[ UMWOG / VELESTO Energy ] 会随着国际油价的走势吗 ???

大家听到 UMWOG / VELESTO ( 新名 ) 就知道是家算是中游的油气公司. 它的主要业务就是提供钻油台给予上游公司, 也有一小部分是进行维修和检查机器服务 . 公司的业务主要是在大马进行, 多数的合约都是由 PETRONAS 所提供, 公司拥有 7 个普通钻井台 ( Jack- up drilling rigs ) 和 5 个自升式钻井平台 ( Hydraulic Workover Units ) , 在第三个季度将会迎来两个新的.

相信大家听到大马的油气公司就知道它们都出名 Write-offs/Assets impairment, 这家也不例外, 在前两年的业绩报告中, 几乎都有出现这种情况 , 在去年 2017年, 公司总共 write off 了 RM 982 mil .

此外, 公司在最新的报告中拥有 RM 13亿 ( RM 1.3 bil ) 的债务, 手上的现金也不多, 只有 RM 350mil. 公司现在的境况就只有把所有的业务盈利贡献都丢在还利息和债务, 让管理层添了不少压力, 市场也就因为这样所以不选择它. 但, 如果公司能在未来几年继续获得大型合约, 也能顺顺利利的完成所有活动, 是否会是个转折点呢 ?

我们先来看公司的基本面 :

P/E : -2.29

ROE : -38.55 %

DY : -

NTA : 0.323

Cash : RM 350 mil

E/Y : -

Debt to Equity : 0.520

EV/ EBIT : -3.29

Price to Book : 0.88

Dividend Policy : -

4 Quarters Total Cash Flow : RM -150++ mil

在几个月前换了名的 Velesto Energy 成功在Q1 18 的业绩中出现盈利, 但深入去看事情并不如此, 当中有了 RM 22 mil 的 Other Operating Income , RM 18 mil 的 Forex Gain , 因此看上去赚到的只能刚刚好补在债务和成本里.

很明显至今的基本面完全是不能看的, 我们能看的就只有它的未来. 管理层是有在报告中指出今年的钻井使用率会是 75% , 至 Q1 17 使用率已经高达 65% , 相信是因为国际油价的上涨. 只要国际油价能继续维持在 USD 70 - 80 这个位置, 公司基本上是会持续有合约.

在近期, 公司也成功获得了ROC Oil (Sarawak) 的钻井合约 NAGA 4,总共价值 RM31 mil , 会在 8 月开始进行, 为期 3 个月 .

由于股票大多数都又本地基金持有,因此个人认为合约方面会有一定的担保, 这是让它加分的一方面, 除非未来油价暴跌.

公司有超过 65% 的本地基金在里面 , 再加上换了名字, 管理层也出来喊话说在未来几个季度会慢慢恢复合理的盈利, 也注明这支股适合中长期投资者. 因此, 个人认为这几股短期来说是中长期投资者的挑战, 也有可能是个好机会. 股价在近几个月都属于炒股型, 都只是短期炒作.

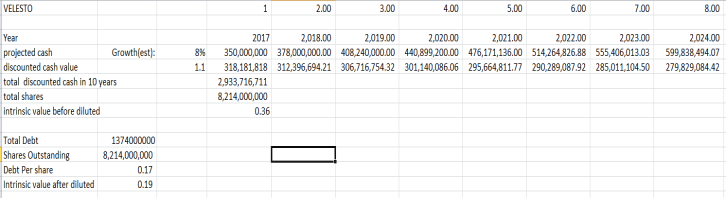

Interinsic Value :

Intrinsic value by using cash valuation method : 0.19 ( all debt factored in)

At the recent trading day (Friday 13/7/18 ) , Velesto(5243) is trading at RM 0.285 closing price which is 33.3% higher than the intrinsic value .

Current cash projection is based on the estimated growth rate of 8 % , the value will be remaining intact if VELESTO’s revenue is in line with expectation .

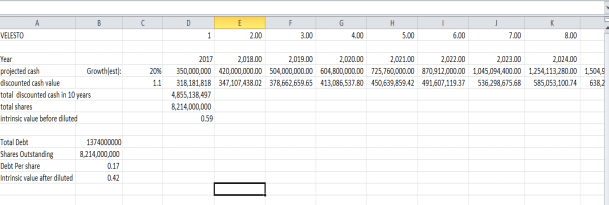

From the perspective of it’s intrinsic value , it is yet still not a value buy . However , the oil and gas industry is highly correlated with the crude oil price . There is unforeseen risk on this industry . However , the global oil price remain a hyperbullish despite near term negative sentiment . With the current oil price stand stably higher than 70 , this company is expected to turnaround from loss to profit . To be optimistic , if the oil price rally over 3 months period to hit 80-90 USD per barrel , we will higher our estimated growth % to 20 percent .

The optimistic expected result is such as following :

Intrinsic Value : 0.42 ( 47 % higher than its current closing price )

Chart Analysis :

Circle region : It indicates a vanish in selling pressure , turn to become a new accumulation period , long term investor can start to buy it in this rectangle formation , however , it requires a 3-6 month holding period . The best buying period will be at the breaching of the rectangle formation , with an expected return of more than 100 % .

All the volume indicator does not shows ant clear signal and picture of buy and sell .

GPMMA starts to converge .

Buying Region/ Accumulation Area : within the support and resistance area ( 0.26-0.325)

Best Buy : high volume breakout on 0.325

PEG ratio is not applied as the company is still not generating profit , further assumption is not necessary to prevent it from becoming a self fulfilling prophecy.

Disclaimer : Information above is for sharing and education purposes , not a buy and sell advice , please refer to ur advisory for any buy or sell call , buy and sell at your own risk .

Feel free to visit our FB Page , give us some likes and share it out so that we share more things to you !!!

http://www.facebook.com/J4-Investment-Capital-398139627315097/