Jaks Resources – What happened in the last 5 Years ?

Jaks’ 5 years chart with notable events

- Signed JV agreement with CPECC as partner to JHDP

- Secured financial close on Loan for JHDP

- Officiated power plant construction

- Entry of Mr. Koon Yew Yin

- 10% private placement at RM1.36

- RM50m Bank guarantee claims by The Star on Pacific Star

- 10% private placement at RM1.38

- Announcement of 1 for 2 Warrant right issue at RM0.25

- Mr. Koon Yew Yin faced initial margin call

- Mr. Koon Yew Yin sold entire holdings under margin calls

- Warrant right issue completed with only 37% subscription

- RM50m Bank guarantee paid to The Star

- Awarded 38m free shares to executives under RSP of LTIP

- 10% private placement at RM0.70

- Lockdown MCO due to Covid19

- Announcement of 2 right shares at RM0.40 with 1 free warrant for every 4 shares held

Discussions

Uptrend A started when Jaks signed JV agreement with CPECC to develop JHDP. Later, Mr. Koon announced his entry after he accumulated more than 5% holding from open market. He cited the power plant as the sole reason for his investment in Jaks. In a short period of time, he aggressively upped his stakes in Jaks to over 30% and became the largest shareholder. The price continued to trend up to RM1.84.

Downtrend B started when a series of unpleasant news started to emerge.

- The RM50m bank guarantee claims by The Star for delay in Tower A of Pacific Star.

- The fight for board representation by Mr. Koon.

- Another 10% private placement

- Warrant right issue

- Mr. Koon facing margin calls

As seen on chart, there was huge volume of shares transacted at around RM0.50. Intense selling as a result of extreme pessimism caused by.

- The exit of Mr. Koon

- Severe undersubscription of warrants

- Loss of RM50m bank guarantee

- Award of huge RSP to executives in time of poor performance

The provision for the RM50m litigation loss took a toll on the Q4 2018 results but the share price reacted positively and continued to trend upward after the result announcement. Even another 10% private placement at RM0.70 did not stop the price from advancing to RM1.57. The close proximity of completion of the power plant was the only possible explanation for the uptrend.

However, the uptrend was interrupted by Covid19 and the construction of the power plant was forced to halt temporarily. Share prices fell across the globe and Jaks was no exception. Its price fell more than 50% to RM0.62. Yet another round of huge volume of transactions was seen.

Nevertheless, Jaks’ price made a quick recovery to RM1.17. Unfortunately, the share price took another beating when Jaks announced another right issue to raise a minimum of RM130m to subscribe for the final portion of its 30% stake in the power plant. This fund raising announcement is perhaps most disheartening to investors especially when it is done in the mist of Covid19. Judging from the gap down in opening price and the big transaction volume on the next trading day, many investors rushed to sell off on fear that Jaks’ price will eventually fall to RM0.40 as seen in the previous right issue.

What is next ?

Jaks has announced another right issue and investors have reacted negatively to the news causing the share price to gap down 13% on opening in the next trading day. Is the panic selling warranted ?

Jaks is asking for additional 20% (RM200 for every 1,000 shares) investment from the investors to subscribe for the 30% stakes in the power plant which will bring great fortune.

It is known that power plant projects require very large capital investments. Jaks Hai Duong power plant project is 75% financed by bank borrowings, the equity capital must be injected in order to drawdown the loan to the same proportionate ratio of 25:75. The loan drawdown is necessary to fund payments for construction of the power plant including Jaks’ EPC works.

This equity injection of USD30m is necessary for additional drawdown of USD180m bank loan. Future payments received by Jaks for its EPC works may be used to finance the 10% option subscription. I have provided a detail computation in the following article.

“Jaks Resources - Funding for the 10% option.”

https://klse.i3investor.com/blogs/Jaks%20resources/2020-05-29-story-h1507892408-Jaks_Resources_Funding_for_the_10_option.jsp

Jaks has rebounded slightly after severe selling pressure seen after the announcement of right issue. What will be the next price trend for Jaks ?

Two possibilities.

- Resumption of uptrend C, or

- Another leg down to RM0.40

- Jaks price was around RM1.50 in late February 2020 before Covid19 in anticipation of commissioning of the power plant. Therefore, present price level is comparatively very cheap at 40% discount to RM1.50.

- The right issue proposal promised at least 50% discount to TERP ensures that the price of Jaks must remain above RM1 during price fixing dates in order to fix the right share at RM0.40.

- The subscription of right shares coincides with the COD of Unit 1 in Q4 2020. The commissioning of power plant will be a major impetus to attract interests of investment funds.

- The current right issue made Jaks a disappointed and hated stock, most would have sold off and left. Those who remain will likely subscribe for the right shares.

- On 29 May 2020, CEO Ang Lam Poah bought 2m shares at RM0.885

- Unit 1 of the power plant will likely achieve synchronization by end June or early July, and commences trial run for 2 months during which Jaks will earn energy payment from EVN. I believe Jaks’ price will react positively to such news.

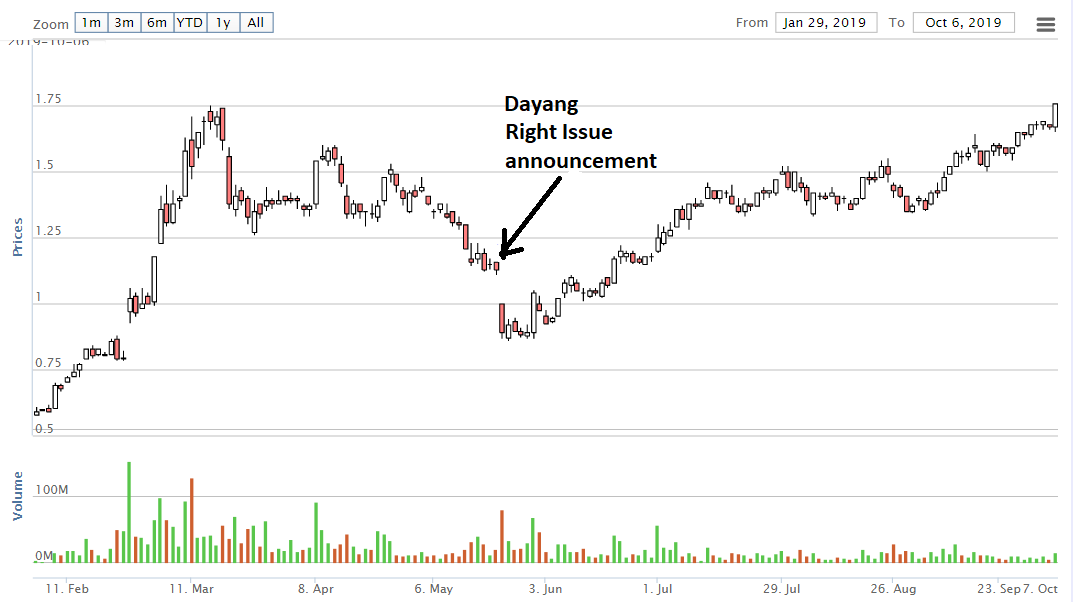

A reference to Dayang right issue

Dayang announced a right issue in 2019 with the same negative initial reaction to share price. Its price quickly recovered and resumed its uptrend seen in early 2019 due to the anticipated recovery in oil maintenance contracts which indeed materialized.

Jaks is anticipated to benefit greatly from its power plant which will commence operation in Q4 2020. Will this be the driving force to map Jaks' price trend similar to Dayang ?

For those who think Jaks will trend down to RM0.40, I have 2 questions for you.

- Will you buy Jaks at RM0.40 given that the power plant has achieved COD?

- Who do you think will sell to you at RM0.40 given that the power plant has achieved COD?

Conclusion

Things that we like may not be good and things that we do not like may actually be good. Jaks needs the right issue for the stakes in the power plant. The right issue is good for Jaks, but you may not like it. Think wisely, you are given a chance to buy more Jaks with free warrants at historical low price to lower your holding cost !

Thank you for reading.

DK66

https://klse.i3investor.com/blogs/Jaks%20resources/2020-06-08-story-h1508670915-Jaks_Resources_What_is_next.jsp