This article first appeared in The Edge Financial Daily, on July 18, 2016.

STOCKS in Malaysia had a roller-coaster ride over the first half of the year (1H16) as the market reacted to concerns about ringgit depreciation, oil price declines, possible interest rate hike by the US Federal Reserve, the health of the Chinese economy and risks of a global recession. Malaysian companies’ 1H16 profits also disappointed, leading to further earnings cuts. The benchmark FBM KLCI lost about 6% of its value to 1,600.92 in 21 days in January as investors were unnerved by steep falls in Chinese equity markets. The index has somewhat recovered since then, moving to 1,727.99 points on April 15 and closed at 1,668.40 last Friday. As the market enters 2H16, Meena Lakshana and Yimie Yong took a look at how the 10 stock picks The Edge Financial Daily featured on Jan 4 fared in 1H16 and whether the analysts’ views remain unchanged.

Sunway Construction Group Bhd

SUNWAY Construction Group Bhd (SunCon), which was seen as the best proxy to the construction sector this year underpinned by a strong infrastructure pipeline, had seen its share price climb 21% this year to close at RM1.65 last Friday, with a market capitalisation of RM2.13 billion. Its strong outstanding order book of RM5 billion, which translates into 2.6 times of its revenue in the financial year ended Dec 31, 2015, and expectations of more public infrastructure projects to be rolled out are keeping SunCon on TA Securities’ list of stock picks, with a target price of RM1.80.

In a recent report, TA Securities expects SunCon to win as much as RM2.5 billion worth of jobs this year. This is supported by internal construction jobs of RM500 million to RM800 million a year (from Sunway Group) as bedrock orders.

The research firm also pointed to SunCon’s cash-rich balance sheet. The group has a net cash position of 23 sen per share.

With the current net cash position and limited capital expenditure requirement, there is a potential upside to its dividend payout going forward, said TA Securities. “Based on its minimum dividend payout of 35%, we expect SunCon to offer reasonable dividend yield of about 3%.”

However, SunCon’s earnings did not fare well in the first quarter ended March 31, 2016, falling 15.5% to RM29.06 million. Its revenue shed 14.5% to RM424.5 million due to lower billings as some of the projects had reached or were near their completion stage.

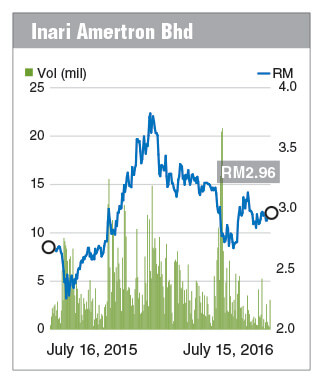

Inari Amertron Bhd

YEAR to date, Inari Amertron Bhd’s share price had slipped 18% to close at RM2.96 last Friday, with a market capitalisation of RM2.83 billion. The stock has been trading in a 52-week range of RM2.24 to RM3.96.

In a note to clients on May 18, CIMB Equity Research analyst Mohd Shanaz Noor Azam blamed the stock’s decline on weak sentiment across the sector following the decline in Apple’s iPhone production and the strengthening of the ringgit against the US dollar.

He believed Inari’s fundamentals remain intact given that its key customer, Broadcom, expects radio frequency content in smartphones to grow by more than 20% per year over the next three years. “Moreover, Inari is also diversifying its earnings stream with its latest venture into China, following an investment in PCL Technologies.”

The research firm, which still counts Inari as its top pick in the semiconductor sector, is maintaining its “add” call on Inari, but with a lower target price of RM3.15 from RM3.65 previously.

“We expect Inari to show stronger earnings growth in the fourth financial quarter ended June 30, 2016, driven by recovery in industry demand on the back of new smartphone launches in 2H16. Therefore, we believe Inari is still on track for another year of record profits in FY16,” said Mohd Shanaz.

TA Securities technology analyst Paul Yap told The Edge Financial Daily that a major smartphone launch in 2H16, Inari’s ramp-up of capacity to 680 testers by September and a weak ringgit, which the research firm forecasts to slip to RM4.20 by year end, are expected to boost Inari’s performance in 2H16.

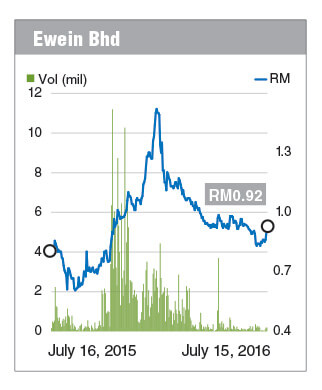

Ewein Bhd

YEAR-on-year, Ewein Bhd has kept its earnings growth momentum going this year. Mercury Securities research head Edmund Tham said the Penang-based property developer has been posting consistent earnings over the past few quarters. Indeed, Ewein’s growth numbers have been impressive, mainly driven by its property development business.

“Purely based on recent results, its fundamentals are intact. It (earnings growth) looks sustainable,” he told The Edge Financial Daily.

For the first quarter ended March 31, 2016, Ewein posted a 514% increase in net profit to RM4.17 million on the back of a 108.23% jump in revenue to RM20.24 million, mainly due to recognition of profits from its City of Dreams project in Penang. Ewein is jointly developing the RM800 million condominium project in Bandar Tanjong Pinang with Consortium Zenith BUCG Sdn Bhd.

However, Ewein’s share price movement does not reflect the earnings growth. Year to date, the stock had tumbled 28% from RM1.28 on Dec 31, 2015 to close at 92 sen last Friday, valuing it at RM204.12 million.

Sasbadi Holdings Bhd

DESPITE being in a business often seen as recession-proof, educational publisher Sasbadi Holdings Bhd saw its quarterly net profit fall for the first time since its listing on the Main Market of Bursa Malaysia in July 2014, in the second financial quarter ended Feb 29, 2016 (2QFY16).

Its net profit dropped 20% to RM6.64 million compared with RM8.34 million in 2QFY15, even though revenue rose 5% to RM33.86 million from RM32.11 million. It blamed the decrease in net profit on higher resources used for the textbook tender participation.

In spite of the slightly tepid results, Hong Leong Investment Bank Research continues to like Sasbadi due to its strong annual free cash flow, high growth rate, its innovativeness in creating products that cater to technology-savvy youth and unique education exposure, which is closely linked to the country’s education system.

In a report on June 20, its analyst Mardhiah Omar reiterated a “buy” call on Sasbadi, with a target price of RM1.55, implying a potential 21% upside to its closing price of RM1.22 last Friday.

However, Mardhiah said its earnings forecast for FY16 has been slightly reduced by 4% as the research firm believes that the group would be slightly affected by the weak purchasing power and tough business environment. “Hence, we are expecting a softer 2H16 for the group.”

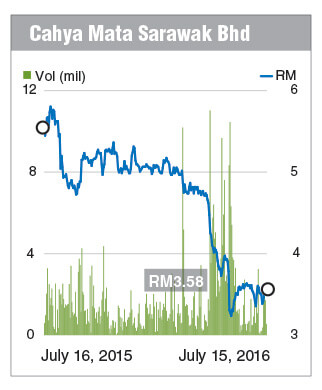

Cahya Mata Sarawak Bhd

CAHYA Mata Sarawak Bhd (CMS), touted as one of the best proxies for the mega projects in Sarawak, reported disappointing net profit in the first quarter ended March 31, 2016 (1QFY16). Its earnings plunged 98% to RM1.05 million from RM57.42 million in 1QFY15, as revenue fell by 29% year-on-year and due to lower profit margin as well as share of substantial losses in associates.

RHB Research, which had a “buy” call on CMS, has downgraded the stock to “neutral” as it cuts its earnings forecast for FY16 and FY17 by 14.8% and 7.6% respectively and lowers its target price (TP) to RM4.80 from RM5.86 initially. The TP still offers a 34% potential upside from last Friday’s closing price of RM3.58. Year to date, however, CMS has lost almost 30% of its value from RM5.09 on Dec 31, 2015.

In a report dated April 14, the research firm said CMS’ subscription to RM110 million convertible preference shares in OM Materials (Sarawak) Sdn Bhd suggested that the latter’s business environment may be more challenging than RHB Research had initially projected.

It continues to like CMS as the best proxy to the rapid development activities in Sarawak. “We believe its medium- to longer-term outlook remains bright and CMS could make a comeback as soon as 2H16,” RHB Research added.

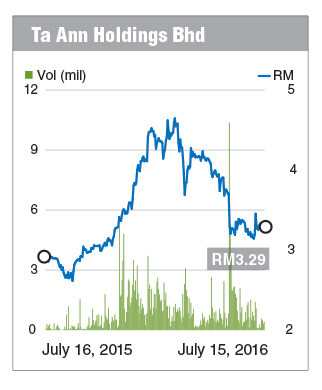

Ta Ann Holdings Bhd

TA ANN Holdings Bhd, with its attractive dividend yield, high-growth businesses and undemanding valuation, is a top pick in 2016 for analysts. However, its first-quarter earnings were less than impressive, coming in below expectations of Kenanga Research plantation analyst Voon Yee Ping and consensus, meeting only 11% and 9% of their core net profit estimates respectively.

For the three months ended March 31, 2016 (1QFY16), Ta Ann posted a 53.7% decline in net profit to RM12.55 million on the back of a 1.6% decline in revenue to RM218.53 million.

In a note to clients on May 20, Voon said the company posted weak results in 1QFY16 due a 16% year-on-year (y-o-y) and an 8% y-o-y decline to US$221 (RM871) per cu m and US$469 per cu m in log and plywood prices respectively, compounded by weaker production volume (logs and plywood declined 33% and 14% respectively).

When contacted, Voon said Ta Ann’s share price was also impacted by the stronger ringgit at the start of the year and its weaker production volumes. Year to date, the share price had declined by 20% to close at RM3.29 last Friday, with a market capitalisation of RM1.46 billion.

However, Voon is optimistic about Ta Ann moving forward as the ringgit has weakened since then and timber prices are expected to pick up. The ringgit closed at 3.9457 to the US dollar last Friday.

“The first quarter was the worst for the year [in terms of timber prices], but with the weakening ringgit and timber prices improving things would be better going forward,” she said.

For the long term, she said Ta Ann’s palm oil segment will boost its earnings as its young oil palms are coming into years of higher production. “The trees are six to seven years old on average. So over the next few years, Ta Ann’s plantation segment will be a better driver of its earnings.”

Karex Bhd

KAREX Bhd, the world’s largest condom manufacturer by volume which was seen as a strong beneficiary of the weak ringgit against the US dollar, saw its fortunes turn when the local currency strengthened this year as it reported a huge net foreign exchange loss of RM5 million for the third financial quarter ended March 31, 2016 (3QFY16). This dragged its net profit down by 37% to RM9.63 million from RM15.21 million a year ago.

While Affin Hwang Capital remains upbeat about Karex’s strategic expansion into the high-margin own brand manufacturing (OBM) segment, it said the longer gestation period could keep costs elevated for the time being, keeping margins expansion in check. As such, in its May 30 note on Karex, Affin Hwang Capital revised its estimates on Karex downwards by 14% to 18% for financial year ended June 30, 2016 (FY16) to FY18 after taking into account the slower-than-expected ramp-up in the OBM segment, among others.

Still, the research firm expects 4QFY16 core net profit to normalise to the region of RM15 million to RM20 million on weaker ringgit, while latex prices have eased back to around RM4.50 from RM5.

“Successful expansion into the OBM segment would be a key rerating catalyst. However, valuations look rich for now,” it said, maintaining its “hold” call on Karex with a RM2.32 target price.

Year to date, Karex’s share price has fallen 16% from RM2.75 on Dec 31, 2015 to RM2.30 last Friday, with a market capitalisation of RM2.31 billion.

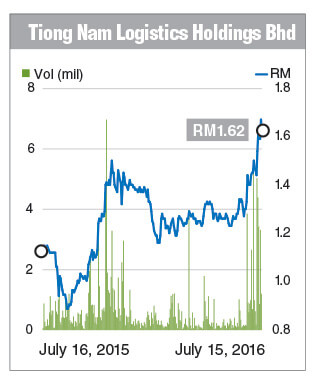

Tiong Nam Logistics Holdings Bhd

TIONG Nam Logistics Holdings Bhd extended its positive earnings streak into the first three months of the year, with its net profit up 3% to RM36.55 million from RM35.55 million a year ago. The better quarterly profit helped push up full-year earnings by 9% to RM79.62 million for the financial year ended March 31, 2016 (FY16) from RM72.88 million in FY15.

For FY17, TA Securities analyst Tan Kam Meng expects the group’s net profit to grow faster and see double-digit rate of growth. He is projecting a 14% increase in net profit to RM90.9 million in FY17 on increased warehouse storage capacity, jump in property revenue from its PineTree Residence project and new property sales of RM129.7 million.

In a report dated June 7, Tan was of the view that Tiong Nam, being the largest land transportation and warehouse owner in Malaysia, was trading at an inexpensive price-earnings ratio of 4.9 times to calendar year 2017 earnings per share forecast.

“This is unjustifiable given its strong earnings growth prospect. In addition, the establishment of a real estate investment trust in the near run could free up the group’s resources and enhance its balance sheet quality,” he said, initiating coverage on Tiong Nam with a “buy” recommendation and a RM1.82 target price, which implies a 12% potential upside to its closing price of RM1.62 last Friday. Year to date, the counter has risen 18%.

Tan also believes that the current soft market condition has little impact on Tiong Nam’s property segment, which has been focusing on niche development. The property segment contributed 23% to the group’s total revenue in FY16.

It noted that Tiong Nam will also be immune to higher land cost as it already owns 25 warehouses and has 253 acres (102ha) of undeveloped land bank.

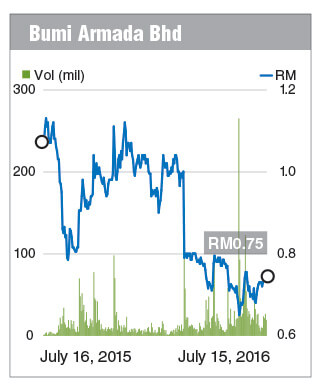

Bumi Armada Bhd

A VICTIM of the slowdown in the oil and gas sector, Bumi Armada Bhd saw its net profit fall 67% to RM23.43 million in the first quarter ended March 31, 2016 (1QFY16) from RM72.05 million a year ago, along with its revenue which dropped by 25% year-on-year to RM430.77 million.

In a report dated June 1, Maybank Investment Bank Bhd (Maybank IB) said the 1QFY16 results came in below the research house’s and consensus initial financial year forecasts, prompting it to cut its FY16 to FY18 earnings for Bumi Armada by 3% to 30%.

It expects Bumi Armada’s earnings to remain weak in 2QFY16 and 3QFY16, owing to the absence of earnings from one of the company’s floating production storage and offloading (FPSO) units called Armada Claire (which saw its contract terminated in March) and lower conversion works.

However, Maybank IB sees a recovery from 4QFY16 onwards as Bumi Armada recognises profits from its four other vessels — FPSO Angola, FSU Malta, FPSO Kraken and FPSO Madura.

The research firm is keeping its “buy” call on Bumi Armada, with an unchanged target price of RM1.05, adding that any share price weakness following the 1QFY16 results is an opportunity to accumulate.

Year to date, Bumi Armada’s share price has lost 26% to close at 75 sen last Friday, with a market capitalisation of RM4.4 billion.

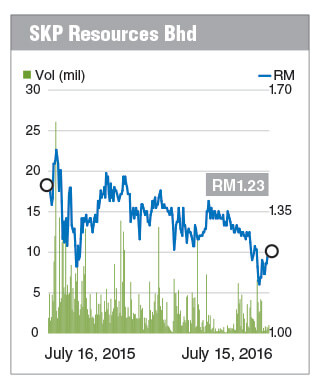

SKP Resources Bhd

SKP Resources Bhd continued its earnings growth momentum in 1H16, posting an 88% jump in net profit to RM21.68 million for the fourth quarter ended March 31, 2016 (4QFY16). Revenue also rose 18% to RM231.97 million during the quarter.

For the full FY16, it saw net profit jump 94% to RM82.15 million, coming in within Kenanga Research’s expectations.

In a note dated May 31, Kenanga Research analyst Desmond Chong said the plastic moulding company’s long-term earnings prospects remained resilient anchored by two long-term contracts awarded by UK-based appliance manufacturer Dyson Ltd, with targeted sales contribution of RM1 billion per year on cordless vacuum cleaners.

He is maintaining his “outperform” call on the stock, with a marginally lower target price of RM1.72 from RM1.76 previously.

However, the Brexit vote last month sparked concern about the prospect of SKP Resources on the sale of Dyson products. The US is its biggest market, followed by Japan in terms of sales and profits.

Still, an analyst who declined to be named said it is too early to gauge the impact of Brexit on SKP Resources, adding that sales weakness from the European Union would be made up by the growing demand for cordless vacuum cleaners in Asia.

Compared with its closing price of RM1.31 on Dec 31, 2015, SKP Resources’ share price has fallen by 6% to close at RM1.23 last Friday, giving it a market capitalisation of RM1.44 billion.

http://www.theedgemarkets.com/my/article/hits-and-mostly-misses-1h16

STOCKS in Malaysia had a roller-coaster ride over the first half of the year (1H16) as the market reacted to concerns about ringgit depreciation, oil price declines, possible interest rate hike by the US Federal Reserve, the health of the Chinese economy and risks of a global recession. Malaysian companies’ 1H16 profits also disappointed, leading to further earnings cuts. The benchmark FBM KLCI lost about 6% of its value to 1,600.92 in 21 days in January as investors were unnerved by steep falls in Chinese equity markets. The index has somewhat recovered since then, moving to 1,727.99 points on April 15 and closed at 1,668.40 last Friday. As the market enters 2H16, Meena Lakshana and Yimie Yong took a look at how the 10 stock picks The Edge Financial Daily featured on Jan 4 fared in 1H16 and whether the analysts’ views remain unchanged.

Sunway Construction Group Bhd

SUNWAY Construction Group Bhd (SunCon), which was seen as the best proxy to the construction sector this year underpinned by a strong infrastructure pipeline, had seen its share price climb 21% this year to close at RM1.65 last Friday, with a market capitalisation of RM2.13 billion. Its strong outstanding order book of RM5 billion, which translates into 2.6 times of its revenue in the financial year ended Dec 31, 2015, and expectations of more public infrastructure projects to be rolled out are keeping SunCon on TA Securities’ list of stock picks, with a target price of RM1.80.

In a recent report, TA Securities expects SunCon to win as much as RM2.5 billion worth of jobs this year. This is supported by internal construction jobs of RM500 million to RM800 million a year (from Sunway Group) as bedrock orders.

The research firm also pointed to SunCon’s cash-rich balance sheet. The group has a net cash position of 23 sen per share.

With the current net cash position and limited capital expenditure requirement, there is a potential upside to its dividend payout going forward, said TA Securities. “Based on its minimum dividend payout of 35%, we expect SunCon to offer reasonable dividend yield of about 3%.”

However, SunCon’s earnings did not fare well in the first quarter ended March 31, 2016, falling 15.5% to RM29.06 million. Its revenue shed 14.5% to RM424.5 million due to lower billings as some of the projects had reached or were near their completion stage.

Inari Amertron Bhd

YEAR to date, Inari Amertron Bhd’s share price had slipped 18% to close at RM2.96 last Friday, with a market capitalisation of RM2.83 billion. The stock has been trading in a 52-week range of RM2.24 to RM3.96.

In a note to clients on May 18, CIMB Equity Research analyst Mohd Shanaz Noor Azam blamed the stock’s decline on weak sentiment across the sector following the decline in Apple’s iPhone production and the strengthening of the ringgit against the US dollar.

He believed Inari’s fundamentals remain intact given that its key customer, Broadcom, expects radio frequency content in smartphones to grow by more than 20% per year over the next three years. “Moreover, Inari is also diversifying its earnings stream with its latest venture into China, following an investment in PCL Technologies.”

The research firm, which still counts Inari as its top pick in the semiconductor sector, is maintaining its “add” call on Inari, but with a lower target price of RM3.15 from RM3.65 previously.

“We expect Inari to show stronger earnings growth in the fourth financial quarter ended June 30, 2016, driven by recovery in industry demand on the back of new smartphone launches in 2H16. Therefore, we believe Inari is still on track for another year of record profits in FY16,” said Mohd Shanaz.

TA Securities technology analyst Paul Yap told The Edge Financial Daily that a major smartphone launch in 2H16, Inari’s ramp-up of capacity to 680 testers by September and a weak ringgit, which the research firm forecasts to slip to RM4.20 by year end, are expected to boost Inari’s performance in 2H16.

Ewein Bhd

YEAR-on-year, Ewein Bhd has kept its earnings growth momentum going this year. Mercury Securities research head Edmund Tham said the Penang-based property developer has been posting consistent earnings over the past few quarters. Indeed, Ewein’s growth numbers have been impressive, mainly driven by its property development business.

“Purely based on recent results, its fundamentals are intact. It (earnings growth) looks sustainable,” he told The Edge Financial Daily.

For the first quarter ended March 31, 2016, Ewein posted a 514% increase in net profit to RM4.17 million on the back of a 108.23% jump in revenue to RM20.24 million, mainly due to recognition of profits from its City of Dreams project in Penang. Ewein is jointly developing the RM800 million condominium project in Bandar Tanjong Pinang with Consortium Zenith BUCG Sdn Bhd.

However, Ewein’s share price movement does not reflect the earnings growth. Year to date, the stock had tumbled 28% from RM1.28 on Dec 31, 2015 to close at 92 sen last Friday, valuing it at RM204.12 million.

Sasbadi Holdings Bhd

DESPITE being in a business often seen as recession-proof, educational publisher Sasbadi Holdings Bhd saw its quarterly net profit fall for the first time since its listing on the Main Market of Bursa Malaysia in July 2014, in the second financial quarter ended Feb 29, 2016 (2QFY16).

Its net profit dropped 20% to RM6.64 million compared with RM8.34 million in 2QFY15, even though revenue rose 5% to RM33.86 million from RM32.11 million. It blamed the decrease in net profit on higher resources used for the textbook tender participation.

In spite of the slightly tepid results, Hong Leong Investment Bank Research continues to like Sasbadi due to its strong annual free cash flow, high growth rate, its innovativeness in creating products that cater to technology-savvy youth and unique education exposure, which is closely linked to the country’s education system.

In a report on June 20, its analyst Mardhiah Omar reiterated a “buy” call on Sasbadi, with a target price of RM1.55, implying a potential 21% upside to its closing price of RM1.22 last Friday.

However, Mardhiah said its earnings forecast for FY16 has been slightly reduced by 4% as the research firm believes that the group would be slightly affected by the weak purchasing power and tough business environment. “Hence, we are expecting a softer 2H16 for the group.”

Cahya Mata Sarawak Bhd

CAHYA Mata Sarawak Bhd (CMS), touted as one of the best proxies for the mega projects in Sarawak, reported disappointing net profit in the first quarter ended March 31, 2016 (1QFY16). Its earnings plunged 98% to RM1.05 million from RM57.42 million in 1QFY15, as revenue fell by 29% year-on-year and due to lower profit margin as well as share of substantial losses in associates.

RHB Research, which had a “buy” call on CMS, has downgraded the stock to “neutral” as it cuts its earnings forecast for FY16 and FY17 by 14.8% and 7.6% respectively and lowers its target price (TP) to RM4.80 from RM5.86 initially. The TP still offers a 34% potential upside from last Friday’s closing price of RM3.58. Year to date, however, CMS has lost almost 30% of its value from RM5.09 on Dec 31, 2015.

In a report dated April 14, the research firm said CMS’ subscription to RM110 million convertible preference shares in OM Materials (Sarawak) Sdn Bhd suggested that the latter’s business environment may be more challenging than RHB Research had initially projected.

It continues to like CMS as the best proxy to the rapid development activities in Sarawak. “We believe its medium- to longer-term outlook remains bright and CMS could make a comeback as soon as 2H16,” RHB Research added.

Ta Ann Holdings Bhd

TA ANN Holdings Bhd, with its attractive dividend yield, high-growth businesses and undemanding valuation, is a top pick in 2016 for analysts. However, its first-quarter earnings were less than impressive, coming in below expectations of Kenanga Research plantation analyst Voon Yee Ping and consensus, meeting only 11% and 9% of their core net profit estimates respectively.

For the three months ended March 31, 2016 (1QFY16), Ta Ann posted a 53.7% decline in net profit to RM12.55 million on the back of a 1.6% decline in revenue to RM218.53 million.

In a note to clients on May 20, Voon said the company posted weak results in 1QFY16 due a 16% year-on-year (y-o-y) and an 8% y-o-y decline to US$221 (RM871) per cu m and US$469 per cu m in log and plywood prices respectively, compounded by weaker production volume (logs and plywood declined 33% and 14% respectively).

When contacted, Voon said Ta Ann’s share price was also impacted by the stronger ringgit at the start of the year and its weaker production volumes. Year to date, the share price had declined by 20% to close at RM3.29 last Friday, with a market capitalisation of RM1.46 billion.

However, Voon is optimistic about Ta Ann moving forward as the ringgit has weakened since then and timber prices are expected to pick up. The ringgit closed at 3.9457 to the US dollar last Friday.

“The first quarter was the worst for the year [in terms of timber prices], but with the weakening ringgit and timber prices improving things would be better going forward,” she said.

For the long term, she said Ta Ann’s palm oil segment will boost its earnings as its young oil palms are coming into years of higher production. “The trees are six to seven years old on average. So over the next few years, Ta Ann’s plantation segment will be a better driver of its earnings.”

Karex Bhd

KAREX Bhd, the world’s largest condom manufacturer by volume which was seen as a strong beneficiary of the weak ringgit against the US dollar, saw its fortunes turn when the local currency strengthened this year as it reported a huge net foreign exchange loss of RM5 million for the third financial quarter ended March 31, 2016 (3QFY16). This dragged its net profit down by 37% to RM9.63 million from RM15.21 million a year ago.

While Affin Hwang Capital remains upbeat about Karex’s strategic expansion into the high-margin own brand manufacturing (OBM) segment, it said the longer gestation period could keep costs elevated for the time being, keeping margins expansion in check. As such, in its May 30 note on Karex, Affin Hwang Capital revised its estimates on Karex downwards by 14% to 18% for financial year ended June 30, 2016 (FY16) to FY18 after taking into account the slower-than-expected ramp-up in the OBM segment, among others.

Still, the research firm expects 4QFY16 core net profit to normalise to the region of RM15 million to RM20 million on weaker ringgit, while latex prices have eased back to around RM4.50 from RM5.

“Successful expansion into the OBM segment would be a key rerating catalyst. However, valuations look rich for now,” it said, maintaining its “hold” call on Karex with a RM2.32 target price.

Year to date, Karex’s share price has fallen 16% from RM2.75 on Dec 31, 2015 to RM2.30 last Friday, with a market capitalisation of RM2.31 billion.

Tiong Nam Logistics Holdings Bhd

TIONG Nam Logistics Holdings Bhd extended its positive earnings streak into the first three months of the year, with its net profit up 3% to RM36.55 million from RM35.55 million a year ago. The better quarterly profit helped push up full-year earnings by 9% to RM79.62 million for the financial year ended March 31, 2016 (FY16) from RM72.88 million in FY15.

For FY17, TA Securities analyst Tan Kam Meng expects the group’s net profit to grow faster and see double-digit rate of growth. He is projecting a 14% increase in net profit to RM90.9 million in FY17 on increased warehouse storage capacity, jump in property revenue from its PineTree Residence project and new property sales of RM129.7 million.

In a report dated June 7, Tan was of the view that Tiong Nam, being the largest land transportation and warehouse owner in Malaysia, was trading at an inexpensive price-earnings ratio of 4.9 times to calendar year 2017 earnings per share forecast.

“This is unjustifiable given its strong earnings growth prospect. In addition, the establishment of a real estate investment trust in the near run could free up the group’s resources and enhance its balance sheet quality,” he said, initiating coverage on Tiong Nam with a “buy” recommendation and a RM1.82 target price, which implies a 12% potential upside to its closing price of RM1.62 last Friday. Year to date, the counter has risen 18%.

Tan also believes that the current soft market condition has little impact on Tiong Nam’s property segment, which has been focusing on niche development. The property segment contributed 23% to the group’s total revenue in FY16.

It noted that Tiong Nam will also be immune to higher land cost as it already owns 25 warehouses and has 253 acres (102ha) of undeveloped land bank.

Bumi Armada Bhd

A VICTIM of the slowdown in the oil and gas sector, Bumi Armada Bhd saw its net profit fall 67% to RM23.43 million in the first quarter ended March 31, 2016 (1QFY16) from RM72.05 million a year ago, along with its revenue which dropped by 25% year-on-year to RM430.77 million.

In a report dated June 1, Maybank Investment Bank Bhd (Maybank IB) said the 1QFY16 results came in below the research house’s and consensus initial financial year forecasts, prompting it to cut its FY16 to FY18 earnings for Bumi Armada by 3% to 30%.

It expects Bumi Armada’s earnings to remain weak in 2QFY16 and 3QFY16, owing to the absence of earnings from one of the company’s floating production storage and offloading (FPSO) units called Armada Claire (which saw its contract terminated in March) and lower conversion works.

However, Maybank IB sees a recovery from 4QFY16 onwards as Bumi Armada recognises profits from its four other vessels — FPSO Angola, FSU Malta, FPSO Kraken and FPSO Madura.

The research firm is keeping its “buy” call on Bumi Armada, with an unchanged target price of RM1.05, adding that any share price weakness following the 1QFY16 results is an opportunity to accumulate.

Year to date, Bumi Armada’s share price has lost 26% to close at 75 sen last Friday, with a market capitalisation of RM4.4 billion.

SKP Resources Bhd

SKP Resources Bhd continued its earnings growth momentum in 1H16, posting an 88% jump in net profit to RM21.68 million for the fourth quarter ended March 31, 2016 (4QFY16). Revenue also rose 18% to RM231.97 million during the quarter.

For the full FY16, it saw net profit jump 94% to RM82.15 million, coming in within Kenanga Research’s expectations.

In a note dated May 31, Kenanga Research analyst Desmond Chong said the plastic moulding company’s long-term earnings prospects remained resilient anchored by two long-term contracts awarded by UK-based appliance manufacturer Dyson Ltd, with targeted sales contribution of RM1 billion per year on cordless vacuum cleaners.

He is maintaining his “outperform” call on the stock, with a marginally lower target price of RM1.72 from RM1.76 previously.

However, the Brexit vote last month sparked concern about the prospect of SKP Resources on the sale of Dyson products. The US is its biggest market, followed by Japan in terms of sales and profits.

Still, an analyst who declined to be named said it is too early to gauge the impact of Brexit on SKP Resources, adding that sales weakness from the European Union would be made up by the growing demand for cordless vacuum cleaners in Asia.

Compared with its closing price of RM1.31 on Dec 31, 2015, SKP Resources’ share price has fallen by 6% to close at RM1.23 last Friday, giving it a market capitalisation of RM1.44 billion.

http://www.theedgemarkets.com/my/article/hits-and-mostly-misses-1h16