Hey, once again thanks for viewing my blog! Last week, KLCI was seen to be staging a rebound with a strong bounce-off the 1500 physiological level. Let’s keep our fingers crossed on more upside in the local bourse as we continue to search for the alpha stocks for this week.

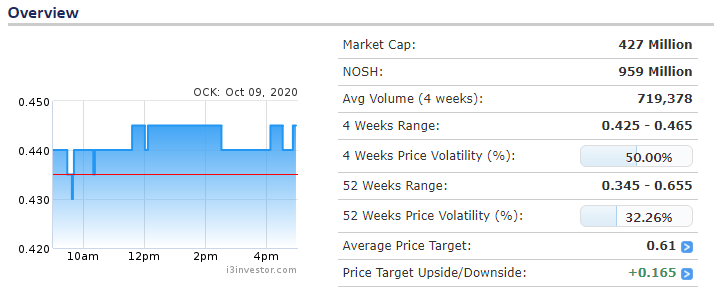

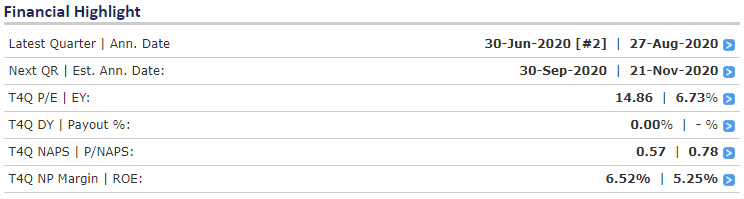

1. OCK (0172)

Catalysts

- Well-positioned for 5G Rollout

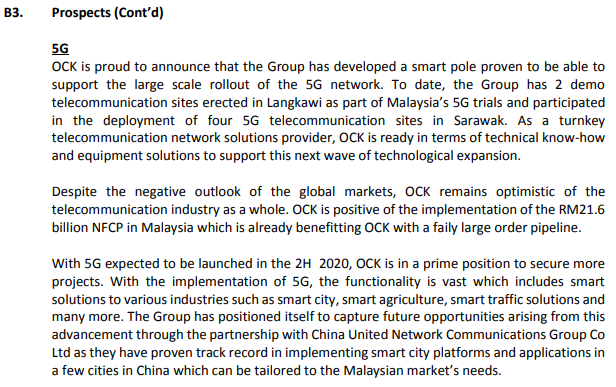

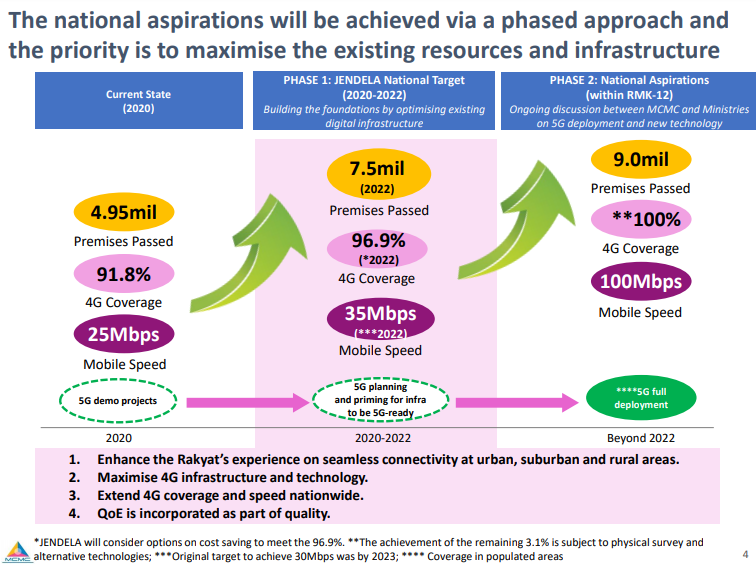

OCK had highlighted in its 2QFY20 quarterly results that the company has developed a smart pole proven to be able to support the large scale rollout of the 5G network.

In line with the company prospects highlighted by OCK, the current government had announced the Jalinan Digital Negara (JENDELA) initiative on 29 August 2020. The 5G planning and priming for infrastructure to be 5G-ready will be executed from 2020 to 2022.

(Source: https://www.mcmc.gov.my/skmmgovmy/media/General/pdf/NDIL-Report.pdf )

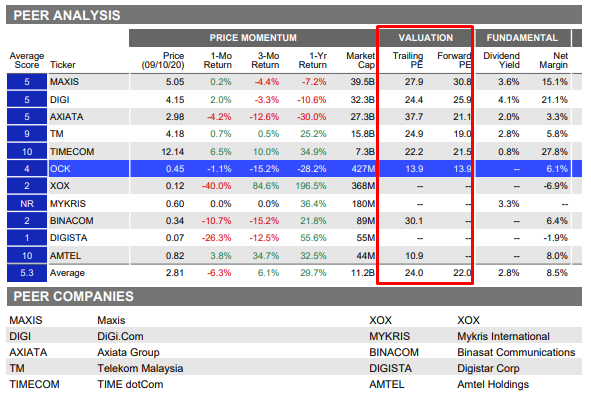

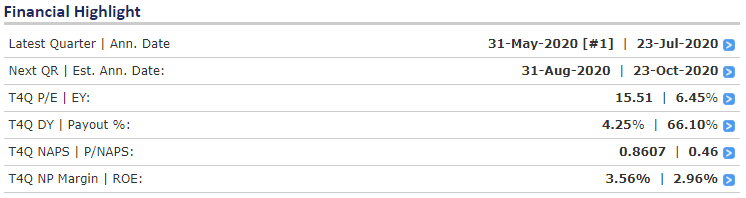

2. Reversion to Sector Mean P/E

Based on peer analysis, the Trailing P/E of OCK at 13.9x is relatively low as compared to its sector average P/E of 24.0x. Even at a conservative take profit P/E of 20-22x, there is at least 40% upside to OCK.

Risks

- Delay in 5G initiative due to a potential change in government

- Higher than expected CAPEX resulting in potential lower bottom-line

- Potential increase in debt burden

2. PANTECH (5125)

Catalysts

- Recovery in Oil & Gas Sector

PANTECH is set to benefit from the recovery in Oil & Gas sector as their client base mainly comprised of O&G players.

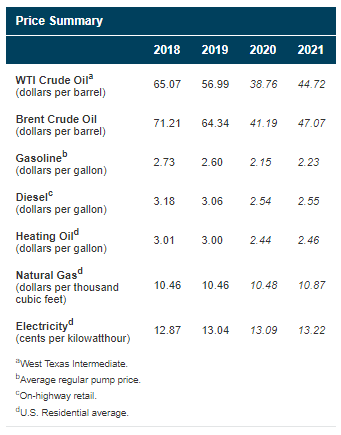

Now let’s look at the Brent Crude Oil prices to determine the performance of the sector.

EIA forecasts monthly Brent spot prices will average $42/b during the fourth quarter of 2020 and will rise to an average of $47/b in 2021.

(Source: https://www.eia.gov/outlooks/steo/)

2. Reversion to Sector Mean P/E

![]()

Based on peer analysis, the Trailing P/E of PANTECH at 15.5x is relatively low as compared to its sector average P/E of 20.0x. Even at a conservative take profit P/E of 20-21x, there is at least 30% upside to PANTECH.

Risks

- Unexpected increase in the prices of raw materials

- Unexpected drop in oil prices

- Unexpected poor performance from associate company (Tuah Nusa Sdn. Bhd.)

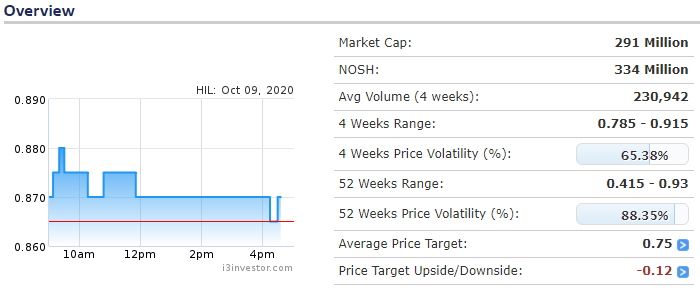

3. HIL (8443)

Catalysts

- Venture into Production of PPE

HIL had mentioned that the company had started to venture into manufacturing Personal Protective Equipment products by producing face shields and face masks.

In addition, HIL had announced that the company has received approval from the Medical Device Authority (MDA), which is part of the Ministry of Health for the manufacturing of its 3-ply surgical grade face mask and face shields.

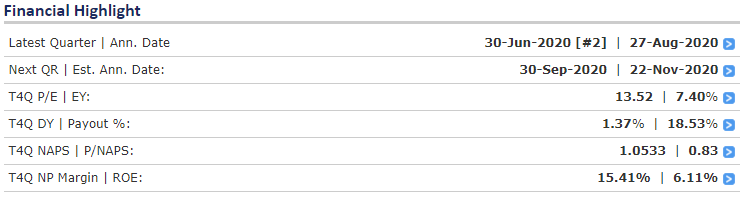

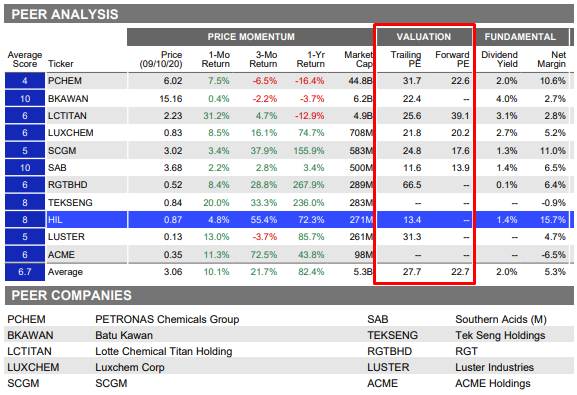

2. Reversion to Mean Sector P/E

Based on peer analysis, the Trailing P/E of HIL at 13.4x is relatively low as compared to its sector average P/E of 27.7x. Even at a conservative take profit P/E of 20-22x, there is at least 50% upside to HIL.

Risks

- Higher than expected CAPEX on manufacturing of PPE

- Slower than expected recovery in the Automotive sector

- Lower than expected profit recognition in its property projects

DISCLAIMER: The information above is provided for education purpose only and does not constitute a buy or sell recommendation. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of you acting based on this information.

https://klse.i3investor.com/blogs/alphastockhunt/2020-10-11-story-h1534586202-Alpha_Stock_Hunt_12_16_Oct_2020.jsp