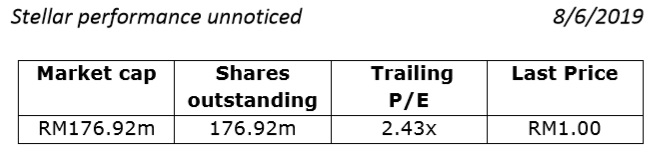

Circulating an article from SJ Securities on Crest Builder.

Corporate Profile

Crest Builder Holdings Berhad (CBHB) is a Malaysia-based company that

has strong footholds in the construction and property development

sectors. The group’s operation can generally be categorised under 4

different segments namely (i) Construction, (ii) Property Development,

(iii) Concession, as well as (iv) Investment Holdings. The group is also

a registered Class A Contractor with the Ministry of Entrepreneurial

Development and a Category G7 with the Construction Industry Development

Board (CIDB).

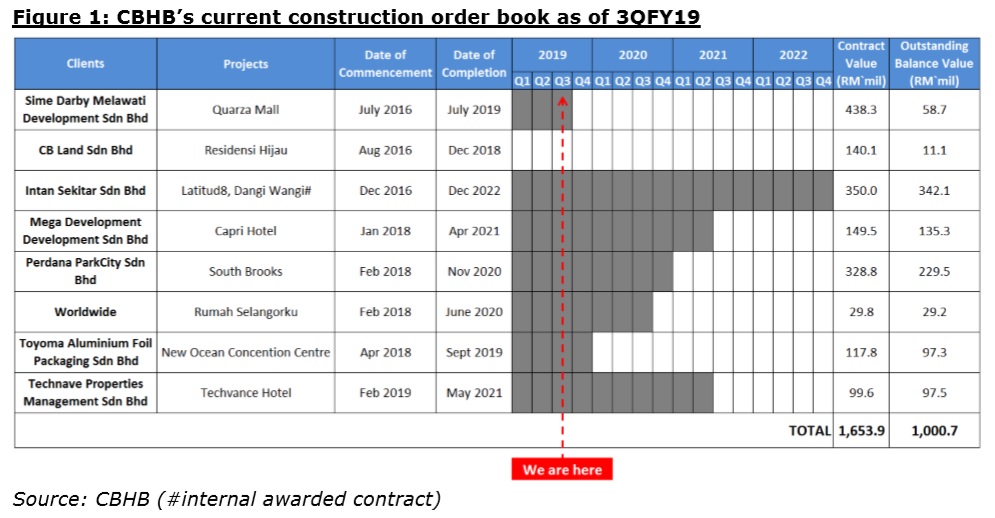

Abundant orderbook to sustain till 2021

CBHB’s outstanding construction order book stands at around RM1.0 bil,

which is expected to last until mid FY21. It has bagged RM100 mil worth

of construction jobs in 1HFY19, and is targeting to replenish its order

book by another RM500 mil worth of projects in 2HFY19. We are also

expecting faster recognition in progressive billing as most of its

existing projects have completed the initial stage and on track to the

higher stage with higher job claims. Another silver lining will be the

possible jobs winning from East Coast Rail Link (ECRL); the group had

submitted application to pre-qualify for ECRL’s civil work packages

earlier this year and we are guided by its management that it is

targeting to bid for station, depot, and building works.

Billion-dollar property projects in the pipeline

Among its ongoing property projects, we note that Alam Sanjung and The

Greens @ Subang West are fully taken up. With almost all projects being

fully taken up, we expect property division’s earnings to dip in FY19.

However, it has another two new developments namely Latitud8 (GDV: RM1.1

bil) and Elevat8 (GDV: RM1.33 bil) in the pipeline and on track to be

launched in FY20. We expect the two billion-dollar projects to be the

next earnings driver for property development from FY20 onwards.

Recurring income

Moreover, it has property investments in 2 corporate towers namely The

Crest and Tierra Crest that could collect rental incomes of about RM16

mil per annum. It also owns a 23-year BuildLease-Maintain-Transfer

concession agreement with the Ministry of Higher Education and

Universiti Teknologi Mara (UiTM) to build and maintain a campus in

Tapah, Perak, enabling it to derive recurring income of around RM43.5

mil annually until Jan 2034.

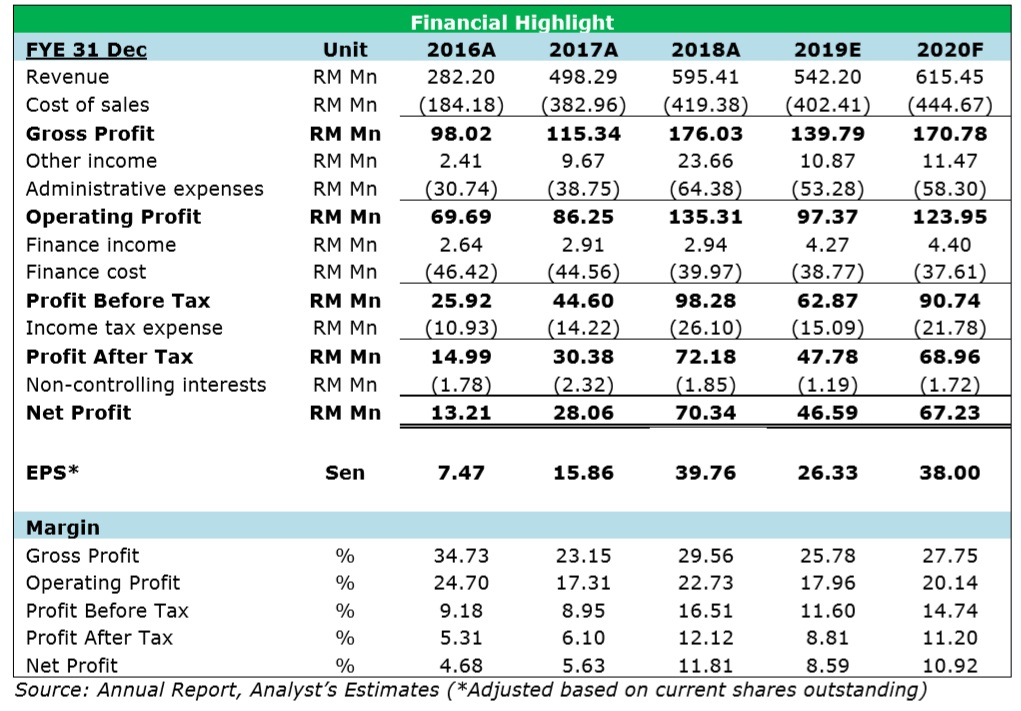

Financial Overview

CBHB’s 1QFY19 was resilience, with both revenue and net profit grew to

RM163.82 mil (+31.80% Y-o-Y) and (+31.33% Y-o-Y) on higher contribution

from both construction and property segments. Nevertheless, with lower

contribution from property development segment, we expect CBHB’s revenue

to slow down in FY19. Subsequently, we also anticipate lower net

earnings as we forecast a higher revenue contribution from the

construction segment which typically commands lower margins of around

7%-12%.

Meanwhile, CBHB is somewhat heavily leveraged with a net gearing ratio

of 0.72x. Dividend wise, despite not having a dividend policy, it has

been distributing at least 4.0 sen dividend during FY1518. It paid out

4.5 sen dividend for FY18, translating to a 4.37% dividend yield.

Valuations

Moving forward, we expect CBHB to continue its growth momentum

supported by abundant orderbook and exciting launches of property

projects. Despite recorded stellar performance over the years, CBHB

remains undervalued and unnoticed by investors as market’s interests

hava been diverted into construction companies with relatively greater

involvement in mega-projects (ECRL, LRT, etc.). On the other hand,

prolonged deferment of property projects could be another factor causing

investors’ avoidance. In light of the earnings visibility, we value

CBHB at RM1.62, based on SoP (Sum of Parts) valuation.

https://klse.i3investor.com/blogs/callmejholow/218703.jsp