Inta Bina Company Structure

Inta Bina Group is a building contractor with more than 25 years of operating history in the construction industry in Malaysia. It has completed more than 110 building construction projects with a total contract value of more than RM2 Billion.

Let sees Inta company structure as below:

With only one subsidiary, there is no risk of unexpected impairment and operation loss from other subsidiary.

http://klse.i3investor.com/blogs/lionind/145070.jsp

Tender Book and Estimated Orderbook (by 30 Dec 2017)

According to theedge’s report, Inta tender book stood at a record high of RM2.91 billion as at Oct 30 2017, out of which RM1.72 billion is pending, RM274 million has been secured and the remaining RM915.4 million was unsuccessful. (http://www.theedgemarkets.com/article/inta-bina-aggressive-bidding-mode)

Based on theedge report on 30 Oct and Inta Q3 report (increasing orderbook as compared to Q2), the estimated tender book figure as per 30 Dec 2017 is possible to reach RM3.2 billion. To estimate the total contracts secured in 2017, let us have the following assumption of success rate as per table below:

Let be conservative on the estimated success rate of the tendered projects. If we assume 12% success rate, there should be RM384 mil of contracts secured in 2017 (including first half of 2018).

With existing orderbook of 634 mil as per 30 Sept 2017 (Q3’17 report), I

expect the total order book as per 30 Dec 2017 may likely to exceed RM700 mil (on the expectation of more contract awarded in 2H2017 from its clients)

Q4’17 and FY2018 Profit Forecast

One of the future profit estimation methods for construction counter is based on their total orderbook. Due to Inta being a pure construction company without other non-core business subsidiary, we can estimate its profit more accurately from the orderbook and past quarter result profit margin.

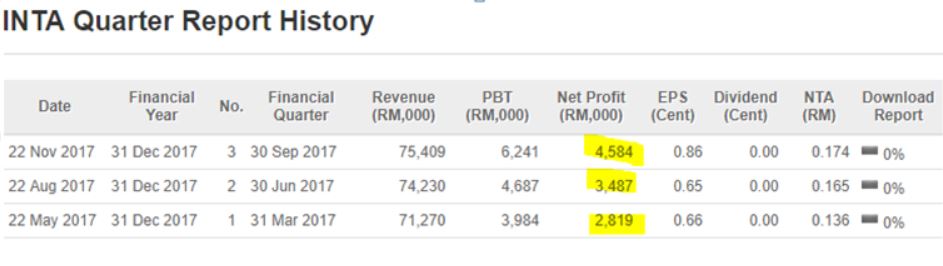

Before we start the profit estimation, let us have a look on the profit margin of past results as per figure and table below:

Source: Inta Q3’17 report

The net profit margin (after tax) in Q3’17 is 6.1% with the revenue of RM75.4 mil. I expect or estimate Inta net profit margin in Q4 maybe slightly improves due to cost saving and resource optimization (as they are dedicated builder and have over 25 years of experience).

Assuming RM700 mil orderbook could be completed in about 2 years’ timeframe with a net profit margin of 6.4%,

For coming Q4 result the forecast net profit is RM5.34 mil --> EPS of 1.05 cent.

The estimated EPS of 1.05 cent is an improvement of 22% QoQ (quarter over quarter). There are no YoY (year over year) data for comparison as it is just listed in May 2017.

Let us have a look on Inta forward 12 months fair value as table below (with 3 different PE) based on the estimated EPS of 4.18 cents (due to current industry average PE for small cap construction counters is about 14)

For PE and orderbook comparison with its peers of similar capital size

construction counter, please refer to Inta part 1 article at the link https://klse.i3investor.com/blogs/lionind/137704.jsp

Based on current price of 36.5 cents with a possible 1.05 cent EPS in the coming quarter result (to be released in Feb), Inta possible forward 12-month PE (annualize EPS 4.18 sen) could be improved to below 10x. Most of the small and medium capital average construction counters PE is about 14x which implies that possible target price for Inta is in the range of 54 cents (PE 13x) and 63 cents (PE 15x). Even with PE11x, there is still about 25% of upside (46 sen) from current Inta price.

Main Catalysts for future profit growth:

1. Most of their clients are well-known and established developers (Gamuda Bhd, Eco World Bhd, Mitraland Group Sdn Bhd, Mah Sing Berhad etc).

2. Actively tendering new jobs which their current tender book possible to reach RM3.2 billion and their orderbook is expected to increase to RM700 mil by Dec 2017 (unbilled orderbook RM635 mil as per Sept 2017 report).

3. I expect Inta may have higher revenue in 2018 as compared to 2017 from their increasing orderbook (refer to Q3’17 report).

4. Inta already qualified to transfer to Main Board as Inta already fulfilled Main Board profit requirement (past 3 years total net profit more than RM20 mil). The benefit of transfer to main board is they can attract more funds.

5. Inta has been actively tendering for projects in the Klang Valley from private housing developers under the federal and state affordable housing initiatives such as Rumah Mampu Milik Wilayah Persekutuan and Rumah Selangorku (affordable housing project) which are still in demand.

Risk

1. Property development projects slow down. I believe Inta still can secure sufficient projects in 2018 based on their past 25 years track records. Inta is a dedicated builder which delivers higher quality of works which is an advantage especially for those established developers (Eco World, Gamuda, Mitraland)

2. Foreign workers shortage is a norm in the market(partly can be mitigated by using IBS)

3. High steel (rebar) price (The estimated rebar cost for a standard residential project is about 6-8%). However, cements, brick and ceramic tiles costs have been dropping for past 1 year which can compensate the rising cost of rebar.

Summary

1. The experience, dedication, quality of works of Inta makes them still doing well in 2015-2017 even in the property market slow down time. This can be proven from their past 3 years profit growth.

2. Normally Ace market counters have higher PE especially those growing companies. Most of the small and medium capital average construction (Eg, bpuri, Ireka, HSSE) counters PE is about 14x. With forward 12-month EPS of 3.99 sen, the possible target price for Inta is in the range of 54 cents (PE 13x) and 63 cents (PE 15x).. Even with PE11x, there is still about 25% of upside (46 sen) from current Inta price.

3. Inta past 3 years profit already qualified to transfer to Main Board as Inta already fulfilled Main Board profit requirement (past 3 years total net profit more than RM20 mil).

If you interested on my analysis report, please contact me at davidlimtsi3@gmail.com

Inta Bina Group is a building contractor with more than 25 years of operating history in the construction industry in Malaysia. It has completed more than 110 building construction projects with a total contract value of more than RM2 Billion.

Let sees Inta company structure as below:

Inta Bina Group Berhand (IBGS) has only 1 subsidiary, which is Inta Bina Sdn Bhd (IBSB). Inta secures and carries out construction contracts through IBSB.

This 1 subsidiary structure shows a very clean structure where all the G7 license, contracts, tenderings, debt and cash flow are under one company. In other words, they are very focused builder that their main or core activities are carrying out construction contracts.With only one subsidiary, there is no risk of unexpected impairment and operation loss from other subsidiary.

http://klse.i3investor.com/blogs/lionind/145070.jsp

Tender Book and Estimated Orderbook (by 30 Dec 2017)

According to theedge’s report, Inta tender book stood at a record high of RM2.91 billion as at Oct 30 2017, out of which RM1.72 billion is pending, RM274 million has been secured and the remaining RM915.4 million was unsuccessful. (http://www.theedgemarkets.com/article/inta-bina-aggressive-bidding-mode)

Based on theedge report on 30 Oct and Inta Q3 report (increasing orderbook as compared to Q2), the estimated tender book figure as per 30 Dec 2017 is possible to reach RM3.2 billion. To estimate the total contracts secured in 2017, let us have the following assumption of success rate as per table below:

|

Dec 2017 Estimated Tender book |

3200M (3.2 billion) |

3200M (3.2 billion) |

|

Estimated Success rate

|

12%

|

15%

|

|

Estimated Contracts secured (mil)

|

384

|

480

|

Q4’17 and FY2018 Profit Forecast

One of the future profit estimation methods for construction counter is based on their total orderbook. Due to Inta being a pure construction company without other non-core business subsidiary, we can estimate its profit more accurately from the orderbook and past quarter result profit margin.

Before we start the profit estimation, let us have a look on the profit margin of past results as per figure and table below:

|

Inta’s NET profit margin (%) |

|

|

Q1’17 |

3.96 |

|

Q2’17 (affected by listing expenses and Hari Raya) |

4.7 |

|

Q3’17 (July-Sept) - |

6.1 (4.58 mil) |

|

Q4’17 (Oct-Dec) - Estimation |

6.4 (expect slightly improve due resource optimization) |

The net profit margin (after tax) in Q3’17 is 6.1% with the revenue of RM75.4 mil. I expect or estimate Inta net profit margin in Q4 maybe slightly improves due to cost saving and resource optimization (as they are dedicated builder and have over 25 years of experience).

Assuming RM700 mil orderbook could be completed in about 2 years’ timeframe with a net profit margin of 6.4%,

1) Estimated Net profit per year, NP = 700 mil / 2 years X 0.064 = RM22.4 mil

2) NP in a quarter = 22.4 mil / 4 = RM5.6 mil.

For the following next 12 month forward 12-months, the estimate net profit forecast is RM22.40 mil --> EPS of 4.185 cents.For coming Q4 result the forecast net profit is RM5.34 mil --> EPS of 1.05 cent.

The estimated EPS of 1.05 cent is an improvement of 22% QoQ (quarter over quarter). There are no YoY (year over year) data for comparison as it is just listed in May 2017.

Let us have a look on Inta forward 12 months fair value as table below (with 3 different PE) based on the estimated EPS of 4.18 cents (due to current industry average PE for small cap construction counters is about 14)

|

Inta’s fair value based on EPS of 4.18 sen |

|

|

PE15

|

63.0

|

|

PE13

|

54.5

|

|

PE11

|

46.0

|

Based on current price of 36.5 cents with a possible 1.05 cent EPS in the coming quarter result (to be released in Feb), Inta possible forward 12-month PE (annualize EPS 4.18 sen) could be improved to below 10x. Most of the small and medium capital average construction counters PE is about 14x which implies that possible target price for Inta is in the range of 54 cents (PE 13x) and 63 cents (PE 15x). Even with PE11x, there is still about 25% of upside (46 sen) from current Inta price.

Main Catalysts for future profit growth:

1. Most of their clients are well-known and established developers (Gamuda Bhd, Eco World Bhd, Mitraland Group Sdn Bhd, Mah Sing Berhad etc).

2. Actively tendering new jobs which their current tender book possible to reach RM3.2 billion and their orderbook is expected to increase to RM700 mil by Dec 2017 (unbilled orderbook RM635 mil as per Sept 2017 report).

3. I expect Inta may have higher revenue in 2018 as compared to 2017 from their increasing orderbook (refer to Q3’17 report).

4. Inta already qualified to transfer to Main Board as Inta already fulfilled Main Board profit requirement (past 3 years total net profit more than RM20 mil). The benefit of transfer to main board is they can attract more funds.

5. Inta has been actively tendering for projects in the Klang Valley from private housing developers under the federal and state affordable housing initiatives such as Rumah Mampu Milik Wilayah Persekutuan and Rumah Selangorku (affordable housing project) which are still in demand.

Risk

1. Property development projects slow down. I believe Inta still can secure sufficient projects in 2018 based on their past 25 years track records. Inta is a dedicated builder which delivers higher quality of works which is an advantage especially for those established developers (Eco World, Gamuda, Mitraland)

2. Foreign workers shortage is a norm in the market(partly can be mitigated by using IBS)

3. High steel (rebar) price (The estimated rebar cost for a standard residential project is about 6-8%). However, cements, brick and ceramic tiles costs have been dropping for past 1 year which can compensate the rising cost of rebar.

1. The experience, dedication, quality of works of Inta makes them still doing well in 2015-2017 even in the property market slow down time. This can be proven from their past 3 years profit growth.

2. Normally Ace market counters have higher PE especially those growing companies. Most of the small and medium capital average construction (Eg, bpuri, Ireka, HSSE) counters PE is about 14x. With forward 12-month EPS of 3.99 sen, the possible target price for Inta is in the range of 54 cents (PE 13x) and 63 cents (PE 15x).. Even with PE11x, there is still about 25% of upside (46 sen) from current Inta price.

3. Inta past 3 years profit already qualified to transfer to Main Board as Inta already fulfilled Main Board profit requirement (past 3 years total net profit more than RM20 mil).

If you interested on my analysis report, please contact me at davidlimtsi3@gmail.com

You can get my latest update on share analysis at Telegram Channel ==> https://t.me/davidshare

Disclaimer:

This writing is based on my own assumptions and estimations. It is

strictly for sharing purpose, not a buy or sell call of the company.