CYPARK 5184 CYPARK RESOURCES BERHAD’s debt and cash flow problems spook investors

THE share price of renewable energy (RE) firm Cypark Resources Bhd experienced a meltdown last week on concerns over its debt and cash flow position as well as its ability to execute power projects it has in hand.

Shares of the Main Market-listed company plunged 41% within a week, from 69 sen on May 20 to 40.5 sen last Friday, translating into a market capitalisation of RM241.57 million. Following a 55% year-to-date drop, the counter is currently trading at a historical price-earnings ratio (PER) of merely three times.

Concerns have been raised over construction delays of Cypark’s ongoing projects, including its floating solar plant in Tasik Danau Tok Uban (DTU), Pasir Mas, Kelantan, and its solid waste modular advance recovery and treatment waste-to-energy (SMART WTE) plant in Ladang Tanah Merah, Negeri Sembilan.

Cypark group CEO and non-independent executive director Datuk Daud Ahmad, it appears, is making an attempt to calm investors.

In a forwarded message sighted by The Edge, a research analyst who claimed to have contacted Daud says the management reaffirms there is no change to Cypark’s company’s fundamentals, while business remains status quo.

For the floating solar project in DTU, Daud apparently told the analyst that solar panel installation has been completed and it is pending construction of Tenaga Nasional Bhd’s infrastructure facilities, such as connection to the grid. Overall, the project is 85% completed.

According to him, the 20mw SMART WTE project is still in the testing and commissioning stage, while earlier delays were mainly due to travel restrictions, as foreign experts were only allowed to enter Malaysia from April.

Cypark apparently expects the new target commercial operation date (COD) for both plants to be sometime in September. The management also appears to have indicated that Cypark does not require any further funding for its ongoing projects, as the group has secured enough funds from its latest placements of shares.

At press time, Daud did not respond to The Edge’s requests for comment, nor did he verify that he had spoken to the analyst.

A 56-year-old accountant by profession, Daud co-founded Cypark in 1999, and is the single largest shareholder with a direct stake of 6.92%.

The Employees Provident Fund Board owns a 5.95% stake in the company, which is currently undertaking the operation and development of 400mw worth of RE projects in Malaysia.

Another substantial shareholder of Cypark is AmanahRaya Trustee Bhd, which owns about 5%. Among its top 30 shareholders are Public Smallcap Fund, Lembaga Tabung Haji and Phillip Capital Management Sdn Bhd.

A market watcher attributes Cypark’s share price meltdown last week to margin calls and short-selling pressure.

“There have been rumours about something brewing inside the company. But the real concerns are whether or not Cypark can deliver its projects on time. There are concerns as to how Cypark could meet its debt obligation [given the delay in projects].”

He points out that certain quarters had previously raised concerns that Cypark’s cash flow could be strangled by its floating solar projects.

“But then again, this has been talked about over the past two to three years. If these projects are really causing cash flow problems to Cypark, then the management needs to find ways to rectify the situation urgently. The last thing you want to see is a bond default because it will really dampen investors’ confidence,” he warns.

Meanwhile, a solar industry expert believes Cypark has got some good solar assets and solid businesses in its stable but, obviously, it has a few problems on its plate.

“For those who have been following Cypark, they should know that it always has these potential risks. If you look at their intangible assets, cash flow and gearing, these numbers are not looking good,” he says.

Nevertheless, he acknowledges that overall market sentiments have been poor recently and, hence, there is little buying interest in its stock.

“Not only do the major shareholders not have financial resources to stabilise its share price, but worse still, they themselves also seem to be getting margin calls,” he says.

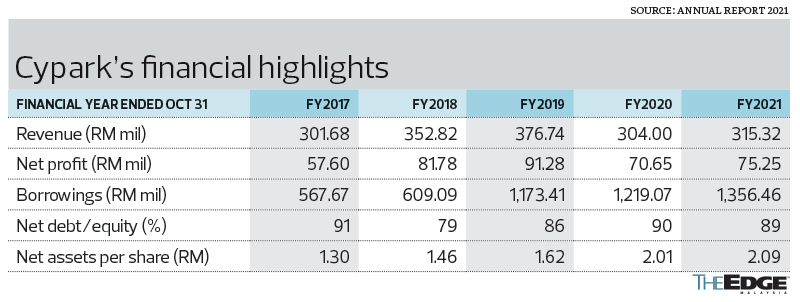

Interestingly, Cypark had been reasonably profitable over the past five years despite the delay in projects. Its net profit grew from RM57.6 million in the financial year ended Oct 31, 2017 (FY2017), to RM81.75 million in FY2018 and RM91.28 million in FY2019, before declining to RM70.65 million in FY2020, and then rebounding to RM75.25 million in FY2021 (see table).

For perspective, Cypark generated a profit before tax of RM96.63 million in FY2021, of which 77% was contributed by its RE division, 15% from waste management and WTE, 7% from construction and engineering, and the remaining 1% from green technology and environmental.

Despite the setbacks to its DTU and SMART WTE plant, Cypark successfully achieved COD for its ground-mounted solar plant in Sik, Kedah, on Jan 1 this year, ahead of the approved COD date by its client. Furthermore, Cypark’s biogas plant in Kg Gajah, Perak, also successfully achieved its COD on Dec 31 last year.

According to its 2021 annual report, the DTU and SMART WTE plants, as well as the 172mw third cycle of its large-scale solar (LSS3) project in Merchang, Terengganu, are targeted to be completed and operational this year.

It is also worth noting that Cypark secured a solar project in Kuantan, Pahang, in June last year under the net energy metering scheme 3.0. This is expected to be completed in June 2023 with a contract period of 21 years on the net electrical output.

RAM downgraded Cypark’s SRI sukuk

Last December, RAM Rating Services Bhd lowered the outlook on Cypark Ref Sdn Bhd’s RM550 million Sustainable and Responsible Investment (SRI) Sukuk Murabahah Programme (2019/2041) to negative from stable, while reaffirming the AA3 rating of the facility.

Cypark Ref, an indirect wholly-owned subsidiary of Cypark, is a funding conduit set up to raise financing for the development of LSS2 projects owned by three entities, namely Viva Solar Sdn Bhd, Cove Suria Sdn Bhd, and Cypark Estuary Solar Sdn Bhd.

Post-completion, Cypark Ref will receive deferred turnkey contract payments from these three project companies to service its sukuk obligations.

Viva Solar is undertaking the 49mw ground-mounted solar plant in Kedah, while Cove Suria and Cypark Estuary Solar are undertaking the 98mw DTU plants in Kelantan.

According to RAM Ratings, the negative outlook reflects the potential downside of extended delays in the construction of the two floating solar plants in DTU.

“Delays beyond our stressed assumption of June 30 (management’s base case: March31) may cause the transaction a further liquidity shortfall. We have reaffirmed the rating in view of the expected irrevocable and unconditional RM26 million liquidity bank guarantee — to be procured by transaction sponsor Cypark Resources for the benefit of Cypark Ref — that would replenish loss of cash flow from the delays under our sensitised case,” the credit ratings agency wrote on Dec 17 last year.

RAM Ratings, however, believes that the liquidity bank guarantee will provide much-needed support to help Cypark Ref tide over a potential default in June this year and restore the transaction’s liquidity buffers to a level commensurate with the AA3 rating.

In a filing with Bursa Malaysia last Friday, Cypark announced that RAM Ratings has again reaffirmed the long-term rating of AA3 for its SRI sukuk via its letter dated May 26.

“The AA3 rating indicates high safety for payment of financial obligations. The rating outlook is maintained at negative to reflect RAM Ratings’ concerns of extended construction delays for the two floating solar plants at DTU beyond its stressed timeline,” it notes. Cypark adds that RAM Ratings’ rating assessment has also considered the extraordinary resolution notice that was circulated to the sukuk holders on May 23.

“These changes, including modifications to the transaction terms and payment structure, are not averse to the issue rating. The reaffirmation of rating at AA3 is expected to provide confidence to sukukholders to support the proposed amendments in the extraordinary resolution favourably,” it stresses.

http://www.theedgemarkets.com/article/cyparks-debt-and-cash-flow-problems-spook-investors

Singapore Investment

-

-

-

-

SGX share price to rocket with Nasdaq?23 hours ago

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Cut exposure2 days ago

-

-

-

-

-

-

-

-

-

Gold Price Forecast 20274 days ago

-

Dividends May 20264 days ago

-

-

-

-

-

-

-

-

-

-

-

-

-

China Day 7 - 白沙古镇, 束河古镇 (丽江)1 week ago

-

-

-

May 2026 Updates1 week ago

-

-

-

-

-

Month of May 20262 weeks ago

-

-

-

Portfolio (May 30, 2026)2 weeks ago

-

Portfolio (May 30, 2026)2 weeks ago

-

-

-

Portfolio -- May 20262 weeks ago

-

May 2025: New Addition UIBREIT2 weeks ago

-

-

-

组屋达到MOP后,你能做什么?3 weeks ago

-

1M net worth at 283 weeks ago

-

-

Happy Mother’s day5 weeks ago

-

Is buying condo your goal?5 weeks ago

-

-

Pamper yourself after retirement5 weeks ago

-

Short games vs long games5 weeks ago

-

When the Market Humbles You.1 month ago

-

-

Quiet times1 month ago

-

-

-

Special Dividend Anyone?1 month ago

-

-

A Case for Mindful Consumption2 months ago

-

Some thoughts on my portfolio2 months ago

-

-

March 20262 months ago

-

-

Farewell careyourpresent.com3 months ago

-

-

A new year, a new workplace, a new start3 months ago

-

-

-

-

Weekly Flow show report, Feb 15 20263 months ago

-

-

The 2026 HDB “MOP Wave” & Upgrading Strategy4 months ago

-

Cory Diary : Family Expense Dec'255 months ago

-

-

Best Countries to Invest in 20265 months ago

-

-

FG Year in Review 20255 months ago

-

Restarting on Substack...5 months ago

-

DBS Home Loan5 months ago

-

-

-

Loopholes Singapore is on YOUTUBE!6 months ago

-

What Shall We Do About VERS?6 months ago

-

-

-

-

-

-

-

Been a while!10 months ago

-

-

-

Is Suntec REIT A Good Buy Now In 2025?10 months ago

-

-

-

-

-

-

FAQ on Quantitative Investing Part 21 year ago

-

-

-

-

-

Top 10 Highlights of 20241 year ago

-

-

-

STI ETF1 year ago

-

-

-

Unibet Casino Bonus Codes 20241 year ago

-

-

-

-

Monthly IBKR Update – June 20241 year ago

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Monthly Summary of November 20232 years ago

-

Migration of website2 years ago

-

-

-

-

-

Hello SP Group, I'm Back!2 years ago

-

-

-

A New Light3 years ago

-

-

-

-

2022 Thoughts, Hello 2023!3 years ago

-

Series of Defaults for Maple Finance3 years ago

-

Takeaways from “Sea Change”3 years ago

-

Greed is Coming Back3 years ago

-

-

-

-

-

-

-

-

What is Overemployment3 years ago

-

Terra Hill Condo (former Flynn Park)4 years ago

-

Alibaba VS Tencent: The Battle Royale4 years ago

-

-

-

-

-

-

-

-

-

-

-

-