Time right for share buybacks despite economic downturn

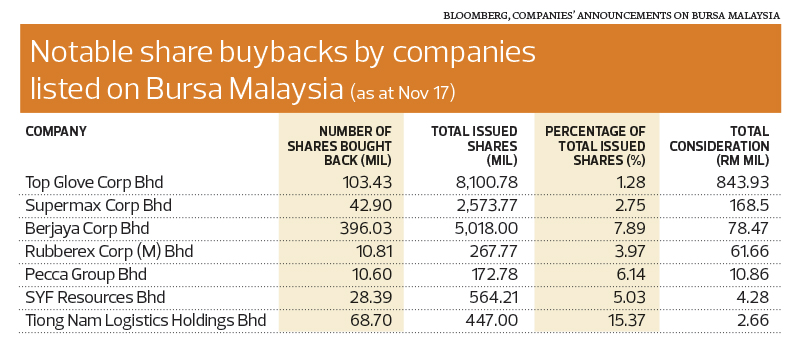

THE world’s largest glove maker, Top Glove Corp Bhd, has repurchased an astounding RM843.9 million of its shares so far this year.

To put things into perspective, that amount is 5.6 times the investment made by property developer Mah Sing Group Bhd to build a rubber glove factory with an annual capacity of 3.68 billion pieces of gloves.

It is not a secret that a number of companies listed on Bursa Malaysia have been engaging in share buybacks quite aggressively this year. Apart from Top Glove, the more notable ones are two other glovemakers, Supermax Corp Bhd and Rubberex Corp (M) Bhd, and Berjaya Corp Bhd.

Although the total number of shares bought back by companies this year does not differ much from that of last year, the buybacks have attracted more attention for several reasons. First, given the dire state of the economy, the thinking is that companies should be conserving their cash. Second, it is probably because the glovemakers have been actively doing so.

For example, Top Glove did not engage in share buybacks at all last year while Supermax only purchased slightly more than 11 million shares in 2019. This year, Top Glove acquired 103.4 million shares or 1.28% of its total share base, while Supermax repurchased 42.9 million shares or 2.75% of the total issued shares.

The same goes for BCorp, which did not engage in share buybacks last year. However, it has spent RM78.5 million buying back 396 million shares on the open market this year.

The fact that BCorp had slipped into the red for the financial year ended June 30 but still engaged in substantial share buybacks this year has raised quite a few eyebrows. Should the conglomerate, as well as other companies, spend money on share buybacks when the country is experiencing an economic crisis?

For Imran Yusof, head of research at MIDF Research, it all depends on the capital structure of the company, the sector it is in and the outlook for the economy. “Share buybacks are an efficient method of putting money back into shareholders’ pockets. The share repurchases reduce the number of existing shares, making each share worth a greater percentage of the corporation,” he says.

“Therefore, if the management believes the economy is turning around and that the company is undervalued, then it is the best time for a share buyback. Basically, it is putting to use the excess cash that the company may have into an instrument that could generate returns.”

In FY2020, BCorp made a net loss of RM101 million, compared with a net profit of RM121.5 million in the 14 months ended June 30, 2019 (14MFY2019), due to the impact of Covid-19 on its businesses, which range from gaming to hotels and resorts. Nevertheless, the group still had huge cash holdings and bank balances of RM855.9 million as at June 30, as well as RM493.93 million in deposits with financial institutions.

However, its short-term borrowings stood at RM2.3 billion. Net cash generated from its operating activities plunged drastically to RM25.43 million in FY2020 from the RM513.4 million generated in 14MFY2019.

After announcing its FY2020 results, BCorp said the business operations and performance of the group for the financial year ending June 30, 2021, would continue to be challenging because of the pandemic, which is still adversely impacting the global economy. However, the group said it was confident of weathering the unprecedented challenge.

Imran says the decision to buy back shares also depends on the timing, reasons and method — whether through borrowings or with excess cash. “In a situation where the market is undervaluing the stock, then it may be acceptable for the company to engage in buybacks. However, if it is to maintain a certain market capitalisation or for optics, then it may be better for the company to utilise its cash to invest in its business [for example, capital expenditure] or return it to shareholders.”

He adds that in times of economic uncertainty, the company may deem it too risky to invest more money in the business. When the market recovers, it can release the shares to be sold to the public or it can reward shareholders through a dividend in specie.

However, Imran opines, it is possibly better to put the funds in normal treasury operations such as deposits and fixed income. But that depends on the management’s view of the economic direction.

Kaladher Govindan, head of research at TA Securities, is of the view that it makes sense for some companies to engage in share buybacks now because of the cheap valuations, plus a recovering economy. The management knows that share buybacks are better than acquiring new companies, he notes.

“It depends on their capital structure. There is no harm in having some borrowings. The economy is already in recovery mode. And specifically on the glove makers, their earnings outlook is strong,” says Kaladher.

“Share buybacks enhance earnings per share (EPS) when shares are cancelled. The company can also reward shareholders in the form of dividend in specie. It can be used to alter its capital structure as well.”

It has certainly been rewarding to be a shareholder of the world’s largest rubber glove manufacturer this year as Top Glove’s EPS has risen rapidly due to the strong demand for its products. For its financial year ended Aug 31, its EPS jumped to 15.95 sen in the final quarter from 4.36 sen in the first quarter ended Nov 30, 2019. The spectacular performance enabled the company to declare a total dividend of 18.5 sen per share this year.

On top of that, the group has rewarded shareholders with a bonus issue, on the basis of two bonus shares for every Top Glove share held by shareholders as at Sept 3. This means someone who bought 1,000 Top Glove shares at RM4.70 each on Jan 2 for a total of RM4,700 would have been sitting on an investment worth RM13,780 on Nov 19. The shareholder would have also received RM370 in dividends, or a yield of 7.87% on the original investment.

There is also the possibility of a dividend in specie now that Top Glove has acquired 103.4 million shares through buybacks.

The high demand for rubber gloves since the Covid-19 outbreak in late February has resulted in Top Glove’s net profit soaring more than fivefold to RM1.9 billion in FY2020. Its cash and bank balances jumped more than sevenfold to RM1.21 billion as at Aug 31, while net cash flow generated from operating activities rose sixfold to RM3.17 billion from a year earlier.

http://www.theedgemarkets.com/article/time-right-share-buybacks-despite-economic-downturn