Liew Jia Teng/The Edge Malaysia

March 30, 2020 14:00 pm +08

This article first appeared in Capital, The Edge Malaysia Weekly, on March 23, 2020 - March 29, 2020.

I am totally lost for words. I don’t think I can understand the market or the economy anymore. I have suffered huge losses. If I had known, I would have got out,” a local seasoned investor, regarded by many as an investment guru, tells The Edge over the phone.

“If I had known …” is a refrain more commonly heard from mom-and-pop investors. Perhaps everybody is equal in the eyes of the bear. Perhaps there is no shame for any investor, big-time or small-time, who has suffered crushing losses in the current coronavirus market crash.

In fact, not even Warren Buffett, one of the most famous investors of all time, is immune to the crash.

Going by GuruFocus calculations, Buffett’s equity portfolio has lost about US$80.2 billion, or 32%, since the US markets began sliding into bear territory in February.

Although the crash owing to Covid-19 is not the worst we have seen — 1973, 1987, 1997 and 2008 all saw similar or worse falls — it should be noted that those previous hammerings were preceded by big bull markets.

“But today, the crash was preceded by five years of bad performance. Those previous crashes all turned around quickly because our country was growing well. This time, I am not so sure [if we can recover quickly],” says the local seasoned investor, who prefers to remain anonymous.

As the global spread of Covid-19 and collapse in oil prices are likely to undermine economic activities and disrupt supply chains, stock markets appear to have priced in not only a recession but also a significant decline in earnings.

Central banks around the world are slashing interest rates and pumping in trillions of dollars of temporary liquidity into financial systems.

But it appears that these massive steps — deemed by many as pressing the panic button — are not enough to calm investors and ease disruptions.

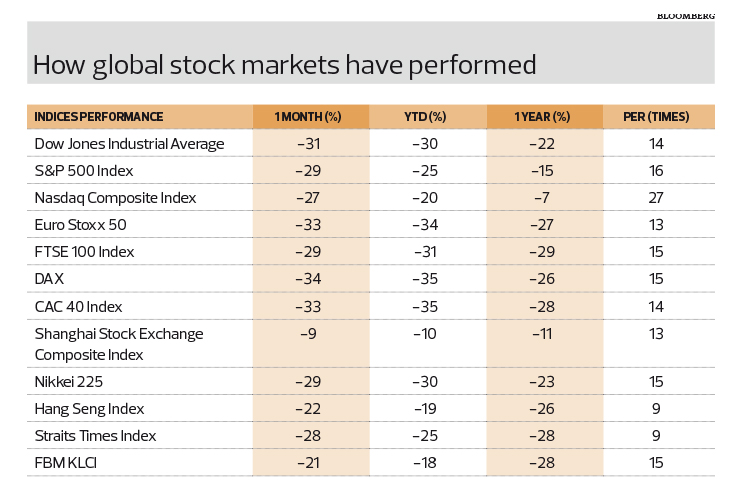

Over the past month, the three major indices of Wall Street, namely the Dow Jones Industrial Average, S&P 500 Index and Nasdaq Composite Index, have declined by about 30%.

Likewise, Japanese and European stocks have also dropped between 29% and 34%.

Interestingly, Hong Kong and Singapore equities are currently trading at a single-digit price-earnings ratio (PER) of nine times, after declining 22% and 28% respectively.

At home, although the FBM KLCI also lost 21%, its PER remained relatively higher at 15 times.

Nevertheless, certain blue-chips are now trading at single-digit levels, which suggest cheap valuations.

Although the Covid-19 pandemic seems to have presented investors with a once-in-a-decade opportunity, or perhaps the best opportunity since the 2007/08 global financial crisis, market experts whom The Edge spoke to have warned that the worst may be yet to come.

Malaysia ‘not particularly cheap’, weighed down by other issues

According to Value Partners Group Ltd founding chairman and co-chief investment officer Datuk Seri Cheah Cheng Hye, foreign investors are worried about Malaysia’s recent political problems and concerned over the continuing weakness in the ringgit as well as the country’s structural challenges.

“I remain very cautious about the Malaysia market. At 15 times earnings, it is not particularly cheap. I think Malaysia has not seen the worst of the coronavirus outbreak,” he states.

Cheah opines that Malaysia will find it difficult to raise its productivity level due to poor investment sentiments at home and the reluctance of foreign investors to come in.

“The economy is in trouble if productivity doesn’t rise,” he observes.

However, Cheah acknowledges that buying opportunities have emerged across the region, as many Asia-Pacific stocks have become “too cheap” and some asset classes, particularly gold, look oversold.

“But I would advise investors to be selective. In particular, I think New York could have another 10% to 20% downside from the current level,” he warns.

“In a good-case scenario, a vaccine for the coronavirus can be found within this year and this would help investor sentiment to recover. But we cannot count on this — it may or may not happen,” Cheah stresses.

Affin Hwang Capital deputy group managing director Yip Kit Weng concurs, saying that despite the FBM KLCI’s year-to-date loss, there may be further downside. Moreover, the sharper correction in regional markets further accentuates the FBM KLCI’s valuation premium.

“At current FBM KLCI PER valuations, market expectations are potentially still too optimistic and we think that there is likely further downside for the benchmark index should there be a further selldown in global equity markets. The sharper corrections in regional and global markets are also making the FBM KLCI look relatively unattractive,” he points out.

Thus, Affin Hwang Capital has further cut its FBM KLCI corporate earnings growth forecast from 1.3% to -4.7%, to reflect its cut in gross domestic product (GDP) growth to 3.3% from 4% — its second reduction for the year.

“Alongside a higher market risk premium, we lower our FBM KLCI 2020 year-end target to 1,200,” says Yip.

With the announcement of a RM20 billion economic stimulus package, he believes domestic demand and private consumption will remain supportive of growth despite expanding at a slower pace.

“We believe Malaysia will not fall into recession. There are many good companies and investable stocks but fundamentals take a back seat given that Covid-19 is affecting both supply and demand chains. This, coupled with the current low oil price, adds more pressure on the Malaysian stock market,” says Yip.

Despite the substantial cut in corporate earnings growth forecast, Affin Hwang Capital chief economist and head of research Alan Tan suspects that this may still prove too conservative and that there could be further downside risk to earnings, should the Covid-19 pandemic be prolonged.

“In view of our earnings revisions, downgrades to target prices and the increased volatility that we are anticipating for the market, we review our sector positioning and largely move away from cyclicals,” he says.

Affin Hwang Capital has downgraded plantations and electronics manufacturing services from “overweight” to “neutral”, and oil and gas, transport and logistics, utilities, financial, and gaming sectors from “neutral” to “underweight”.

It is only “overweight” in relatively defensive sectors, namely healthcare and real estate investment trusts (REITs).

“We are still convinced of the growth story in the rubber gloves space. The weak ringgit against the US dollar should be positive for glove makers,” says Tan.

Geoffrey Ng Ching Fung, investment adviser and director at Fortress Capital Asset Management (M) Sdn Bhd, agrees that Malaysian stocks are pricing in an earnings decline.

“If we assume no PER contraction on the index, then [we expect] about 20% decline in market earnings,” he says.

Stay calm as the panic will pass

With the exception of the 1997/98 Asian financial crisis, Ng highlights that the FBM KLCI is near the bottom of the valuation range on a price-to-book basis for most of the previous economic or pandemic crises.

“We would agree that the market is in a complete risk-off, panic-selling mode and certainly pricing in an imminent recessionary environment, characterised by significantly slower near-term economic activity, consumption, exports and price pressure on real assets,” he says.

Investors may look to be overreacting but, at this time, it is a total risk-off measure, Ng says, so in-the-money stock investments generally get sold first, followed by cut-loss positions if liquidity requirements are still unfulfilled.

While it would be safe to assume that dividend payouts will fall across the board for companies that experience weaker earnings and cash flow during the period of the pandemic, Ng insists that he will still be looking for companies that historically boast high payout ratios as he expects such a trend to continue or even rise as a percentage of earnings.

“Some of these sectors include breweries and tobacco. However, this may be offset by increased pressure from the government through the raising of excise taxes on such sectors in the near future,” he says.

Ng’s advice to investors is to stay calm as the panic will blow over.

“Take the China market’s recent lead, where there was evidence that the Covid-19 outbreak was starting to be controlled. The world markets, including Malaysia, will stabilise and recover once the pandemic is seen to be under control.”

Ng is of the view that the current Covid-19 crisis certainly presents one with the best opportunities to buy stocks on the cheap but there are caveats.

“Asset prices were already ripe for a correction given the long-running equity bull market. The onset of Covid-19 has released a lot of pressure from this ‘late-cycle bull market’, which has reset asset prices to more realistic fundamentals. If the world economy doesn’t fall off a cliff and provided that the pandemic doesn’t last too long, we do see this as a great opportunity for investors,” he says.

More of a crisis for the West

Value Partners’ Cheah points out that based on historical experiences, a pandemic like Covid-19 will go away over time.

“Indeed, China is quickly resuming full production and the country will still be able to enjoy economic growth this year of around 2.5%,” he says, noting that while the coronavirus has caused a global crisis, it is much more of a crisis for the US and Europe.

“Of course, China and Japan are also suffering, but frankly, the crisis is much more serious in the West, particularly in the US.”

Cheah says the Chinese economy is driven by domestic consumption and investment, rather than exports, so the slowdown in global trade has only a limited impact on China.

“In contrast, the impact on the US, and to some extent Europe, is much bigger. This is because the US economy was already over-extended by the beginning of this year. The New York stock market had reached a historical high, while the US interest rates were at historic lows,” he continues.

Cheah observes that the US economy had been enjoying an expansion for over 10 years — a record length of time — and thus, the West was fragile and vulnerable when the pandemic hit.

In many ways, he says, the disease was not the cause of a crisis but acted as a trigger.

“This is very different from China where the disease put a brake on an expansion that was moving along nicely. The outcome is going to be that the West will face a financial and economic crisis that will not go away quickly,” Cheah remarks.