key in analysing a good export based company. My reason are simple:

1) Poor Ringgit has resulted in many beutiful financial ratio in many export based companies for the past few years. This is what i call 饮水要思源。

2) If it is not important, one will not seen the words " ...due to favourable exchange rate...." keep appearing in the quarter reports and long tedious explaination on currency risk / exposure in foregn currency in Annual reports.

Back to the point, about currrency, I recently think of another important criteria in analysing an export based company, in particular, the destination/ geographical location.

Again, this is just my own theory and may not represent the vast market, or actual situation.

You see, whenever, Ringgit turn strong, some people get worry, they worry the export business will drop.

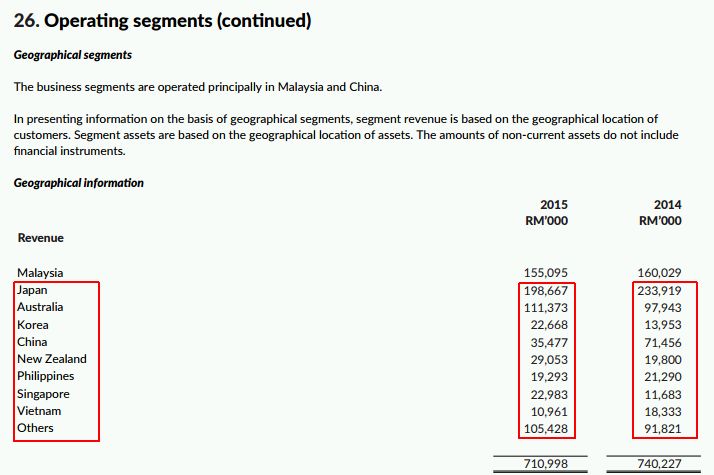

Is this the real case? Let see below example of Tguan customer location. Japan still the largest, followed by australia.

We all know that in Q1 2016, USD has depreciated nearly 9.1% against MYR (ringgit turned strong)

This sounds bad for Tguan or other export based companies.

However, if you are a client of Tguan and currently Import Tguan's product into Japan and Australia. During the 1st Q of 2016, your JPY and AUD has also appreciated by 6.6% and 5.1% respectively. A stronger JPY and AUD make the purchasing power stronger.

The "net impact" is therefore, export to JPY is 9.1% - 6.6% = 2.5% different @ export to AUD 9.1% - 5.1% = 4.0% different. Actually not so bad.

So, the next time when you see ringgit get strong by 10%, perhaps you also want to see from Client's perspective too.

What else?

Below is the USD/JPY price chart, notice that Q2 2016 JPY get strong again by another 7.1% so far?

What will be the impact?

Ringgit has weaken by 6%

Where are the opportunity in Q2 2016?

7.1% + 6.0% = 13.1% <= net impact!

This give a lot of space for imagination.

Cheers!

YiStock

Note: I think i have wrote too much about Thong Guan, but there are simply too many thing to look at when investing in a company. I'm thankful to members of KC Group to provide guidance on many companies. I missed the recent meet up in johor due to busy schedule. I will try catch up the next one.

TGUAN (7034) - Thong Guan - Rising Oil Price and Ringgit A Worrying Sign to the Bottom Line? (PART II) (9) -YiStock

http://klse.i3investor.com/blogs/thongguan/98542.jsp