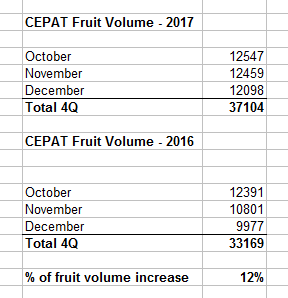

Earnings growth should return in 4Q. As we can see below, CEPAT fruit volume has increased 12% in 4Q. So the earnings should improve in 4Q against same period last year. While CPO price has been lower by about 10%, the higher fruit volume should boost earnings.

Current share price is 46% discount to the book value of RM1.53. The market has likely overlooked this as CEPAT share price is only 82 sen now, about 46% discount to the book value.

FY17 earnings will be a record high. 9MFY17 net profit of RM22.8m is already higher than FY16 net profit of RM21.1m. With 4Q profit at least should match same period last year, I foresee FY17 earnings to be a new record high for CEPAT. Ballpark figure about RM28m in total for FY17.

All in, Target Price RM1.20 (Upside 46%)

Value = 12x PE * 10 sen EPS for 2018 = RM1.20

For the details of CEPAT business, please read my previous post on the Company here… In short, it has 10,290 ha of plantation land in Sabah (8450 ha or 82% planted with oil palm). It also has 12 Megawatt Biomass power plant and a 3.8 Megawatt Biogas power plant, both in Sandakan, Sabah.

https://klse.i3investor.com/blogs/richDad/137200.jsp