For better reading experience, please visit the original site:

HEXTAR (5151) – Getting Better and Better

Hextar Global Berhad (formerly known as Halex Holdings Berhad) has been in the agrochemical scene since 1990. Under the name Halex Holdings Sdn Bhd, the company had its public listing status on the Main Market of Bursa Malaysia Securities on 16th September 2009. Since it got public listed, Hextar’s business had been on a downhill due to many reasons which were explained in their annual report during the early days. From my point of view, the main reason their business was getting worse is due to their products just weren’t good enough back then, coupled with their weak branding (it was under the brand name Halex).

Throughout all these years, Hextar has been trying to restructure its business internally towards realigning the direction of the business to concentrate on its core business, which is the agrochemical business. This can be witnessed through the divestment of its property development business segment in 2017 and also the discontinuation of its horticulture segment in 2019.

The Pivotal Acquisition

After many years of subpar performance by the company, we started to see an improvement in its financial performance in 2019. This is after the acquisition of Hextar Chemicals Limited (HCL), which led to the change of company name from Halex Holdings Sdn Bhd to Hextar Global Berhad.

How did the acquisition of HCL manage to rejuvenate Hextar’s business to turnaround in a big way? First we will take a look into HCL:

HCL is an integrated agrochemical group which is involved in the entire supply chain of the agrochemical business from production, marketing, warehousing to R&D, product testing and product registration. HCL currently supplies its products to distributors and corporate plantation groups locally and exports to over 30 countries around the world. Being one of the largest manufacturers of pesticides in Malaysia, HCL’s strength lies in:

- Strong Branding worldwide

- Strong R&D and technical capabilities

- Strong market reach and expansion

Based on the past financial result of HCL (source: Circular to Shareholder pertaining to this acquisition), it is evident that HCL’s financial performance is significantly stronger than Hextar. Through the acquisition of HCL, Hextar is then able to:

- grow its revenue and customer base for its agrochemical business segment by tapping and leveraging on HCL’s close rapport with business networks and business associates in more than 30 countries worldwide

- penetrate into other selected foreign markets in Indochina which is predominately active in agriculture industry

- expand its existing product range and leverage on HCL’s R&D capabilities with the aim of providing value-added services to Hextar’s customers

- benefit from the economies of scale and operational synergies through, among others, optimisation of production processes and capacity, R&D activities, as well as procurement and administrative functions between Hextar and HCL.

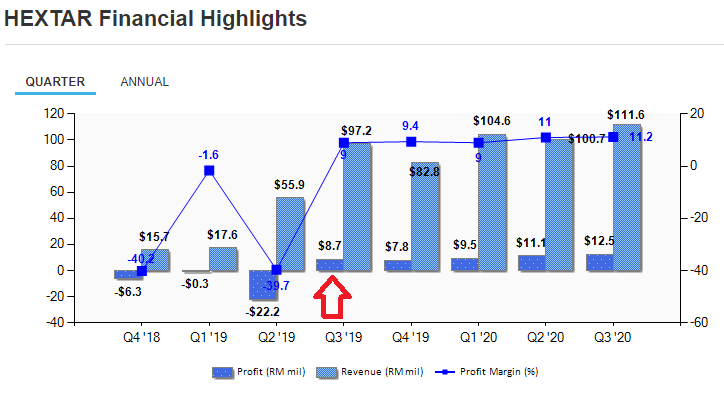

The acquisition has proven to be successful so far. This can be witnessed by the improvement in Hextar’s financial results from Q3 2019 onwards.

Favorable Market Environment

Since acquiring HCL, Hextar has been showing healthy profits every quarter for five consecutive quarters. Each quarter is showing a better record-high quarterly profit after tax than its immediate preceding quarter. All these happened amid the Covid19 pandemic, which caught me in surprise.

It turns out that Hextar business is fall within the essential service, as such they are able to continue their operations during the Movement Control Order period. Why does an agrochemical business is deemed essential? Well, due to the pandemic, the availability and security of food supply from crops are essentially needed than before.

Agriculture has always been important in developing countries, particularly the southeast Asia. This is because the agriculture industry plays a really important role in their economy and social development by providing employment, improving food security and reducing poverty. In addition, the growth of global population and rising income are also driving up food demand.

Therefore, to accelerate agriculture productivity on a sustainable basis to meet the increasing demand for secured food has always been a priority in these countries. Faced with growing food demand with limited agricultural land and other challenges, enhancing agricultural productivity through cost-effective methods like the application of improved use of fertilizers and pesticides become the most indispensable and effective solution to increase agricultural production.

As a leading crop management solutions provider domestically and strong presence globally, Hextar is well positioned to benefit from the ever growing demand for secured food. Already a market leader in Malaysia with an estimate market share of 30%, there is still ample potential for its business to grow domestically and globally.

This is why:

1) Malaysia and Indonesia Market

Indonesia is the largest producer of palm oil, followed by Malaysia with both countries account for 84% of the worlds palm oil production. There will always be demand for palm oil due to the vast usage of palm oil (refer to google on the widespread usage of palm oil). With the acquisition of HCL, Hextar has become the market leader in Malaysia. Early this year Hextar has accepted the tender award by Sime Darby Plantation Berhad (SDBP) for the supply of agrochemicals to SDBP in Malaysia, Papua Guinea and Solomon Islands. Through its strong local home brand name and wide range of specialised products for palm oil plantation, I foresee the company to secure more sales from the large pool of palm oil plantation companies in Malaysia.

Hextar is also a significant player in Indonesia due to its well established business network and business associates in Indonesia (through HCL). Indonesia has been actively carrying out their palm oil replanting program as currently there are at least 2.8 million hectares of land size in palm oil tree that aged over 25 years with bad quality seedings. According to Indonesia agriculture ministry’s Plantations Director – General Kasdi Subagyono, besides increasing the productivity and quality of fresh fruit brunches, the replanting program is also aimed to implement the good cultivation practices in order to meet the sustainability principles as required by the Indonesian Sustainable Palm Oil certification (source: Indonesia Palm Oil Association). This augurs well for Hextar as replanting program usually takes many years to implement, which provide a recurring income stream opportunity for Hextar.

2) Distribution Agreement with Sumitomo Chemical Vietnam Co. Ltd

Agriculture is one of the most important economic sectors in Vietnam. Besides to meet the growing domestic demand, Vietnam is always a major exporter of agriculture products. Their main crops production include rice, rubber, and coffee, which are important in our daily life.

Hextar has signed a Distribution Agreement with Sumitomo Chemical Vietnam (SCV) in October last year for the distribution of herbicide in Vietnam for a period of 5 years. SCV is part of Japan’s leading group of chemical companies, which is also a leading chemical group globally. This has opened the door way for Hextar to penetrate into the Vietnam’s market. I believe through its partnership with SCV, Hextar will also tap into SCV’s established network to penetrate into other potential markets.

Based on Hextar’s recent actions, I believe the management has their focus on Indochina now. This is wise as agriculture industry is still going strong in these Indochina countries.

3) Improvement in commodity prices

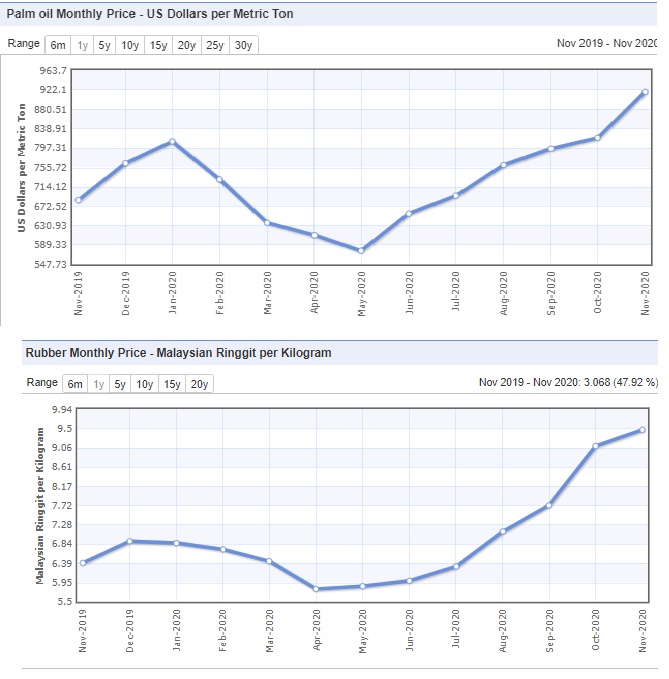

As seen from the graph above, the commodity price for Crude Palm Oil and Rubber have been increasing rapidly in 2020. A higher commodity price will give a better yield and return for the palm oil and rubber plantation companies. This will then entice them to increase their crop productions, which is done through the greater applications of agrochemicals. As the market leader in agrochemical industry, Hextar will be the biggest indirect beneficiary from the increase in commodity prices.

4) Timely venture into smart agriculture

We all know that technology is always improving and advancing at a fast pace. Malaysia government is also working its way towards digital transformation across the country and have identified 9 industries as the focus areas of Malaysia’s 5G technology. These 9 industries include agriculture, education, entertainment, healthcare, manufacturing, oil and gas, smart city, smart transportation and tourism.

In order to adapt to the 5G infrastructure which will arrive in a very near future, Hextar has started its venture into smart agriculture through partnership with overseas company with expertise in drones and smart unmanned aerial vehicle.

The advantages of agriculture drone spraying agrochemicals are: high pressure spraying, efficient use of chemicals, more uniform spraying and reducing the amount of pesticide wastage in water consumption. Furthermore, high-altitude spraying will make it easier to spray on the upper surface of the vegetation, to reduce personnel contamination and also wastages as well as promote safe agriculture practices (source: Hextar annual report).

This simply means the application of smart agriculture will help plantation companies to reduce operational cost, improve crop production yield, and improve crop quality.

The venture will include sales of equipment and the provision of services as well as consultancy services on the use of 5G technology to the plantation industry in an effort to drive cost efficiencies. This is synergistic to Hextar’s current business.

5) Biogas Green Business Venture

To further expand and compliment its core business, Hextar is also venturing into biogas green business through the acquisition of Biogas Engineering Sdn Bhd (BESB) and its subsidiary Biogas Environmental Engineering Sdn Bhd.

The liquid (POME) and gaseous waste that are generated during the extraction process of crude palm oil could cause environmental pollution as POME decomposition process releases a large amount of methane gas into the atmosphere. Disposing POME had always been a never-ending problem for palm oil mills not just in Malaysia but also for the rest of the regions.

BESB specialises in engineering design, technical research and construction of biogas processing system with over 20 years of experience in the industry. As a certified technology partner of Malaysian Palm Oil (MPO) Board, BESB is in collaboration with the MPO board on its biogas processing system to harvest and convert methane gas into green energy that can be used in generating electricity, burning boilers, or produce CNG and hydrogen. Currently, the system has been implemented in various sites in Malaysia an Indonesia

With the palm oil industry expanding further in Malaysia and Indonesia, BESB’s system will be well accepted as it will help in reducing environmental pollution and turn gaseous wastage into green energy for multi purpopses. Hence, the acquisition of BESB will allow Hextar to provide solutions to its existing customer base (palm oil millers) under its agrochemical business. In return, this will provide Hextar a new stream of income which bodes well with the palm oil industry in Malaysia and Indonesia.

Fundamental Analysis

Revenue

Due to the 100% equity acquisition of HCL which happened in April 2019, HCL’s financial results will also be incorporated into Hextar’s financial account. As such, we could see a huge jump of revenue in Q2 2019 onwards. Since the acquisition, the revenue has been improving every quarter which is excellent.

Profit Margins

In line with the increase in revenue, the gross profit margin and adjusted profit after tax margin are increasing too. This is probably due the economies of scale and operational synergies through, among others, optimisation of production processes and capacity, R&D activities, as well as procurement and administrative functions between Hextar and HCL which helped to bring down its cost of sale and operational cost.

Please take note that adjusted core PAT is used instead of normal PAT. In order to have a better picture of its business performance, I have made adjustments to remove the unrelated items such as foreign exchange gain/loss, impairments, gain/loss on disposal of assets, and so on which are not related to the core business of the company.

Earning per share (EPS)

Core EPS too has been increasing satisfactorily. Growth in EPS is one of the main catalysts to move the share price higher. As seen in the table above, the Core EPS of Hextar has been growing consistently due to increasing revenue with better profit margins.

Balance Sheet

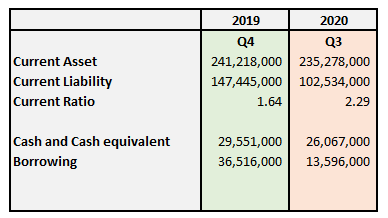

Comparing its balance sheet between Q3 2020 and Q4 2019, we could clearly see that its current ratio has improved to 2.29 from 1.64. Anything above 1.5 is acceptable, having it at 2.29 is even better. This shows that the management of the company is capable as they managed to improve the business without taking on more liabilities.

The management also managed to reduce its borrowing from RM36.5mil to RM13.6mil in less than a year time. This is due to healthy cash flow from its business, which was used to pay off part of its borrowing. The amount of cash balances is more than enough to cover its borrowing, so there is nothing to worry about.

Cash Flow

To compare how well the company has performed in its latest quarter, we will compare it with Q3 2018 and Q3 2019. From the table, we could clearly see that their operating cash flow management has been improving tremendously. Furthermore, their free cash flow is also improving handsomely, which explains how they managed to reduce their borrowings. If this keeps up, we could see Hextar becoming a zero borrowing company real soon.

The advantages with massive free cash flow are: Hextar could further consider merger & acquisition plans that will compliment its business, rewarding its shareholders with a higher dividend payout and expansion through investment into R&D and equipment.

PE Valuation

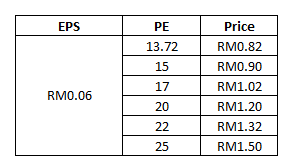

The total consideration amount (total purchase price) for Hextar to acquire HCL was RM596.79 million. The payment was settled through a combination of cash amounting to RM17.9 million and the issuance of 714.68 million new ordinary shares in Hextar at RM0.81 each. The price was determined based on HCL’s FY17, audited consolidated profit after tax of RM43.4 million which translates to a PE multiple of 13.72 times.

Since Hextar’s business is not affected by any seasonal events, we could use its recent results as a reference. The company managed to achieve an EPS of RM0.0154 during its latest quarter, if you calculate its actual core EPS you will get the adjusted core EPS of RM0.0166.

To be conservative, lets give it a 10% discount to its latest adjusted core EPS, which gives us an EPS of RM0.0150 (take note, in Q2 2020 the company has already achieved an EPS of RM0.0159 for its adjusted core EPS). Assuming the company will only achieve an EPS of RM0.015 every quarter for the next four quarters, which sums up to an annualized EPS of RM0.06.

Applying the benchmark PE multiple of 13.72 times, which was used to acquire HCL, we will then get the price of RM0.823. Well, as Hextar has been growing since the acquisition, the benchmark PE of 13.72 times should not be applicable anymore (personal opinion). Personally, I think Hextar deserves a higher PE multiple valuation due to its fast growing business which is well positioned to benefit from the future agriculture industry trend.

Therefore, PE multiple of 13.72 times should be used only as a benchmark. With the current status of Hextar, it is reasonable to assume a PE multiple in the range of 17-20 times. This gives us the target price range of RM1.02 to RM1.20. Bare in mind that my valuation is fairly conservative as it is based on the assumptions that for the next 4 quarters, there wont be any improvement in its financial results every quarter and the EPS of the next 4 quarters are fixed at RM0.015 every quarter, which is less than its Q3 2020 EPS amount.

This assumptions are made to give us a margin of safety in our valuation.

Technical Analysis

The stock has been gaining traction since May 2020, which could be observed through the inflow of volumes. This is what we observed through its latest daily chart:

- Trend Channel: Uptrend is still intact, as stock price is still moving within the trend channel

- MACD: Blue line has crossed below red line above zero, this means the uptrend momentum is decreasing

- RSI: RSI currently stands at 49, which is slightly below 50, this means the buying and selling pressure are on an almost equal ground.

- Stochastic: Stochastic is showing a trend reversal whereby blue line has crossed above red line at the zone below 20 and heading upwards. This means the stock has turned from downtrend to an uptrend. But take note, stochastic weighs much less than MACD in this particular case due to the trend of the stock.

- Moving Average: The price is below its 20-days moving average, which is a short term bearish sign. Mid to long term wise, the stock is still bullish as the price is standing well above its 70-days moving average and 200-days moving average.

Take note there is a small gap (highlighted in orange) in the chart which represents the price range of RM0.77-RM0.80. This price zone is important as it serves as a really important psychological support level. We should not see the price to drop and breach this level.

- Immediate Support 1: RM0.800

- Immediate Support 2: RM0.770

- Immediate Resistance 1: RM0.915

- Immediate Resistance 2: RM0.990

Risks

Apart from all the risks that have been repeatedly mentioned in their annual reports, there are a few risks which I think could impact Hextar’s business:

Regulation governing agrochemicals

The regulation and compliance governing agrochemical in Malaysia and also foreign countries might change from time to time in an unfavorable way for Hextar. As food security and quality are always improving, strict rules towards application of agrochemicals might affect Hextar’s ability to sell certain products or operate in foreign markets.

With proper policies in place, Hextar should be able to ensure continued compliance with all regulations and keep abreast of any change in the regulations in order to take the necessary actions to maintain compliance at all times.

Rise of organic farming

The rise of organic farming and food might also affect Hextar’s business. As more people accept organic food, more farming companies might choose to do organic farming instead (due to better margin as well) which decreases the demand for agrochemicals.

Although the acceptance of organic food is slowy increasing, it is still not on a significant level to affect the normal farming due to its much more expensive price level for end consumers. Therefore, in near future normal farming will still be the main and preferred choice.

Opinion

The acquisition of HCL was proven to be a pivotal decision which got the company to turn over a new leaf. Things are starting to look better now as Hextar is well positioned to take on the future trend of agrochemical business due to the 5 favorable market factors as mentioned above:

- Strong presence in Malaysia and Indonesia, which are the largest palm oil producers in the world

- Successfully penetrated into Vietnam market, a country which strongly relies on its agriculture industry

- Improvement in commodities prices such as Crude Palm Oil and Rubber which will further encourage the greater application of agrochemicals

- Timely venture into smart agriculture by staying proactive and take advantage in the future agriculture technologies

- Venture into Biogas green energy business which compliment its existing business as the world is also leading its way towards green and renewable energy

Hextar has another business segment – Consumer Products which I did not mention earlier. Apart from the agrochemical business, Hextar also manufacture and distribute healthcare disposal products such as wet wipes, tissue and cotton-based products. Due to its minimal profit contribution, I have chosen to omit it from my analysis. But it is worth mentioning that this segment has recently turned profitable for the first time this year. Due to the Covid19 pandemic, the demand for disposable healthcare products from the company has been increasing. I foresee this trend to continue due to the new normal caused by the pandemic. As such, I look forward to the profit contribution by its Consumer Products segment moving forward.

Trading companies are usually working on thin profit margins, but that is not the case for Hextar. With the average gross profit margin and net profit margin of 22% and 12% respectively, they are considered high! And the best part is, these margins could be improving in future due to the cost efficiency measure by the company.

Due to its excellent cash flow management, Hextar is able to reduce its borrowing from RM36.5 million to RM13.6million. Its healthy free cash flow trend shows the company is capable of generating good cash flow for its business. It is exciting to see how the management is going to utilize its cash moving forward.

As I have mentioned, the acquisition of HCL was done through the combination of cash amounting to RM17.9 million and the issuance of 714.68 million new ordinary shares in Hextar at RM0.81 each which translated to a PE multiple of 13.72 times. Based on my simple PE valuation, using the PE of 13.72 times gives us the price of RM0.82. On top of that, according to the chart of Hextar, the price level of RM0.80 serves as a strong psychology support which should not be breached. Combining these 3 factors, I conclude that the price level around RM0.80 is indeed a strong support level for its share price.

As we know HCL accepted the share issuance at RM0.81, anything below RM0.81 will then considered a loss for HCL. If you get what I mean…

From technical analysis, we could see that the stock is currently on its short term correction phase. I believe the uptrend in still intact. During 2017-2018, even though the company was still making losses, its share price once went to the high of RM1.10 (May 2017 & Jan 2018). It is obvious that Hextar is performing much better than before. As such, I believe the target price of RM1.10 is easily achievable. This is also align with my PE valuation (please refer above).

Although the potential for its agrochemical business is huge, there is still a long journey ahead for Hextar to reach its true potential. As such, we should invest in Hextar long term instead of short term. This is because business takes time to grow, and share price will grow along with its business.

Always invest at your own risk. Thank you

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

DISCLAIMER

This post is completely for education and discussion purpose only. The author of this post does not have the required licenses to provide any investment advice or induce any trade for the readers here. Therefore, it should not to be taken as investment advice or inducement to trade and the Author take no responsibility for any gains or losses as a result of reading the contents herein. Please invest at your own risk.

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

https://klse.i3investor.com/blogs/buycall/2020-12-26-story-h1538399389-HEXTAR_5151_Getting_Better_and_Better.jsp