PH Government Has Promised to Review All Highway Concessions

The recent announcement on the possible abolishment of toll has seen a stampede of investors out of Bursa stocks with toll road. A crisis is a flashing red warning for the danger ahead, yet there is an opportunity that lies in every crisis. In the time of turbulences, new kings are made but we must realize that many times more die in the attempt to be one. So no, this would not be a discourse of what is right or wrong but simply to lay out the known facts to the best ability of the author. Remember, the risks are yours, so should be your ultimate judgements for the sanctity of your financial well-being.

A 2010 study by PEMANDU estimated the costs to take over all highways in the country would be RM45.2b for taking over the highway concessionaires and RM338.1b for abolishing toll collection. More recently, a Maybank research report published that there is a total of RM55.3b of outstanding toll bonds in circulation based on the Bond Price Agency Malaysia (BPAM). Pakatan Harapan had earlier estimated that the takeover of all highways via the expropriation clause would only cost the government about RM50bil. What would be the right figure then?

Whatever the government decides, inevitably the compensation pay-out will be down to these 3 variables

- Outstanding debts – mostly bonds and perhaps some bank loan.

- Equities

- Future profits.

Unsurprisingly, the long descent of the toll road companies’ stock price accelerated since the end April/early May. There is no dispute that all concessionaires will be negatively impacted due to foregone future profit. Yet, two groups will be less impacted relatively

- New concessionaires as most of the concession assets are still financed with bond/bank loan, which will be paid by the government and little equities.

- Less efficient/profitable concessionaires as the equities portion are valued based on IRR minus out the accumulated profit in the year of operation.

EKOVEST: Duke/SPE

Ekovest is the operator of Duke Highway (Duke 1 & Duke 2) which was sold 40% to EPF at the RM2.8b at 100% valuation. Currently Ekovest is building RM3.6b Setiawangsa Pantai Expressway (SPE) since Aug 2016 with the expected completion date in 1Q2020 (Hint: It is too late to cancel). The location of the both highways are shown in the map below. Note the strategic location of both Duke Highway (Connecting KL Inner Ring Road with KL Middle Ring Road on the North and North East KL) and SPE Expressway (whichl traverse North and South of Kuala Lumpur and run along the eastern boundary of Bandar MalaysiaDirect link with Bandar Malaysia). Ekovest certainly meets the first criteria mentioned above as both Duke Highway and SPE Expressway concession only end in Aug 2059 and Aug 2069 respectively.

Source

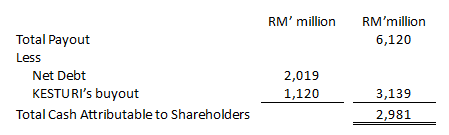

Assuming the government is paying only for all the outstanding bonds (zero value assigned for the equity portion), total payout for Ekovest is RM6.12b

Source: Maybank Research

Total cash attributable to the shareholders after deducting for total net debt for EKOVEST (this include all the debts for the construction, property and toll division) as of the most recent quarter (31/12/2017) and generously buying back EPF's 40% stake in KESTURI at the previous purchase price of RM1.12b.

Based on 2.139b share in circulation, total cash per share after the excercise is RM1.39. Please note that this is the minimum amount of cash per share and there could be upside to total cash per share with payment for the equities portion and less likely, future profit. After the disposal of the toll division, EKOVEST ends up with a minimum RM1.39 cash per share plus a construction division with RM5.6b in book order and a property division with up to 60 acres (30 acres in bag with another 30 potential acres from payment-in-kind for River of Life project) of prime land right the heart of KL with potential RM16.5b in GDV. All that for curent price of RM0.655 per share!

Zeti's announcement on the toll charges next week will provide greater clarity to the investors. There is a saying it is always darkest before dawn. Between now and the announcement, it is expected EKOVEST's share to gyrate violently. Despite the deep value as revealed here, readers should be aware of value trap and the danger of catching a falling knife. This is NOT a buy or sell call, but simply to lay out the facts. So are the cautions and the warnings.

OPPORTUNITIES or THREATS, your call!

Disclaimer:

A sharing of personal investment idea and thought and is not a recommendation to buy or sell.

http://klse.i3investor.com/blogs/20102017/157432.jsp