BJCORP (3395) BERJAYA CORP BHD Overview

This was a hard one. I had to derive a few figures, such as the result from Berjaya's consumer marketing segment, and make a few other assumptions. I still don't understand their corporate structure. If you can see anything that is wrong, please let me know.

Please be aware that I am not a professional investor- I do this because I enjoy it. This is not advice, and I cannot guarantee accuracy of information included. I make no recommendations for your investing practice.

Berjaya (English: Success) run six core segments and several other businesses. Berjaya came into their current form in the decade proceeding 1984, when founder Mr. Vincent Tan gained control and began to combine a few diverse operations under the “Berjaya” name.

- Motor trading: the sale and maintenance of cars. They are primarily luxury cars (Ferrari, Maserati, Bugatti etc.) sold in the United Kingdom.

- Gaming (gambling): the operation of lottery and other gambling operations and is the major cash contributor. Berjaya may divest parts of this segment due to ESG concerns.

- Marketing of consumer goods: the resale and production of household products- food, cleaning, health and beauty, and other supermarket products.

- Restaurants and café’s: includes management of Starbucks and Krispy Kreme Malaysia, along with several others.

- Financial services: operate under the “Inter-Pacific” heading, offering securities trading services and asset management.

- Property development: involves several ongoing projects in KL, Penang, Hoh Chi Minh City and Hanoi. Property investment is primarily in KL.

- Hotels and resorts: located in KL, Penang, Tioman Island, Kyoto, Iceland, and London, among others.

- Other businesses: education, car trading, waste management, and telecommunications.

Berjaya’s interests and operations are more than those mentioned above- they are an immense web of businesses. Their size is limiting for growth but provides opportunities for synergy. Over the next decade, management aim to streamline by removing dragging segments, and add power to the company engines with greater synergy and a stronger profit drive.

Overview of Industries

Just under 60% of Berjaya’s revenue is from consumers throughout Malaysia. They cater to the essential needs- food, shelter, health, household goods and recreation. Domestic businesses are in established industries that convey predictable value to consumers. Experimental growth businesses comprise a negligible part of the corporation.

International operations vary. The biggest international revenue contribution comes from the luxury motor industry the UK. Car sales income is fairly predictable, but maintenance income is more variable depending on the cost of labor. International hotels and resorts have been severely impacted during COVID but are reliable over the long term. Other overseas operations comprise an insignificant percentage of Berjaya’s overall revenue.

Click here for a table of the profitability of each segment and the impact of some external forces.

Margins are fair in most of Berjaya’s industries. The most influential external forces are the Malaysian economy, the cost of labor, and the Malaysian government’s regulatory treatment of gambling. Regulations are susceptible to change, and the economic outlook is uncertain short-term. But over the coming decades, many believe that Malaysia is fundamentally strong and likely to experience improved business activity and growing wealth. Berjaya’s Asian industries are a prime candidate to benefit, and generally able to adapt well to inflation.

Management

|

Average tenure of directors |

6.42 years |

|

Relevant director’s experience |

-Founder present -Entrepreneurship, government fund management, and large global enterprise management -Engineering and real-estate experience -Significant experience within Berjaya. |

|

Notable other experience |

-Sustainability -Environmental management -Significant international experience. |

|

Board remuneration |

-Founder’s remuneration exceeds that of all other directors combined, at RM20m -Salaries were 71% vs bonuses 2.2% and other emoluments 21% |

|

Board alignment |

-Founder approx. 2.5b shares -Top holding executives 591m and 182m -Significant share-based interests among subsidiary directors -Family connection between 3 directors |

Mr. Vincent Tan is the founder of Berjaya. He is a well-known businessman and billionaire. After began his career as a clerk and salesman, he succeeded as a manager. Mr. Tan gained control of Berjaya in 1984 and has been involved up until the present day. He recently stepped back to become a non-executive, remains the primary controller through his shareholding. His son, Robin, is Deputy Chairman, and daughter Nerine an Executive Director.

Management are a combination of experienced directors who have served since the mid 2000’s, and new recruits from recent years. There is an intention to adapt to societal changes while retaining the experience necessary to manage this large corporation.

In 2021, Mr. Tan stepped back to non-executive status. He stated that his family will also lessen their involvement with Berjaya. This appears to be positive shift for the company, opening the door for other highly talented managers.

Especially promising is the new Chief Executive Officer Jalil Rasheed, who has premier international business experience and was Group CEO for Malaysia’s government fund manager. He is 39 years old and has provided a new sense of clarity to Berjaya after communicating their most recent strategy directly to shareholders.

Strategy

Berjaya is an entity that has historically aimed to acquire businesses for the highest risk-adjusted return on investment. Aspects of Berjaya’s strategy include:

- Unconventional swaps, opportunistic deals, and acquisition out-of-favor businesses with high liabilities to lower the initial cost of investments

- An effort to participate in diverse businesses, limiting exposure to industry specific risks

- Cooperation, creating synergistic efficiencies

- Diversification of expertise, granting individual managers access to knowledge of various industries with which they interact

- Flexibility, as management can enter and exit businesses and adapt to market conditions.

The strategy has a few limitations. When management exit and enter new lines of business too frequently, there is a lack of depth and focus on their investments. Additional inefficiencies arise when an overwhelming amount of information associated with many operations must be coordinated. Profits from successful businesses are sometimes used to help weaker businesses rather than being reinvested into strength.

For the past decade, Berjaya have struggled to generate good total returns. New leadership have helped to create a three-year plan to re-define Berjaya and deliver better results:

- Divest dragging businesses, focusing on profitable verticals

- Restructure into a five-segment corporation, rather than a diversified conglomerate: retail, food, real estate, hospitality, and services

- Enhance cooperation

- Improve motivation with stronger performance incentives

- Implement a dividend policy

- Reduce debt by half

- Restructure board with more independent directors

- Use accumulated data more effectively

Within their strategy is a vision of sustainability. The most profitable segment of the business, gambling, is often called unsustainable and unethical. No explicit plan for this segment exists, but management have said that it is not possible for gambling to be a part Berjaya with their long term ESG goals. It is assumed that the segment will be sold at the highest possible price, rather than at the earliest convenience.

Quality of Earnings

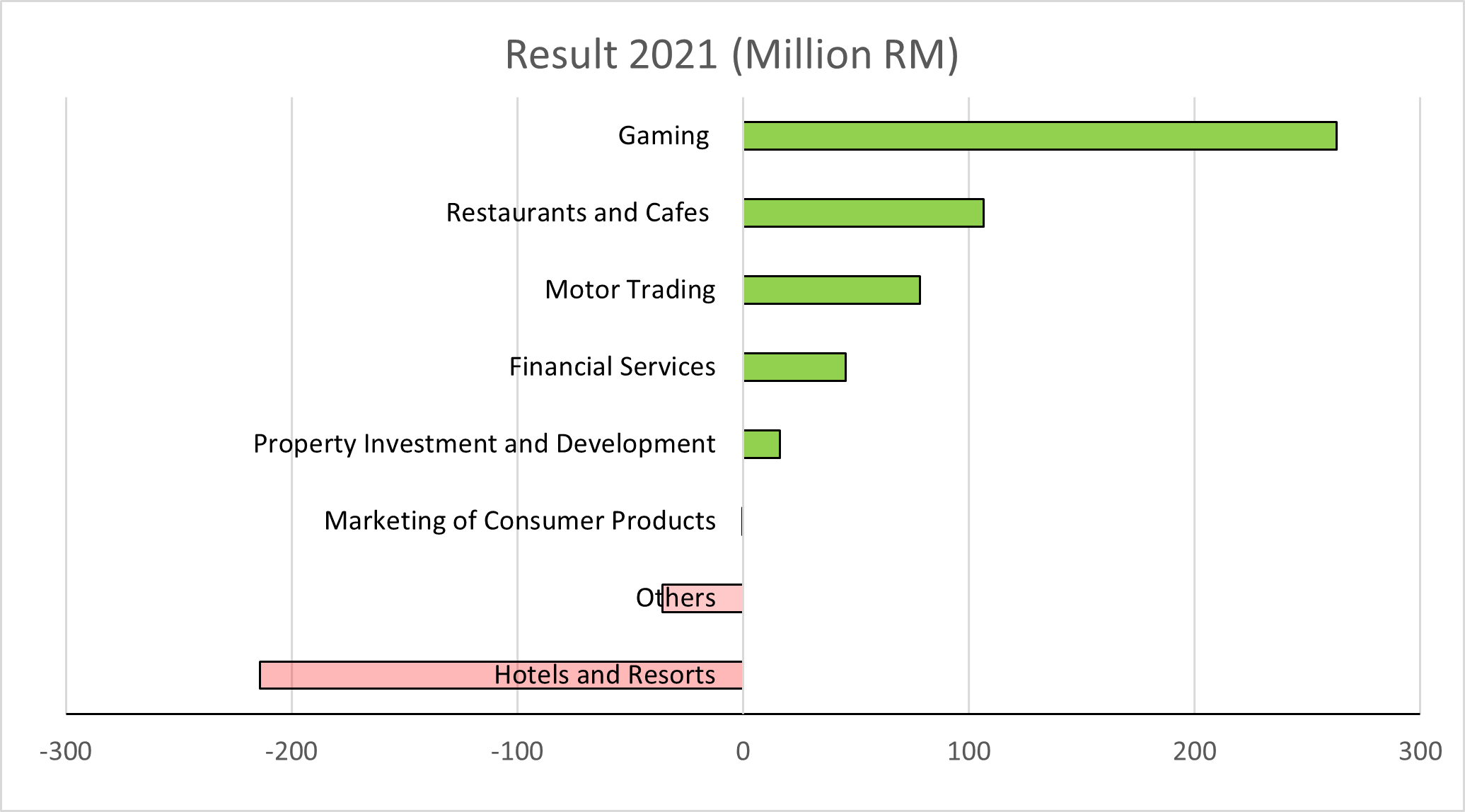

Berjaya’s yearly earnings appear unpredictable and are highly influenced by their investing activities and impairments. Average income for the 6 years pre-COVID was RM61m, although most years yielded a loss. The pre-tax result for FY21 is depicted below:

Each of Berjaya’s major businesses provide goods or services that deliver reliable value to consumers. Besides “others”, each segment was profitable between 2016 and 2019, with losses in four segments in 2020, and one segment (Hotels and resorts) in 2021.

Restaurants and café’s deliver the highest quality earnings, with promising growth over the past 5 years, near doubling between 2016 and 2020, and tripling in 2021. With the incorporation of proven brands like Starbucks and Krispy Kreme, this segment is likely to have a strong future.

Financial services have delivered inconsistent earnings, with minimal growth. The industry has been recently tough, and earnings are highly dependent on economic conditions.

Marketing of consumer goods is a large segment that runs on tight margins. Earnings have grown in line with industry expectations in the past 5 years. The segment is currently evolving with an influx of online sales and in-store technological evolution. This could help to expand margins by reducing overheads and automating the customer experience in store. The segment also generates significant consumer exposure, providing a medium for interaction between Berjaya and their customers.

Motor trading and property are similar in what they provide. While earnings vary from year to year depending on liquidity, they are decently profitable, and based upon resilient underlying assets.

Gaming provides the most historically reliable profits, but negative sociopolitical perceptions are a threat. This segment should provide substantial capital upon divestment, though it may take a few years to sell.

“Others” contains various smaller businesses, including waste management and telecommunications. It is possible, though not dependable, that some of these businesses could deliver significant profits in the future or provide substantial synergistic value.

The conglomerate nature of Berjaya can both corrode and enhance earnings. Administrative expenses are very high, amounting RM1.5b in FY21 compared to RM7.4b revenue. The impact of this has been mediocre total profitability for Berjaya, making an EBITDA of around 9% in the years leading up to COVID, and net losses in most years.

On the other hand, there are benefits provided by cooperation. Segments can interact in a way that enhances profitability by having a more intimate understanding of where efficiencies can be created. Their restaurants and cafés, consumer goods, accumulated data, and Berjaya’s access to 7eleven (of which Berjaya have substantial ownership) are candidates for cooperation as a food and household goods e-commerce platform. This has not been proposed by the company, and may be difficult due to franchising rules, but it is an example of how Berjaya could enhance cooperation and improve returns going forward.

The majority of Berjaya’s revenue, from a diverse combination of essential goods and services and appreciating asset classes, is well protected. The remaining third, from gaming, is both an excellent provider of cash and the biggest threat to the company.

Financial strength

A few figures relating to Berjaya’s balance sheet:

|

|

Value (million RM) |

|

Working land and buildings |

2102.9 |

|

Investment properties |

1000.7 |

|

Land for development |

2238 |

|

All other inventories |

1335.3 |

|

Vehicle stock |

255 |

|

Gaming rights |

3437.2 |

|

Cash and equivalents |

1267.4 |

|

All other assets |

8486 |

|

Total debt |

5025.6 |

|

All other liabilities |

6189.3 |

|

|

|

|

Net assets |

8908.5 |

Berjaya carry substantial debt. Property and gaming rights assets are their biggest assets. Most of their assets are dependent on successful execution to realize their full value.

The balance sheet is satisfactory, but Berjaya will struggle unless economic conditions and the property market improve. They may be forced to sell assets (ie. gaming related assets) prematurely and at a discount to meet debt payments. Berjaya’s tangible value is around RM1.25b.

Capital allocation

Acquisitions and new lines of business are the major investing activity throughout the history of Berjaya. Sports Toto, the gambling operation, was the first major incorporation and provided excellent returns. Most acquired businesses are in their established consumer industries, although others are in new lines of business, like luxury motor trading.

Recent acquisitions have a stronger focus on existing segments- restaurants and cafés, property development, and hospitality have each incorporated new businesses in the past year.

Berjaya alter their level of ownership over time. For example, Berjaya increased their ownership of Starbucks from 50% to 100% in 2014, but have reduced ownership of Berjaya Land, Berjaya Assets, and Berjaya Leisure since. Divestments are a common method of generating capital for other investments.

Going forward, management aim to acquire new businesses with an emphasis on existing segment verticals. In greater focus is the divestment of businesses that do not create synergistic value or are potentially damaging to the company.

Increasing core capacities is undertaken in selected segments. The greatest recent recipients in the last 5 years were property investment and administrative capacity.

Dividends are issued under no specific policy, depending on the needs of the company. The last dividend yielded 2.3% in 2016.

Buybacks occur when they are perceived as the best use of capital. Over the past three years, buybacks have yielded shareholders 15.63% (2.19% FY19, 10.58% FY20 and 2.86% FY21), taking advantage of COVID’s impact on the market.

Dilution is rare and minimal- the largest dilution adjustment in recent years was 2015, where the effect on exercise of options was (RM3.8m) vs RM846m attributable profits.

Debt maintenance is ongoing. Current debt is excessive, and management aim to allocate the proceeds of divestments to reduce it in coming years.

Risks and threats

Gambling operations: Their biggest contributor of income is also the biggest risk to the company. Ethical views differ, but the general agreement is that gambling harms society. While Berjaya appear to be waiting for a decent price for the business, the unpredictable political conditions in Malaysia mean that the regulatory outlook is uncertain. Should regulations change, the value of this business could be deeply impacted for better or worse. The fate of this segment could decide the fate of Berjaya.

Stagnation: A large administrative burden, lack of focus, and excess of businesses are ongoing problems. Revenue and earnings have shown no growth in the past 5 years. Promises to restructure have been broken in the past.

Corruption: With more business activities and more employees, simple probability dictates that there is a higher chance of illegal corruption being present at large corporations like Berjaya. Because many of their businesses require the support of regular consumers, a single high profile corruption event could have substantial negative effects.

Economic exposure: The business is highly exposed to broader economic health. While motor trading is not exposed to the Malaysian economy, all other segments are. Liquidity is necessary for Berjaya to continue, and without improvement in property, consumer spending, and financial markets, Berjaya will struggle.

Concentrated founder risk: While Mr. Vincent Tan is responsible for Berjaya’s success, his level of influence creates a potential for unchecked mistakes. His children are on the board, and his salary is very high. These issues could reduce the quality of the board- if Mr. Tan’s salary were spread among directors, Berjaya may attract better talent. If similar recruiting and salary decisions are part of the company culture, there is a risk of a lack of talent throughout.

Strategy risk: Berjaya rely on businesses in mature industries with ongoing competition. Many of their businesses have tight margins. Continuing with tight margins is not likely to be successful, so Berjaya must execute a new strategy.

COVID: Their hospitality businesses are highly affected by COVID and produced the biggest drag on the company in the past year. A resolution and return to travel are essential for Berjaya to return to profit.

Balance sheet: Berjaya’s financial position means that all other risks are amplified. They may be forced to make value sacrificing sales of core businesses to continue, should any of the above risks materialize. Any assets sold at a discounted price would degrade Berjaya’s net assets.

Valuation

Berjaya have not earned a sustainable profit in the last decade. Valuing the company based on earnings is difficult due to their complex investing activities, but it should be noted that revenues are usually above RM7b compared to a current market cap of RM1.4b. With assumed revenue of RM7b, Berjaya need to earn a profit margin of 2% to result in a PE of 10. With a 10-year median free-cash-flow margin of 2.5%, and gross profit margin of 31.1%, this looks achievable after some work.

Berjaya’s enterprise value to FCF is 1.5. Free cash flow is Berjaya’s most consistently growing metric, at a CAGR of 15.4% over the last 10 years.

Berjaya’s tangible value is reported at RM1.25. A substantial portion of their assets are intangible, or of unreliable value. If liquidated at full value today, Berjaya would return value to shareholders worth slightly less than a share’s price.

While the company have exhibited poor recent performance and a vulnerable balance sheet, they own some businesses that can provide consistent, high returns in the future. They have all the necessary ingredients to perform well. If they can execute their newest plan, it is highly probable that Berjaya will generate the profits necessary to demand a higher share price.

A rough sketch of their future earnings might include the sale of their gaming operations which could help lower their debts but would reduce revenue to around RM4.5b. If they can cut administrative costs and less promising businesses, and focus on their highest margin operations, they may earn consistent a net profit margin of, say, 5%. This would result in net income of RM233m, and a PE of 6 at the current price. Further synergies could improve margins. After this, growing revenue is largely industry dependent. With luxury cars, Malaysian property, and the broader Malaysian economy each predicted to grow at 5-10% CAGR, Berjaya could begin to grow revenue and earnings, and hence demand a PE above 6, delivering a price that exceeds the current valuation.

Conclusion

Berjaya is an immense entity built on the capital allocation activities of Mr. Vincent Tan, who acquired several diverse, high-quality businesses, beginning with their gambling operations, and more recently including Starbucks, Krispy Kreme, and luxury car trader H.R. Owens. The collection of businesses is broadly consumer-facing, and heavily dependent on market conditions for success. They occupy proven sectors and deliver predictable value to millions.

The goods and services provided are often useful for other businesses within the company. Creating synergies between their highest quality businesses is part of Berjaya’s medium-term strategy. Reducing other disconnected or risky operations is another part of that plan, and at the heart of this strategy is Berjaya’s gambling segment.

Selling the gambling segment should generate billions in capital, but it may take some time, and the longer it takes, the higher the risk of crippling regulatory changes occurring in the interim. On the other hand, the regulatory environment could improve. The outcome for this segment will heavily impact the future of Berjaya.

Their strategy was communicated to shareholders by Jalil Rashid, one of several new faces at Berjaya. With Mr. Tan and other family members stepping back, there is a chance of some material change taking place at Berjaya.

Change is essential going forward- the past decade has been a stagnant one. Administrative costs and debt are excessive, and a drag on Berjaya’s potential future earnings.

The biggest risks to the business can be summarized as a lack of execution and poor economic conditions. Simplifying operations is a difficult task in such a large business and realizing the value of their assets requires patience. If either of these tasks go wrong, the business will be worth less in the future.

But if things go well for Berjaya, they should return to growth after

some consolidation. Achieving a net margin of around 5% and exhibiting

growth in ex-gaming revenue would earn Berjaya a significant re-rating,

which appears entirely reasonable with the high-quality businesses they

own. In any case, Berjaya’s diversity should protect them from abject

failure. In my opinion, Berjaya is a worthwhile investment with a

reasonable chance of providing good returns.

https://klse.i3investor.com/blogs/gregorythe2/2021-11-21-story-h1594582177-Berjaya_BJCORP_Overview.jsp