A little background introduction:

RGB is a one stop gaming solutions provider for clients in the gaming industry. Based in Malaysia with more than 30 years of experience in gaming industry, they have set their footprint across most of SEA countries in Macau, the Philippines, Singapore, Vietnam and Cambodia. They mainly operate in 2 segments: SSM (Sales & Marketing), which involved in manufacturing and trading of various gaming products, & TSM (Technical, Support & Management), which provides leasing of gaming machines to casinos & slot club operators on a revenue share basis. I’m not going to go through in details here, as few bloggers and article have already covered about this stock previously, you can google it up if you wish to know more.

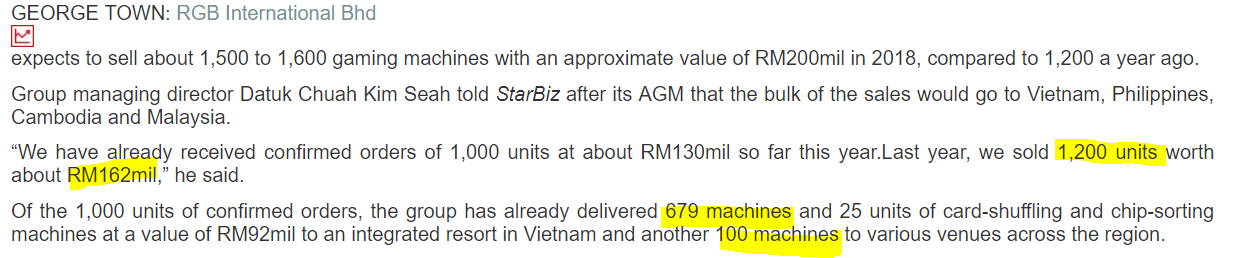

On 30th May 2018, Starbiz release an interview with RGB on their coming prospect. Here’s what the Group MD, Datuk Chuah Kim Seah said:

Basically information that we can derive from the above statement:

1) Sales of one machine = RM162m/1200 units = RM135k

2) For first half they had delivered 779 units of machines, total revenue = 779 x RM135k = RM105m

So for 1H18, total sales for their sales & marketing segment is RM105m, If we use this figure to deduct Q1 Sales & Marketing revenue RM15.17m, we will be able to get their Q2 estimated revenue from S&M, which is RM105m-RM15.17m = RM90m. in 2017, their profit margin from this segment is 14%. RM90m X14% = RM12.6m.

How About TSM (Technical support & management) division?

Currently, TSM segment operates in 38 concession venues across Asia with a total of 6,207 machines as at end of 2017. From last year, they have secured another 1,500 machines to supply to various customers and operate under concession business, which will start to contribute to their bottomline in this year. That’s a 24% increase in number of machines compare to the year before. And it doesn’t just stop there. In the recent interview with starbiz, Datuk Chuah indicated that RGB has also locked in another 850 gaming machines for its concession and leasing business this year, and will contribute another RM30-35m in turnover in 2019.

Looks like pretty promising, Isn’t it?

But in order to not to get too excited, let’s assume everything remain the same for now, at least for next quarter.TSM division revenue in Q118 was RM32m. Let’s assume both revenue & profit remain the same, Profit will be RM9.75m.

Total aggregate profit =RM12.6m+RM9.75m = RM22.35m. Minus off unallocated expenses RM3.4m (Plug from Q1), operating profit will be RM18.95m. Assume finance cost of RM230k & tax expenses of RM4.5m, Net profit = RM14.22m or EPS 10.5sen. Well sometimes things are too good to be good, so Let’s apply margin of safety and -20%, it will still equal to RM11.38m, EPS 8.4sen.

If this performance can be sustained for the rest of quarters, their EPS will came out to be 3 sen. Let’s apply a 12x PE and target price = RM0.36.

Datuk Chuah is being quite bullish and super confident on his company as well, he had mentioned few times in interviews and also financial report that RGB Is going to perform better than 2017.

He even told Zi Hui in an interview that the growth rate in 2018 will surpass than that of 2017. 2017 vs 2016, growth rate = 21.8%, If FY2018 able to grow 25%, the net profit will be RM38m, minus off RM6.4m in Q1, they will need to deliver RM31.6m for the balance 3 quarters, that’s an average of RM10.3m net profit per quarter. RM38m also equals to EPS of 2.8sen. Not too far from my estimation earlier.

Other Plus points:

- Past financial track record – net profit growing 5 years consecutively. CAGR of 35.47%.

- Strong BalanceSheet, Net Cash per share 7.51sen

- Expanding their business to fresh markets such as Nepal and South America. Huge potential as there are lots of machines with more than 10 years old and need to be replaced

- According to Technavio’s Global Casino Gaming Equipment Market 2017-2021 report, the global casino gaming equipment market is expected to grow at a compounded annual growth rate of 15.25% over the next four years.

Uptrend but not too aggressive, finding support on the trend line. It’s my biggest investment in my portfolio which took up 50% of my capital and I’m still looking to add position.

Disclaimer: This is not a buy call. Sharing is Caring :)

http://klse.i3investor.com/blogs/hanliang88/171154.jsp