1. Introduction

CIMB used to trade as high as RM8.70 back in May 2013. It is currently trading at RM4.29 (down 51%).

The downtrend was caused by decline in profitability. In 2013, CIMB reported net profit of RM4.54 billion. In the latest financial year, its profit had declined by 40% to RM2.85 billion.

Annual Result:

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | PE | DPS (Cent) | DY | NAPS | ROE (%) |

|---|---|---|---|---|---|---|---|---|

| 2015-12-31 | 15,395,790 | 2,849,509 | 33.62 | 13.51 | 14.00 | 3.08 | 4.8100 | 6.99 |

| 2014-12-31 | 14,145,924 | 3,106,808 | 37.48 | 14.84 | 15.00 | 2.70 | 4.4400 | 8.44 |

| 2013-12-31 | 14,671,835 | 4,540,403 | 59.97 | 12.71 | 23.82 | 3.13 | 3.9200 | 15.30 |

| 2012-12-31 | 13,494,825 | 4,344,776 | 58.45 | 13.06 | 23.38 | 3.06 | 3.8100 | 15.34 |

The stock looked interesting as it is currently trading at Price to Book Ratio of 0.88 times. A banking group like CIMB should trade at at least 1.5 times when its earnings recovers.

(When come to banking stocks, the Market has been quite fair and rational. The higher the ROE, the higher the valuation multiples).

The purpose of this article is to try to understand what are the major factors dragging down CIMB's earning in recent years and to try to have a feel of whether it will be turning around soon.

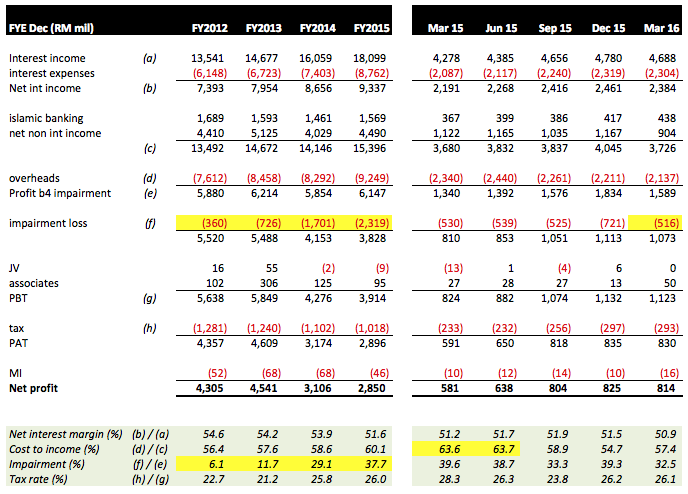

2. Historical Profitability

Key observations :-

(a) Loan impairment was the main reason CIMB's performance deteriorated over the years. In FY2012 and 2013, impairment charges were 6.1% and 11.7% of profit before impairment respectively. However, in FY2014 and 2015, it increased to 29.1% and 37.7% respectively.

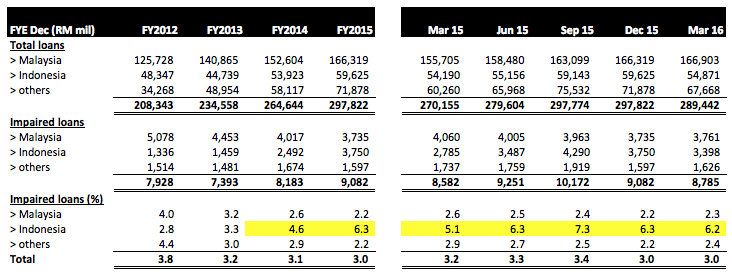

(b) Indonesia subsidiary CIMB Niaga accounted for the bulk of the bad loan spike.

As shown in table above, in FY2012 and 2013, only about 3% of CIMB Niaga's loans were impaired. However, in FY2014 and 2015, that has increased to 4.6% and 6.3% respectively.

Compared to Indonesia, Malaysia and other regions had been managing their loan books pretty well with impairment of 2% plus in FY2014 and 2015.

According to the company, collapse of commodity prices was the main reason for the spike in Indonesia bad loans. Indonesia relied quite heavily on commodity export. The downturn caused many borrowers to get into difficulties.

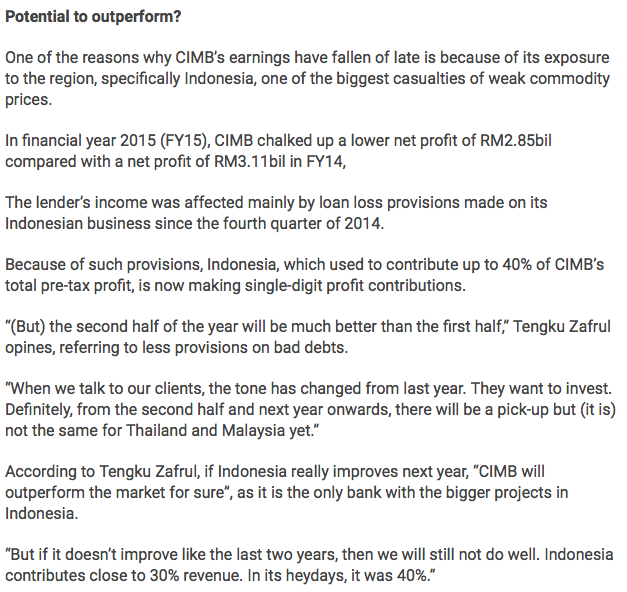

(c) In a recent interview with The Star, the CEO of CIMB expects Indonesia operation to perform better in second half of 2016.

(d) To improve performance, CIMB launched a campaign in 2015 called T18 (Target 2018) to revamp its operation. Among the measures put in place is reduction in overhead. The group's Cost to Income ratio has inched up in FY2015. The group targets to bring it down to 50% by 2018 (The group retrenched more than 3,000 employees in 2015 through a Mutual Separation Scheme).

3. Concluding Remarks

(a) By virtue of its 0.88 times PBR, I believe that CIMB is undervalued at current price of RM4.29. However, re-rating will only happen if its earnings improve.

(b) As mentioned above, the main reason the group's profitability has declined so much is because of non perfoming loans of its Indonesia subsidiary. After going through two rough years, there are signs that the Indonesian economy is gaining strength. CIMB's CEO has hinted of better performance in second half of 2016. Will that materialise ? We can only find out over time.

(c) The reason I invest in CIMB is because I believe it has limited downside. I do not have high expectation for this stock. If it can deliver 20% return for me by end of 2016 (Target Price of RM5.20), I will be very happy.

CIMB (1023) - (Icon) CIMB - Undervalued, But Patience Required

http://klse.i3investor.com/blogs/icon8888/100751.jsp