Tiger Synergy Berhad ("TIGER") was formerly known as Minply Holdings (M) Berhad. It was incorporated on December 1994. It is an investment holdings company where the company's core businesses are in the property development and construction industry.

Moving forward, TIGER will envisage higher revenue contribution for the property development segment. TIGER under its subsidiaries is led by an experienced, capable and dynamic management team. Some of the directors and senior management of the Company have more than 15 years of hands on experience in Property Development, Construction Industry as well as Manufacturing and Trading Industry.

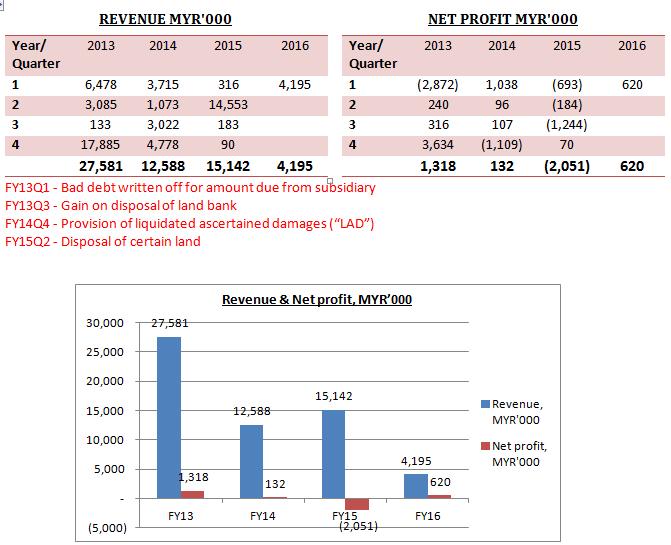

Financial Highlights

TIGER financial performance over the past 3 years was bad.

Basically, it had almost no revenue contributed in FY15! Its revenue in FY15 is mainly contributed from disposal of certain land in 2nd quarter, which it did not disclose the amount.

Other than that, there is no on-going projects too while pending for the launch of new projects.

Besides, the high administration costs and professional fees of comprising mainly expenses incurred for the Private Placement 2015, auditors’ remuneration, legal and secretary fees, are also a main factor for the net loss in FY15.

In short, TIGER had difficulty to generate revenue since FY15.

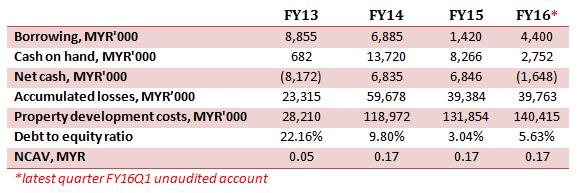

Financial Strength

As a penny stock, TIGER financial strength is surprisingly to be average, with borrowing of only MYR4.4m. Its debt to equity ratio is only 5.63% in the latest quarter, which is very low! FYI, TIGER debt to equity ratio had been reduced from year to year. One of the reasons is because of fund raising by private placement, which leads to an increase in shares capital and reduce in liabilities.

Besides that, TIGER is able to maintain its NCAV at the level of MYR0.17 per share.

Most of its current asset is come from property development costs, with MYR140.42m in FY16. This figure is potentially to be converting into revenue one day!

Having said so, TIGER accumulated losses is currently up to MYR39.76m! In other words, its company business is not profitable.

Company 2015 Highlights

Project Overview

Project Briefing

TIGER will launch three new projects with a combined gross development value (“GDV”) of MYR500m in year 2016.

With the three new projects, TIGER aims to generate a gross profit of MYR100m in FY16 from a net loss of MYR2.05 million in FY15.

TIGER will kick off its Alam Impian project in Shah Alam, Selangor, which has a GDV of MYR300m. The project features 132 semi-detached houses. Currently, it had started earthworks on the site, and target to launch the project by early 2016.

Apart from Alam Impian, TIGER will also be launching two condominium projects located in Gombak and Cheras, with a GDV of MYR100 million each. It is targeting to launch the two projects by the second quarter of 2016.

It estimated that with about 40% of development costs, the three projects will garner a gross margin of some MYR300 million over the three years of construction period.

That is where TIGER FY16 target of MYR100m gross profit comes from, provided that it manages to sell all the units to be launched.

Nevertheless, TIGER’s managing director, Ms. Shirley Tan noted that even in the case of TIGER not being able to achieve 100% sales within FY16, it is still sufficient to finance the development by selling 40% of the three projects. Once it achieves 40% of sales, TIGER would have enough funds to complete the entire projects.

Besides, TIGER has another two property projects in Serdang and Seri Kembangan, which are relatively larger. It will launch these two projects maybe by 2017, because they are quite huge with a collective GDV of MYR1b.

Therefore, all five projects have a combined GDV of MYR1.5b, which is estimated to provide the group a gross profit of MYR500 million over the next five years.

FYI, Ms. Shirly Tan was appointed to her current position on Nov 2014, succeeding her brother Datuk Tan Wei Lian who has been redesignated as executive chairman.

*NOTE: The GDV given by TIGER’s managing director, Shirley Tan, is different with the GDV extracted from TIGER annual report 2015. Both of the info are published on Nov 2015.

Batching Plant

Besides property development, TIGER recently had set up a MYR2m new concrete batching plant in Alam Impian, Shah Alam. The business is meant to complement its property development division.

The plant is mobile in nature and can be dismantled and relocated to another location. The opening of this plant marks a new chapter in TSB’s growth in the concrete business segments through many projects in the Klang Valley region.

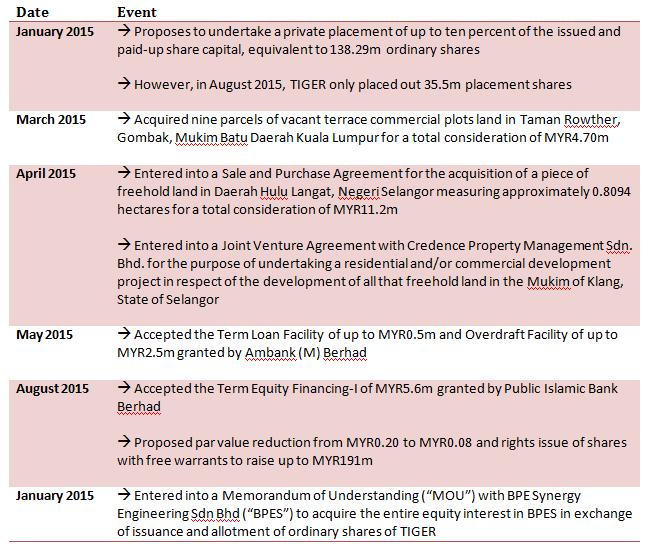

Corporate Exercise

Meanwhile, TIGER has proposed to undertake a rights issue on the basis of two rights shares for one existing share, to raise up to MYR191.47m.

Under the proposal, the rights issue also comes with two free warrants and one bonus share for every five subscribed rights shares. The warrants and bonus shares are intended to be a “sweentener” and an incentive to make the proposed corporate exercise more attractive.

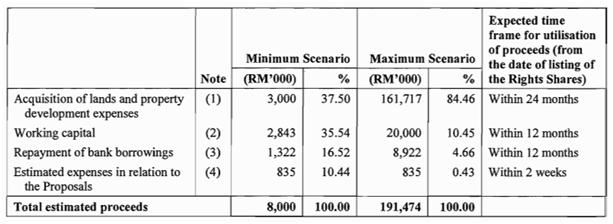

The usage of proceeds from rights issue are as below:

TIGER plans to use 84.46% of the proceeds to acquire land and for property development expenses. It has the intention to acquire additional land bank in the Klang Valley going forward. It is because the management foresee that in the near future of one or two years, there will be good land with attractive prices due to the economic slowdown now.

Of the remaining proceeds, 10.45% is slated for working capital, 4.66% to repay borrowings, and 0.43% for estimated expenses in relation to the rights issue. Subsequent to the repayment of bank borrowings, TIGER will have zero gearing.

In addition, TIGER has resolved to fix the following:

(i) the issue price of Rights Shares at MYR0.08 each; and

(ii) the exercise price of Warrants at MYR0.08 each.

Notably the proposed corporate exercises also includes a par value reduction of Tiger Synergy share to 8 cent, from 20 cent. With the par value reduction, TIGER will be able to eliminate its existing accumulated losses.

Based on the cancellation of MYR0.12 of the existing par value of the enlarged issued and paid-up share capital assuming full exercise of the outstanding TIGER-WB, Warrants 2013/2018, the proposed par value reduction will give rise up to a total credit of MYR143.61m.

TIGER intends to utilise to eliminate its accumlated losses and the balance arising thereafter will be credited to its retained earnings.

FYI, as at 30 September 2015, TIGER has available cash on hand of MYR2.75m with borrowing of MYR4.40m. TIGER’s balance sheet also shows that its accumulated losses stood at MYR38.76m.

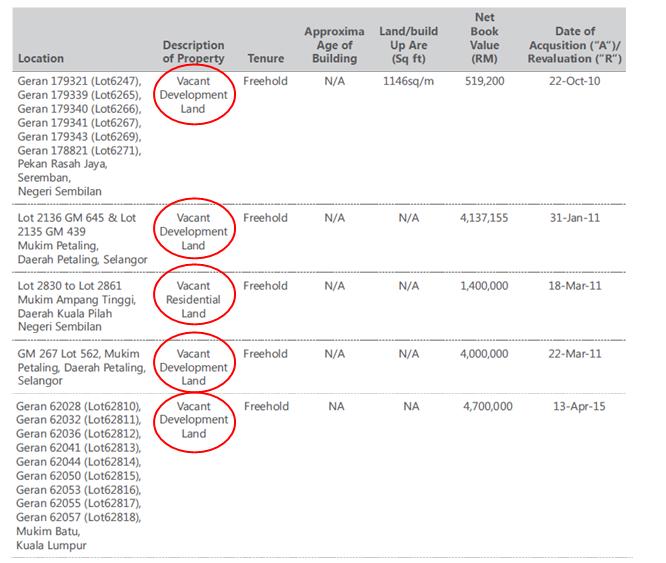

Land Bank

As to date, TIGER had 5 piece of vacant lands to be developed in future, where 2 piece at Seremban, 2 piece at Petaling Selangor and 1 piece at Kuala Lumpur. The piece of land at KL is for Gombak project. The total net book value of this lands are up to MYR14.76m.

MOU- Venture into Semiconductor Industry

On Jan 2016, TIGER had entered into a Memorandum of Understanding (“MOU”) with BPE Synergy Engineering Sdn Bhd (“BPES”) to acquire the entire equity interest in BPES in exchange of issuance and allotment of 200m ordinary shares of TIGER of MYR0.08 each upon completion of proposed capital reduction for MYR16m.

In other words, TIGER plans to use 200m of its ordinary shares which worth MYR16m to exchange for BPES 100% equity interest.

In the MOU, it mentioned that BPES shall provide a profit guarantee of at least MYR2m per financial year for 3 years continuously upon the completion of the Share Swap.

BPES specializes in printed circuit board and mechanical design, fabrication, assembly and board repairing services for the semiconductor industry and provides full service turn-key solutions for engineering applications, operations and project management.

Both parties agree to enter into an agreement within 6 months from the date of this MOU or such other extended period as may be agreed by both parties.

Based on this MOU, BPES have a PE of 8x based on profit guarantee of MYR2m and share swap consideration of MYR16m.

This business diversification will enable TIGER to leverage on the growth of the semiconductor industry in Malaysia, which has benefited from the global demand in the usage of mobile devices, optoelectronics and embedded technology.

Going forward, TIGER intends to offer value-added properties with smart technology by capitalizing on the competency and experience of BPES.

FYI, BPES has successfully developed Smart Factory solutions to customer. It had a team of engineers who are very familiar with IoT gateway. For example relay counter, temperature detection automation unit, air pressure monitoring & controller and handler environmental monitoring. It can provide value added property to purchasers by integrating TIGER property projects with Smart Home Solutions.

Conclusion

Currently, TIGER had 3 on-going property projects which will be launched by this year. This 3 projects will be the main contribution for TIGER in 2016. The estimated gross profit for this 3 projects are MYR93m over the next 3 years, with averagely MYR31m per year. Besides, TIGER is going to launch another two big projects in year 2017 too.

TIGER had a new concrete batching plant which will lower down its property development cost. I believe this will boast up its profit margin more or less.

In addition with its par value reduction and rights issue to clear off its accumulated losses and bank borrowings, TIGER had seems to be very keen in turning its fundamental.

Other than that, TIGER had also entered into MOU and look forward to acquire a semiconductor company which will provide guarantee return of MYR2m for three years continuously. It is trying to seek for other income rather than just property.

It also had NTA of MYR0.22 per share and NCAV of MYR0.17 per share. In other words, with its current share price of MYR0.09, TIGER is currently traded approximately 50% below its NTA and NCAV. In term of assets, TIGER had seems to be undervalue and it is because of its not profitable business.

However, do take note that, after right issues, TIGER will have approximately 3b shares! Its earnings will be diluted quite heavily. Even though TIGER does not have a strong proven track record, we are able to foresee its future earnings ability. Once the share swaps complete, its semiconductor business is expected to contribute steady recurring income. The income from property development is expected to increase gradually too.

Hey guys, I am writing stock analysis report to earn some pocket money. For more information, you may email me at richeho_92@hotmail.com

I will send you one or two samples of my report, for your reference.

Happy 2016 new year! Hopefully all of you will do well in investment this year :)

Cheers!

TIGER (7079) - (RICHE HO) Tiger Synergy Berhad - A Transforming Tiger

http://klse.i3investor.com/blogs/rhinvest/89272.jsp