1. The Teapots

Shandong Hengyuan is an enterprise backed by Shandong's local government (some said it is privately owned. Whatever it is, I don't think the nature of ownership is important).

It is a Teapot Refinery, a term used to describe refinery with capacity as small as 20,000 to 100,000 barrels per day (bpd). Shandong Hengyuan's capacity is 70,000 bpd while the capacity of its newly acquired 51% owned subsidiary Hengyuan Refining at Port Dickson (previously Shell Refining) is 156,000 bpd, twice its size.

There are about 20 Teapots in China, 80% of which are in Shandong province. Their presence is quite significant. Collectively, they accounted for 15% of China's crude import and 20% of its refining capacity.

Teapots are more efficient and profitable than state owned big boys such as CNPC, Petrochina and Sinopec. One of the reasons is because the SOEs incurred high assets acquisition cost during the oil boom years.

The SOEs are hostile towards the Teapots and constantly lobby against them. As a result, the Central Government imposed all kind of conditions on the Teapots. Teapots were not allowed to import crude directly from overseas and have to buy from SOEs, thereby allowing SOEs to make a cut (this restriction was uplifted in 2016). The Central Government also imposed export quotas on Teapots. In short, life for Teapots is not easy.

If that is the case, why did the government allow the Teapots to mushroom in the first place ? That was actually caused by the unique dynamics between Local and Central Government.

Teapots came into existence because of the policy pursued by the existing provincial governor Guo Shuqing. It was a way to generate economic growth, create employment and increase tax revenue. All these are good things, so the Central Government has no issue with it. However, when the Teapots became too successful and threatened the SOEs, the Central Government stepped in to intervene. That is how they ended up with the current mess. Welcome to China !!!

As a result of the unfriendly policies, Teapots started looking for ways to diversify. Some moved up the value chain to produce chemicals, one ventured into lumber business, one ventured into Lithium battery business, etc. And of course, diversification overseas is always an option, provided the opportunity is there.

And that opportunity came knocking on the door one day.

2. The Deal

In February 2016, Shell International announced that it was disposing 51% equity stake in Shell Refining to Shandong Hengyuan. Shell has been in Malaysia for a long time (at least since the 1960s). It has three major divisions : upstream, refinery as well as petrol stations. It is not difficult to guess why Shell wanted to exit the refining business. Oil price has collapsed since 2014. The disposal was likely part of its streamlining exercise to strengthen its financial position.

What was intriguing about the deal was the pricing. Shell disposed of its 51% stake in Shell Refining to Hengyuan at RM1.92 per share. This represented a huge 60% discount to Shell Refining's market price before announcement of the deal. The official reason given by Shell International was that Shandong Hengyuan has demonstrated ability to refinance Shell Refining's borrowings. This is actually a very credible explanation : banks lent money to Shell Refining in the past because they trusted the Shell name. But now a Teapot has emerged as the new controlling shareholder, the risk profile has changed beyond recognition. The banks wanted their money back. Whoever that can pull off a refinancing deal will be the most qualified candidate.

Still, one can't stop wondering whether Shell International has tried hard enough to find a better buyer. Shell Refining is a very valuable asset, it is really a big waste to sell at such a depressed price. Afterall, it is not like Shell is facing bankruptcy during that time. Why in a hurry ? Until today, many investors, analysts and fund managers are still scratching their head.

Maybe they can stop scratching their head now. I think I might be able to provide an explanation.

3. The Partnership

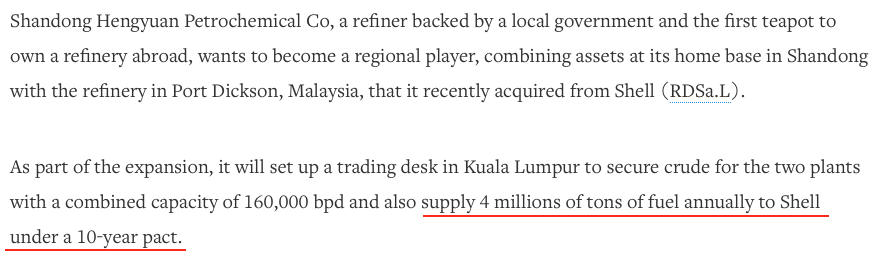

It seemed that Shell International's disposal of 51% stake is not the end of the story. Pursuant to the transaction, Shandong Hengyuan has entered into a 10 year agreement with Shell to supply it with 4 million tonnes of fuel annually.

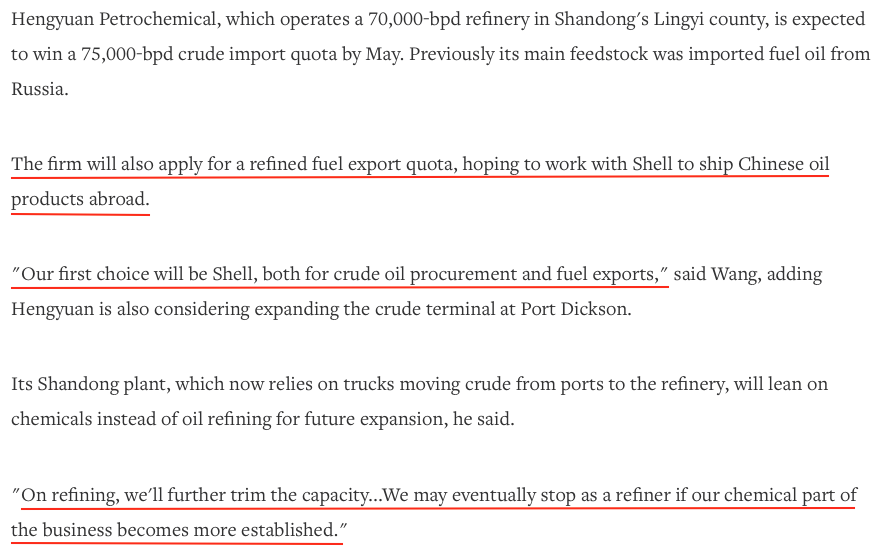

This explains a lot of things. First of all, it explains why Shell International was willing to part with its 51% stake at such depressed price. The Shell Group can claw back some of its lost value (probably through attractive pricing of products) through the subsequent long term supply agreement.

Secondly, it explained why an ex Shell empoyee was appointed as the Managing Director of Hengyuan Refining. The objective is not to protect Shell's interest (there is nothing to protect anyway. Shell International does not own any more stake in Hengyuan Refining). I believe it is more to make sure that Hengyuan Refining can continue to meet the high standard required by Shell International for its products.

It seemed that Shandong Hengyuan's relationship with Shell is not limited to Malaysia. The Chairman elaborated on how they intend to work with Shell on various other business oppurtunities.

4. Concluding Remarks

I have fed you with a lot of information. But this is not a business school, we are here to discuss how to make money from punting Hengyuan. So, what are the conclusions ?

The conclusions are as follows :-

(a) Once again, I would like to argue that the Hengyuan Group is not the same as the other dodgy Red Chips that faked accounts and information. It has an established track record in the industry. The details that I got from various new sources allow us to have a good feel of what it does, what problems it faced, what drove its recent acquisition of Shell Refiing and what its aspiration is.

(b) The long term partnership with Shell Group is a very positive point. Even though Shell has exited the refining industry in Malaysia, it is keeping its petrol stations operation.

The petrol stations are sourcing the refined products from Hengyuan Refining. Hengyuan will need to operate professionally to ensure no disruption of supply.

The government is actually a party to this arrangement (albeit invisible). Any disruption of supply to Shell petrol stations will create turmoil and adversely affect the economy. In other words, many pairs of eyes are watching the Hengyuan Group. Do you really think they will do stupid things like cooking their books ?

For more detals, please refer to the following articles :-

http://www.hellenicshippingnews.com/chinese-teapots-the-game-changer-in-chinas-oil-industry/

http://www.chinadaily.com.cn/business/2016-12/28/content_27795122.htm

https://www.ft.com/content/7fc95106-fc71-11e5-b5f5-070dca6d0a0d

http://klse.i3investor.com/blogs/icon8888/127720.jsp

Shandong Hengyuan is an enterprise backed by Shandong's local government (some said it is privately owned. Whatever it is, I don't think the nature of ownership is important).

It is a Teapot Refinery, a term used to describe refinery with capacity as small as 20,000 to 100,000 barrels per day (bpd). Shandong Hengyuan's capacity is 70,000 bpd while the capacity of its newly acquired 51% owned subsidiary Hengyuan Refining at Port Dickson (previously Shell Refining) is 156,000 bpd, twice its size.

There are about 20 Teapots in China, 80% of which are in Shandong province. Their presence is quite significant. Collectively, they accounted for 15% of China's crude import and 20% of its refining capacity.

Teapots are more efficient and profitable than state owned big boys such as CNPC, Petrochina and Sinopec. One of the reasons is because the SOEs incurred high assets acquisition cost during the oil boom years.

The SOEs are hostile towards the Teapots and constantly lobby against them. As a result, the Central Government imposed all kind of conditions on the Teapots. Teapots were not allowed to import crude directly from overseas and have to buy from SOEs, thereby allowing SOEs to make a cut (this restriction was uplifted in 2016). The Central Government also imposed export quotas on Teapots. In short, life for Teapots is not easy.

If that is the case, why did the government allow the Teapots to mushroom in the first place ? That was actually caused by the unique dynamics between Local and Central Government.

Teapots came into existence because of the policy pursued by the existing provincial governor Guo Shuqing. It was a way to generate economic growth, create employment and increase tax revenue. All these are good things, so the Central Government has no issue with it. However, when the Teapots became too successful and threatened the SOEs, the Central Government stepped in to intervene. That is how they ended up with the current mess. Welcome to China !!!

As a result of the unfriendly policies, Teapots started looking for ways to diversify. Some moved up the value chain to produce chemicals, one ventured into lumber business, one ventured into Lithium battery business, etc. And of course, diversification overseas is always an option, provided the opportunity is there.

And that opportunity came knocking on the door one day.

2. The Deal

In February 2016, Shell International announced that it was disposing 51% equity stake in Shell Refining to Shandong Hengyuan. Shell has been in Malaysia for a long time (at least since the 1960s). It has three major divisions : upstream, refinery as well as petrol stations. It is not difficult to guess why Shell wanted to exit the refining business. Oil price has collapsed since 2014. The disposal was likely part of its streamlining exercise to strengthen its financial position.

What was intriguing about the deal was the pricing. Shell disposed of its 51% stake in Shell Refining to Hengyuan at RM1.92 per share. This represented a huge 60% discount to Shell Refining's market price before announcement of the deal. The official reason given by Shell International was that Shandong Hengyuan has demonstrated ability to refinance Shell Refining's borrowings. This is actually a very credible explanation : banks lent money to Shell Refining in the past because they trusted the Shell name. But now a Teapot has emerged as the new controlling shareholder, the risk profile has changed beyond recognition. The banks wanted their money back. Whoever that can pull off a refinancing deal will be the most qualified candidate.

Still, one can't stop wondering whether Shell International has tried hard enough to find a better buyer. Shell Refining is a very valuable asset, it is really a big waste to sell at such a depressed price. Afterall, it is not like Shell is facing bankruptcy during that time. Why in a hurry ? Until today, many investors, analysts and fund managers are still scratching their head.

Maybe they can stop scratching their head now. I think I might be able to provide an explanation.

3. The Partnership

It seemed that Shell International's disposal of 51% stake is not the end of the story. Pursuant to the transaction, Shandong Hengyuan has entered into a 10 year agreement with Shell to supply it with 4 million tonnes of fuel annually.

This explains a lot of things. First of all, it explains why Shell International was willing to part with its 51% stake at such depressed price. The Shell Group can claw back some of its lost value (probably through attractive pricing of products) through the subsequent long term supply agreement.

Secondly, it explained why an ex Shell empoyee was appointed as the Managing Director of Hengyuan Refining. The objective is not to protect Shell's interest (there is nothing to protect anyway. Shell International does not own any more stake in Hengyuan Refining). I believe it is more to make sure that Hengyuan Refining can continue to meet the high standard required by Shell International for its products.

It seemed that Shandong Hengyuan's relationship with Shell is not limited to Malaysia. The Chairman elaborated on how they intend to work with Shell on various other business oppurtunities.

4. Concluding Remarks

I have fed you with a lot of information. But this is not a business school, we are here to discuss how to make money from punting Hengyuan. So, what are the conclusions ?

The conclusions are as follows :-

(a) Once again, I would like to argue that the Hengyuan Group is not the same as the other dodgy Red Chips that faked accounts and information. It has an established track record in the industry. The details that I got from various new sources allow us to have a good feel of what it does, what problems it faced, what drove its recent acquisition of Shell Refiing and what its aspiration is.

(b) The long term partnership with Shell Group is a very positive point. Even though Shell has exited the refining industry in Malaysia, it is keeping its petrol stations operation.

The petrol stations are sourcing the refined products from Hengyuan Refining. Hengyuan will need to operate professionally to ensure no disruption of supply.

The government is actually a party to this arrangement (albeit invisible). Any disruption of supply to Shell petrol stations will create turmoil and adversely affect the economy. In other words, many pairs of eyes are watching the Hengyuan Group. Do you really think they will do stupid things like cooking their books ?

For more detals, please refer to the following articles :-

http://www.hellenicshippingnews.com/chinese-teapots-the-game-changer-in-chinas-oil-industry/

http://www.chinadaily.com.cn/business/2016-12/28/content_27795122.htm

https://www.ft.com/content/7fc95106-fc71-11e5-b5f5-070dca6d0a0d

http://klse.i3investor.com/blogs/icon8888/127720.jsp