Altering the course of rivers and moving mountains is easy. Changing someone’s character is impossible.

Chinese saying.

Summary- A “bad” fourth quarter – oil sold is below expectation, but with good reason

- A very good fourth quarter – surprised (more) negative goodwill – more on this later

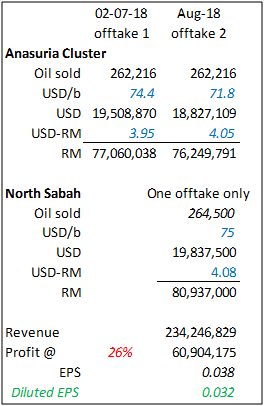

- North Sabah (NS) production – 5,903 bpd > 5,500 bpd assumed (+7%); 623,544 barrels oil sold at USD 73.26 and opex dropped from 12.92 to 8.15 (reduce by 37%)

- Anasuria Cluster production – 3,375 bpd > 2,800 bpd (+20%); zero barrel sold; opex reduced from 23.96 to 16.39 (-31.6%)

- Anasuria Cluster reserve upgraded to 24.4 mmb (P2) from 20.2 mmb

Investment / Speculation

Yes, if one narrowly looked at the fourth quarterly report, the “delayed” selling of oil produced in Anasuria Cluster was a shock to say the least. But there was a good reason for that and management has to be commended for it.

As an investor / shareholder of the company, I would want my asset to be safe and to keep producing oil (& gas) way into the future. So the decision to defer the off-take was a right one. Take a moment and imagine while oil is being transfer from the FPSO to the oil tanker and drilling rig encounter a blowout (this is the risk entering any well, especially an old well that was shut in, there may be gas buildup)

While gas will always be associated with any oil production and when there is a market for it, it is a bonus; from here on, only oil production figure will be considered and gas excluded, this also make the evaluation with an added margin of safety.

But one just cannot fault “investors” taking flight; evolution, yes evolution has caused this action once perceived danger is approaching. Malcolm Gladwell tells us in “BLINK” and many others. Millions of years, we are hardwired to run when danger approaches. It is in our genes. And it is hard to remain calm; I have learned this with many of my money “donated”. Investment made on a blink lost money while those with cold gaze and careful study make money.

Most investment bankers had gone through the quarterly report figures and it need not be repeated here.

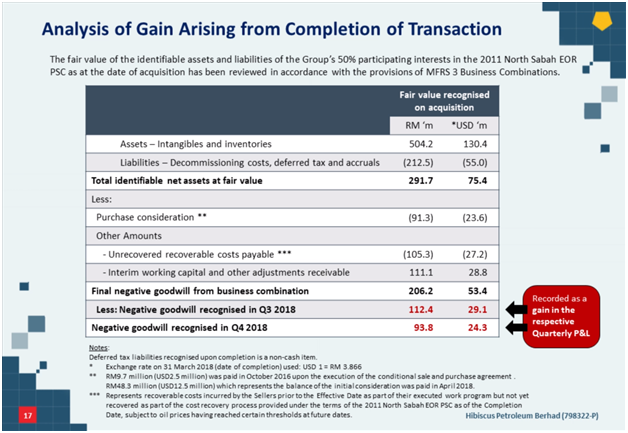

Negative Goodwill / Reserve upgrade

Accountants do have a way with words. They have to be different else “cannot find food”. Negative, yes, straight away ones think it is no good, negative, conjure up, invoke lost / lose / not good, poor and so on.

When I started my business, had headaches trying to understanding accounting terms, credit, debit, balance sheet among others.

But it was good training to understand the going on of a business and dare say become a better investor too. I highly recommend this to all prospective investor to go start a business, small one also can, then one will know first-hand what all the terms in the Annual report / quarterly report meant. Nothing beat hand-ons learning.

So in this particular sense, Negative Goodwill is a damn GOOD THING.

It meant the company bought the North Sabah asset CHEAP. This is not paying peanuts, get monkey.

Imagine you buy Mid-Valley mall for a quarter of the current market price, good, no?!?

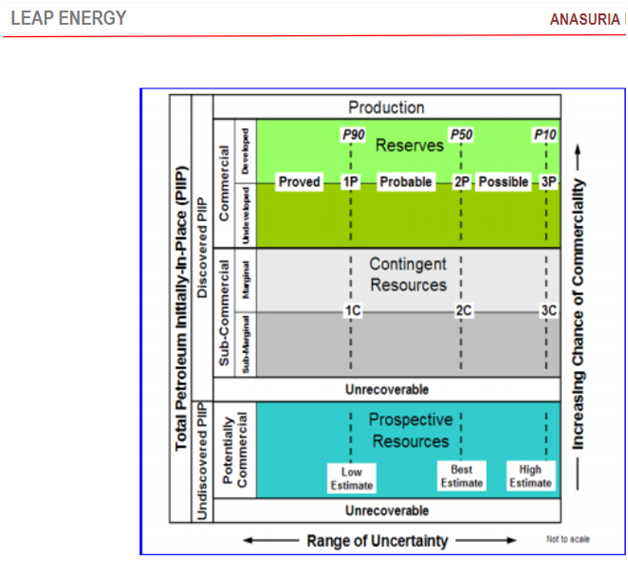

And reserve upgrade, well all this means is, just like Mid-Valley owner (IGB REIT), asset revaluation, the property / asset is more valuable now. Simply because it cost more to build another Mid-Valley, and producing oil reserve also more VALUABLE now as oil price is USD 70+, no longer at USD 30+ (much higher revenue).

HOW? Well like Mid-Valley, these lobbies, that open space, etc., can be turned into rental space for instance. Similarly, looking at flow rates from current producing wells may indicate slower depletion rate, newer better tools to evaluate seismic data could / would show up some pockets of reservoir not seen in previous evaluation and so on. This is a layman view of things, but an investor has to build this knowledge where value comes from, don’t just look at a word.

Of course, you are right, there is a big difference between a mall and a reservoir, one can see, the other is underground, for this one, also under the sea. That is why there is a range of possibility as shown in the graph: (P90 means at least a 90% probability that the estimated potentially recoverable quantity (from a technical standpoint) will equal or exceed the low estimate, on the assumption that development did proceed – from Guidelines for the Evaluation of Petroleum Reserves and Resources by Society of Petroleum Engineers)

An (independent) expert need to be employed to go through the data and an assessment made so that investor, shareholders have a feel what the asset is worth not based on what Management said.

It is just like going to see a doctor, get an x-ray / MRI / etc. and an “observation” made. Of course, a second opinion can be sought, are you willing to pay maybe RM 5 million for another reservoir assessment (I am guessing here)? Sometime, we just have to trust that DOCTOR.

LEAP (the independent expert) is conservative in their valuation too, oil price used is much less than the previous study.

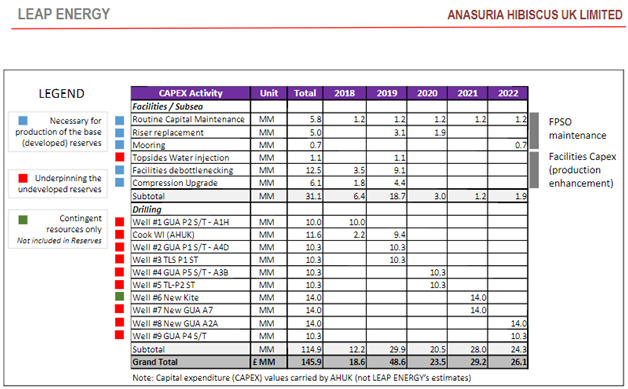

Management had been busy and had come up with a list of asset enhancement initiatives (AEI) as shown.

And with some of these AEI, the cash flow might be:

Sorry this is small; an enlarged one follows and please note the probable daily production and the oil price used.

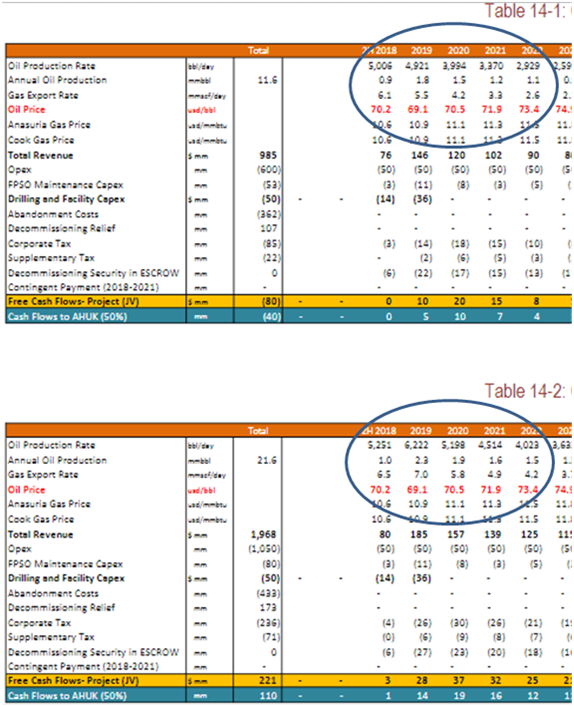

Table 14.1 is for 1P that is developed while Table 14.2 is for 2P developed. The expectation is daily oil production could exceed 5,000 barrels per day.

Do note the conservative oil prices used.

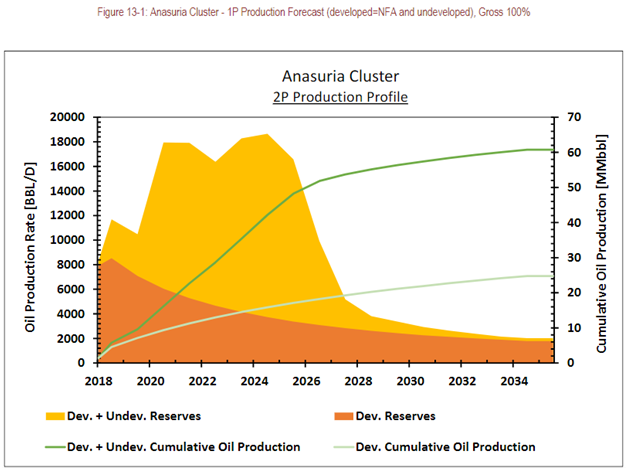

Management had guided Anasuria Cluster production would be 5,000 bpd by 2020.

And this is the production profile predicted.

What do all these mean to an investor / shareholder – negative goodwill and reserve upgraded?

The company net tangible assets’ value is higher, much higher, and oil should be continuously produced at current rate and for many more years to come.

(That is why Saudi Aramco will not be listed as no reserve evaluation for 40+ years, so you believe worth USD 2trillion or whatever they say?)

The main concern should be oil demand; would it be destroyed in the years to come so that the oil price will tanked back to USD 30 to 40 per barrel?

In the near term (next six months), No, medium term (up to 2 years), NO! Longer term (beyond 2 years), also NO. EV, please read my post here - https://klse.i3investor.com/blogs/teoct_blog/158175.jsp

The main risk would be a recession – can you guess when? Whatever your guess is, you are right because there is no right or wrong in this.

But if all this is still too much risk then get out, probably, death care is a better business. People definitely die! Demand always there. Oil, one can opt out – bicycle, walk.

So what will the future be like for my, company?

Stock markets / exchanges are a wonderful invention by mankind.

One can participate in all kind of businesses. Banking, insurance, (electric) power producer, properties (all kinds too, from office buildings, malls to warehouses etc) and so on, think about it for a moment, WONDERFUL isn’t it, no need to get one's hand dirty.

So be business like, a great sifu said, you all know who said that, and the return will be taken care of.

Here is the revised projection for 2019 to 2021.

The oil sold for Anasuria Cluster already confirmed (524,432 barrels) by Management. They implied that the price is good (hear the web-cast, please).

Normally, quarterly estimate is spurious. But for interest, due to the (Anasuria) production carried over to Q1 ’19, and in keeping with the off-take at N Sabah of previous quarters that alternate between large / low quantities sold, Q1 ’19 assume only about 264,500 (N Sabah) barrels sold.

Oil price is in keeping with that obtained from EIA but averaged while exchange rate is based on Bank Negara and also averaged.

This (profit) estimate ignores the reserve upgrade of Anasuria Cluster.

You may ask why the daily productions are less than those stated in the cash-flow done by LEAP. It is better to be conservative, margin of safety, one never know what the management may do, defer another off-take, things like that.

Conclusion

Hibiscus is going to double their profit in the coming financial year 2019.

The assets (both Anasuria Cluster & North Sabah) are more valuable. Net tangible asset per share is going to be about RM 0.90 this coming first quarter.

With pending sanction on Iran by US, there will be less oil supply; Venezuela is in free-fall, the human tragedy unfolding is sad; Libya, civil commotion again flared up; Saudi, Saudi, Saudi, there is a school (of thought) that think they have this wonderful spare capacity where just turn the tap (like water tap) oil will just gushed out by the bucket full. The recent increased supply from Saudi, the other school thinks that it was from storage. OIL PRICE SHALL REMAIN ABOVE USD 70 FOR THE NEXT SIX MONTHS (baring a recession).

There is so much potential for production to be enhanced, that the probability for higher production is there.

Disclosure : I and my family own shares in Hibiscus.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. Buy / sell at your own risk.