THE glove sector has undoubtedly been in the limelight since the Covid-19 pandemic broke out. However, of late, there has been much discourse on the sector, with one party, comprising mainly retail investors, making bullish bets, and another, the institutional investors, having a less sanguine view.

This has been further fuelled by the GameStop frenzy in the US, where a “battle” broke out between a group of amateur investors on Reddit — who were buying shares of the video game retailer, leading to phenomenal gains in its share price — and a multibillion-dollar hedge fund, which was betting against the stock.

In a bid to emulate the GameStop saga and mounting a challenge to short-sellers, a new forum on Reddit dubbed “BursaBets” was created by Malaysian investors on Jan 28 to buy up shares in rubber glove companies, in particular Top Glove Corp Bhd. The forum even has its own Telegram group dedicated to discussing the stock.

However, many do not see this as a formidable threat for the Malaysian market, given the strong presence of institutional investors. As at last Wednesday, the daily trading participation of institutional investors, both foreign and local, was at 66.81%, while that of local retail investors was at 33.19%.

In fact, Top Glove’s shareholder mix, according to the latest available annual report for the financial year ended Aug 31, 2020, showed Malaysian and foreign institutions holding a 88.79% stake in the company, with local and foreign retailers holding the remaining 11.21%.

Nevertheless, it is worth noting that local retail participation in Top Glove has risen from 9% on Aug 31, 2019, to 11.13% on Aug 31, 2020.

“Top Glove is already heavily owned both by institutions and retailers, so it’s a totally different scenario from the GameStop saga where it was a case of new retailers jumping into the market, and therefore the end results won’t be the same,” says Peter Lim Tze Cheng, founder and chief research officer of Trident Analytics Sdn Bhd, an independent research firm.

When Bursa Malaysia lifted the suspension of regulated short-selling (RSS) on Jan 4, glove stocks were heavily shorted, especially Top Glove, during the first trading week of the year.

Short-selling aside, most analysts who had bullish target prices on glove stocks in 2H2020 have since trimmed the said target prices.

“What’s happening now is earnings expectations have increased, but surprisingly, target prices have been lowered. This is because some analysts had been caught up in the euphoria of the whole situation and were using one-year forward earnings expectations and trying to use the same price-earnings multiple of 20 to 25 times on supernormal earnings, which is the incorrect thing to do,” says Pankaj C Kumar, a former fund manager and head of research.

“Analysts have now turned pessimistic on the sector because they realised that they were overly bullish before, so they have started shifting the goalposts in terms of how they value the companies today.”

Pankaj says it is best to ignore the noises in an upcycle or downcycle of a sector when valuing a company. “Always value a company based on what is sustainable. If you know that 2021 is going to be ridiculously high in terms of earnings, and of course that would mean that the price-earnings ratios (PERs) are going to drop but will likely normalise in maybe 2022 or 2023, use a yardstick that is a bit more consistent, rather than shifting the goalposts.”

Trident’s Lim says there are three aspects that move share prices fundamentally — earnings growth, a rerating of the stock and follow-through interest from the market. “You need to have all three aspects together for share prices to move up fundamentally.

“The glove sector has already seen tremendous earnings growth and it has already experienced a rerating. The issue at hand now is the follow-through interest, as the market is now shifting away its interest from Covid-19 plays to other sectors such as tech.”

Glove stocks are not as popular now as they were last year but a few are still fundamentally attractive, says private investor and former investment banker Ian Yoong.

“The average selling price (ASP) of gloves is still high; the average order book is still high at 340 to 360 days (this refers to the number of days from order to delivery). The biggest fear of fund managers is that earnings will fall off a cliff in 4Q2021. The main reasons for this is the significant growth in planned glove production capacity and news of vaccines for Covid-19.

“Many listed companies jumped on the glove bandwagon in mid-2020. These were mainly announcements and news flow with generally little action. If indeed these prospective glove manufacturers are able to fulfil the planned production capacity, total glove production will most probably double from the current global capacity of 330 billion,” says Yoong.

To make matters worse, China’s glove manufacturers reportedly plan to ramp up production by 100 billion by 2023, he adds.

“The reality is that glove production capacity is unlikely to increase beyond 20% to 30% by the end of 2021. Glove stock prices have declined 20% to 50% since the peak in October 2020. There are opportunities for profit in selective glove companies. Focus on those glove manufacturers that are able to differentiate their products.

“Production bottlenecks have slowed down the vaccination process to 2Q to 3Q 2022. The use of rubber (nitrile) gloves in many industries has become the norm since the outbreak of Covid-19 and will remain so for the next few years,” says Yoong.

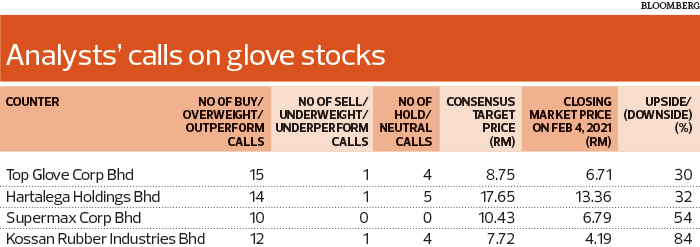

A Bloomberg poll of analysts shows that the majority still have “buy” calls on glove counters, while some are less enthusiastic, with “hold” and “underperform” calls.

Like in any debate, there are the affirmative and negative arguments. We take a brief look at both from the perspective of analysts.

The affirmative

Hong Leong Investment Bank Research, in a Jan 7 note, maintained its “overweight” call on the glove sector. Top Glove was its top pick with a target price of RM10.54, indicating an upside of 57% to its closing price of RM6.71 last Thursday.

“We remain upbeat on the sector’s 2021 outlook, as we see high demand and ASPs to persist. Although there may be a gradual dent in glove demand post-vaccine discovery, we do not see it being too damaging, considering past trends showed only mild tapering in growth. That said, the appreciation of the ringgit against the US dollar presents a slight negative impact,” the firm says.

In a Jan 26 note on Hartalega Holdings Bhd, PublicInvest Research reiterated its “outperform” call on the stock with a target price of RM24.50, an upside of 83% to its closing price of RM13.36 last Thursday.

“Despite the gradual rollout of viable Covid-19 vaccines, we believe that the demand for gloves is still robust, as Hartalega is expecting to further raise its ASP by another 40% to 50% in 4QFY2021. We opine that it is fairly unlikely to inoculate a sufficient percentage of the population to reach herd immunity, given the limited vaccine supplies. With that, we believe that the demand for rubber gloves should be able to sustain in the short to medium term,” the firm says.

Meanwhile, CGS-CIMB Research in a Jan 14 note retained its “add” call on Kossan Rubber Industries Bhd, but with a lower target price of RM7.64 from RM9.16 previously. This is an upside of 82% to Kossan’s closing price of RM4.19 last Thursday.

“We now peg Kossan to the glove sector’s five-year mean despite its robust earnings prospects as we think the stellar numbers we forecast for FY2021 to FY2023 may be unsustainable in the long run. Nevertheless, we continue to like Kossan for its strong earnings prospects (three-year earnings per share compound annual growth rate of 79.6%) as it stands to benefit from the favourable supply-dynamics in the glove sector owing to Covid-19,” the firm says.

As for Supermax Corp Bhd, MIDF Research in a Feb 3 note maintained its “buy” call on the stock with a target price of RM13.83 — more than double its closing price of RM6.79 last Thursday.

“We reiterate our ‘buy’ recommendation on Supermax as valuation is still very attractive at current levels. We notice that Supermax’s treasury shares increased to 212.3 million from 101.9 million in FY2020 and it is possible that the shares could be paid out as dividends.

“Topping that with Supermax’s improving operating cash flow and cashpile, we think that there is a possibility that the company may reward shareholders with a potential special dividend,” the firm says.

... and the negative

AmInvestment Bank in a Jan 13 report maintained its “neutral” view on the sector as valuations for glove companies under its coverage (Top Glove, Kossan and Hartalega) are already fully reflected in the companies’ earnings outlook.

“We reckon the ASPs will begin to ease after 1H2021 following the strong increase over the past nine months, and are already priced in. Moreover, we are cutting our target PER by 10% across the board to take into account the risk of a down cycle in the sector as a result of successful rollouts of Covid-19 vaccines.

“While we believe that glove makers’ fundamentals remain steady for the next few years, they offer limited upside at their current share prices. Hence, we advise investors to accumulate at lower levels,” the firm says.

JP Morgan has “underweight” ratings on the three glove stocks under its coverage, namely Top Glove (target price: RM3.50), Hartalega (RM8.50) and Kossan (RM3.80).

“No one is certain of the ASP beyond 1Q2021. But consensus and JP Morgan forecasts are in unison, projecting a year-on-year drop in 2022/2023 profits — the variance is only in the magnitude of decline.

“ASP is now at US$140 versus pre-Covid-19’s US$22. It is too simplistic to assume that the glove pricing mechanism will revert to pre-Covid-19’s cost-plus model, when sellers had altered it to a ‘take it or leave it’ basis during this pandemic,” the firm says.

JP Morgan adds that since there are no official data on global glove demand and supply, it is thus difficult to track stock levels.

“But one has to accept that the recent seven times ASP hike was driven by unsystematic buying. Our testing thesis might shed light on demand prospects because testing drives hospitalisation and thus glove demand.

“Developed nations, which had been testing aggressively, have now shifted to lockdown to handle Covid-19, which could reduce testing and, thus, glove demand. US testing has also decelerated,” the firm says.

The sum of all perceptions

There is no doubt that profits in the coming months for the glove sector will reach record highs, says Yoong. “Stock prices represent the sum of all perceptions. This is true for all financial instruments. It is likely that the share price performance of the glove sector is set to improve in the short term.

“Retail investors should be less concerned about the short-term share price performance of glove stocks and instead, focus on the business performance of the listed companies they have invested in, and industry developments,” he continues.

“It matters little if other investors or analysts agree or disagree with us. If the market mechanism is inefficient, leading to a mispricing of a certain asset, retail investors who have the luxury of time should, in Wall Street speak, ‘back up the truck’. This means buy as much as possible in layman’s terms.”

As to which side will be proven right further down the road, only time will tell, and the getting it right — which few can do all the time or most of the time — is what gives investors, punters and analysts the satisfaction in forecasting and investing.

RSS focus shifted to Supermax last week

By Supriya Surendran and Lee Weng Khuen

Regulated short-selling (RSS) on Top Glove Corp Bhd eased last week, following calls — inspired by the GameStop mania in the US — for retail investors to buy more local glove shares to fight against institutional funds.

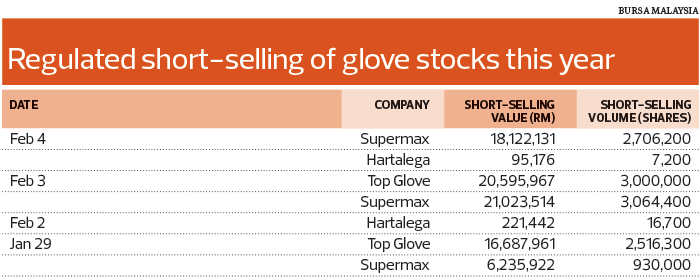

Instead, the short-selling limelight shifted to Supermax Corp Bhd, which saw 5.77 million shares worth RM39.75 million shorted for the week to Feb 4.

For the week ended Jan 29, only 1.39 million Supermax shares valued at RM9.29 million were shorted.

To recap, on Jan 29 — a day after the BursaBets forum was created on Reddit, shares in glove companies gapped up while Top Glove recorded an RSS volume of 2.52 million shares worth RM16.69 million.

The local bourse was closed last Monday as it was Federal Territory Day. The short-selling activity was tepid for glove stocks last Tuesday, except for Hartalega Holdings Bhd, which saw 16,700 shares worth RM221,442 being shorted.

However, by Wednesday, the two-day settlement cycle, or T+2, began to weigh on the glove stocks’ rally and reignited massive short-selling activity.

Some three million Top Glove shares worth RM20.6 million were shorted that day.

Supermax saw heightened short-selling pressure, with 3.06 million shares valued at RM21.02 million being shorted.

On Wednesday alone, Top Glove and Supermax collectively accounted for 39.9% and 71.2% of total short-selling volume and value respectively on Bursa Malaysia.

Top Glove was again not the main target of short-sellers, as 2.71 million Supermax shares worth RM18.72 million were shorted last Thursday. There was no RSS on Top Glove on Thursday.

Overall, for the week to Feb 4, investors shorted three million Top Glove shares valued at RM20.6 million. This compares with 17.24 million shares worth RM110.23 million shorted for the week ended Jan 29.

Also, it is far less than the short-selling volume in the first week this year, after the RSS ban was lifted. A total of 196.19 million shares worth RM1.09 billion were shorted that week.

The net short position of Top Glove rose to 2.98% last Thursday from 2.95% a week ago, while Supermax was lower at 0.76%.

Private investor and former investment banker Ian Yoong says the impact of RSS on share prices is marginal as the cap is 4% on aggregated net short positions.

“Any number below 10% is considered insignificant, and the uplifting of the suspension of RSS inconsequential. The uplifting did, however, dent investor confidence.”

He stresses that RSS and the conspiracy theory about investment banks and stockbroking firms colluding were wrongly blamed for the plunge in glove stock prices.

“During the euphoria of glove stocks in July to November last year, the vast majority of investors were overzealous in their buying. They were nudged on by proprietary dealers who earned millions in short-term trading. They were encouraged by influencers on social media and exuberant research analysts.

This was a potent explosive mix that led to the irrational exuberance that peaked in October last year,” he explains.

http://www.theedgemarkets.com/article/great-gloves-discourse