KUALA LUMPUR (April 26): Interest in the dry bulk shipping segment, a sector that has been off the radar for more than a decade, is getting strong, against the backdrop of surging freight rates driven by an unexpected commodity boom during the Covid-19 pandemic.

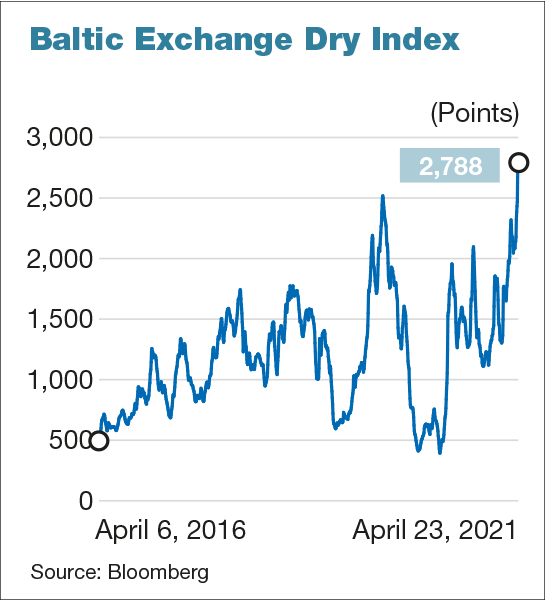

The Baltic Exchange Dry Index, which tracks freight rates across different vessel sizes, started the year higher than pre-pandemic levels, and is currently double its five-year average at 2,472 points as key markets replenish supplies that were drawn down in the year of the pandemic.

Shares of dry bulk carriers, from Thai-listed Thoresen Thai Agencies PCL to Hong Kong-listed Pacific Basin Shipping Ltd, have risen between 63% and 153% in tandem with the bullish charter rates.

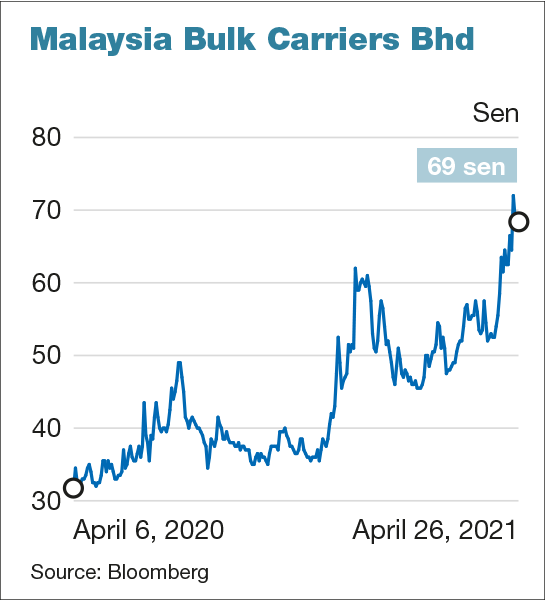

At home, shares of Malaysia-listed Malaysian Bulk Carriers Bhd (Maybulk) have also climbed 58% from their lowest point this year. The stock hit a high of 72 sen, just shy of its August 2019 high of 73.5 sen when shipping rates spiked. Maybulk is trading at 70 sen this morning.

Unlike the temporary spike in shipping rates in 2019, analysts are expecting its levels to remain elevated this time. The commodity boom, further induced by governments pushing for infrastructure projects to drive economic recovery post-Covid-19, comes at a time when newbuild order book is at a low, which points to supply tightness at least until 2022.

Demand outstrips supply until 2022

To be sure, the industry was headed towards market balance since 2016, as fewer new ships were built after more than a decade of suppressed freight rates after the 2003-2008 commodity supercycle.

Noticeably, commodity prices are also at their highest in over two years, with the Bloomberg Commodity Index rising to US$87.33.

While newbuild orders jumped in the first quarter of 2021 in response to the climbing shipping rates, the undersupply situation should persist in the short term as it takes 18 months at the earliest for a vessel to be completed.

Leading shipping analyst Cleaves Securities, in its quarterly report dated April 18, forecasts net dry bulk supply growth of 3.3% year-on-year in 2021, and only 1.7% in both 2022 and 2023.

This compares with a dry bulk demand growth forecast of 10.1% in 2021, before normalising to 3.4% in 2022 and 2.2% in 2023.

“Given the historically low order book, very limited demand growth is needed in order to significantly improve fleet utilisation, earnings and asset prices going forward,” the research house said.

Peter Lindström, head of research for Norwegian shipping firm Torvald Klaveness Group, said in its 2021 outlook that positive demand growth is expected across the board for key commodities, from iron ore to grains and minor bulks. This while fleet growth remains at “historical lows” in 2021 and 2022.

"We believe it is very likely that freight rates will increase in 2021 and 2022 as low fleet growth combines with a seaborne dry bulk trade that recovers from the black swan events of Brumadinho dam disaster [which slashed iron ore exports from Brazil in 2019] and Covid-19 [in 2020].

“We also believe that fleet growth in the next five years is likely to be at low levels due to uncertainties around the choice of fuel and propulsion systems,” he added.

It includes the IMO 2020 regulation which limits sulphur content in ships’ fuel oil to 0.5%. This pushes shipbuilding costs higher, and provides an advantage for shippers with newer, more eco-friendly vessels.

Cautious optimism?

Others also see a tipping point in the sector’s supply-demand dynamics, although at a more conservative level. Moody’s, for one, foresees dry bulk demand to grow by 3%-5% in 2021.

Interestingly, Maybulk also had a more conservative tone on the industry outlook.

"Despite a slower fleet growth, coupled with an order book of less than 6% of fleet capacity, there are influences that are likely to limit dry bulk trade performance in the following months due to divergent growth rates worldwide reflecting variation in pandemic-induced disruptions and the extent of policy support across countries,” said Maybulk in its annual report released on April 16.

“We should be prepared for pressure on freight rates and likely volatilities as the impact of China stimulus wanes and recovery of other economies likely to be uneven during the post Covid-19 pandemic,” the report also said.

Understandably, the company was loss-making in its financial year ended Dec 31, 2020 (FY20). However over the past five financial years, the group has gradually reduced its losses, with positive operating profit in FY18 and FY19.

Having exited the loss-making oil and gas services unit PACC Offshore Services Holdings Ltd in 2018, Maybulk has also completed its fleet sizing to be younger and more eco-friendly.

Maybulk, which is linked to tycoon Robert Kuok, owns and operates 10 vessels with an aggregate carrying capacity of 555,059 metric ton deadweight and an average age of 5.6 years, according to its annual report. Its voyage spans Europe and Australasia.

The fleet comprises three kamsarmax, three supramax and four handysize vessels. These vessel types typically cater more towards minor bulks, grains, and coal more than iron ore, according to 2019 data from shipping firm Torvald Klaveness.

According to Maybulk’s website, its vessels are “largely tramped on the spot and period markets”. It also has a long-term contract worth an estimated RM563 million with TNB Fuel Services Sdn Bhd to ship about 1.5 million tonnes of coal per year to Malaysia until 2031.

Group borrowings have also been pared down from RM543.9 million at end-FY15, to RM237.3 million at end-2020. Cash and cash equivalents stood at RM38.89 million at end-2020, while group accumulated losses stood at RM183.94 million.

At current level, Maybulk's market capitalisation stood at a mere RM700 million.

At 70 sen, the counter is trading near one-fifth of its peak valuation in the 2000s — the good heydays in the previous powerful commodity boom when the Baltic Dry Index rocketed to above 10,000 in 2008 shortly before the onset of the Global Financial Crisis. It then plunged to below 1,000 soon during the economic crisis.

The index is trading at 2,700-level currently.

It’s a long-awaited recovery for the dry bulk shipping segment, and one which Maybulk has worked hard to position itself to benefit from. It's a rosy picture for recovery from here on in — if the upswing in the global economy goes uninterrupted this time.

The following article above is copied entirely from The EdgeMarkets.

https://www.theedgemarkets.com/article/freight-rate-spike-puts-dry-bulk-carriers-back-spotlighthttps://klse.i3investor.com/blogs/kvinvestment/2021-04-27-story-h1564143497-BALTIC_DRY_INDEX_AT_10_YEARS_HIGH_MAYBULK_BERHAD_5077_A_DIRECT_BENEFICI.jsp