Source: https://musingzebra.com/how-to-beat-the-efficient-market/

The stock market is like a pari-mutuel system of horse racing. Everybody goes there to make a bet and the odds change based on what’s being bet. Everyone can tell a quality company has better profitability, higher return on capital than a company with a terrible record. But when you look at the odds, the terrible record company has a 7 P/E and the quality company selling at 25 P/E, it becomes hard to determine which one is cheap. The odds make it hard to beat the market. The market is efficiently priced to a point.

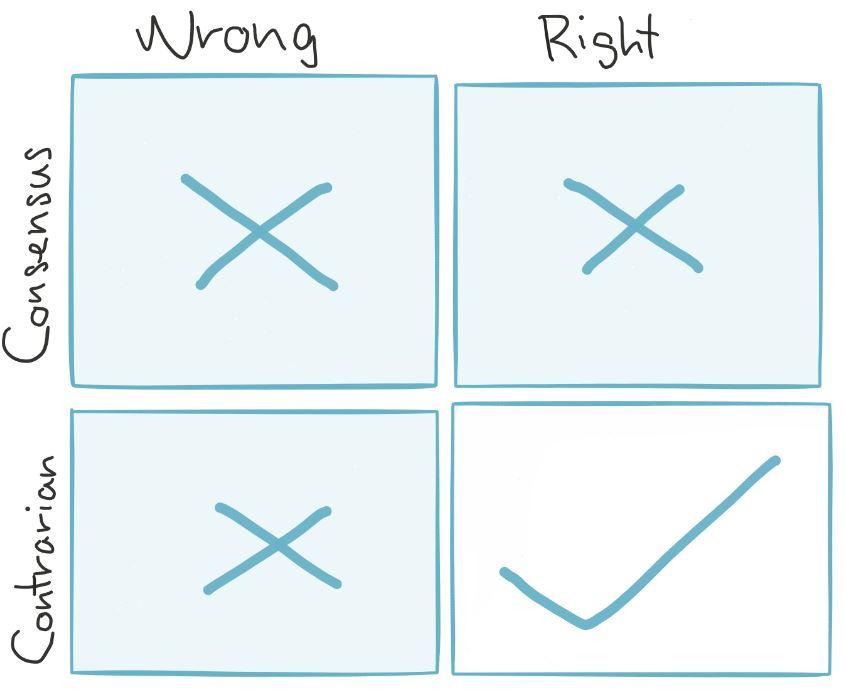

If you follow the market or have a consensus view, you only earn a market average return for being right. But that’s not the outcome you want as a stock picker. It is better to invest in index funds or passive ETF if achieving market returns is the financial goal. What you’re after is outperformance—above-average market returns. To do that, you’ve to be a contrarian.

To achieve outperformance one has to be a contrarian.

Contrarian means having a different view of the market. It doesn’t have to be the opposite; you don’t have to think the market has to go down. If the market is going up yet you think it is going to move in the other 99 directions, that makes you a contrarian. The essence of a contrarian is to think differently.

So how does one think differently to achieve long-term outperformance? There’s no universal formula. If there’s one, the consensus would adopt it until the odds ensure an average return over time. But here is something to think about. To beat the market, pay attention to the input. This can be expressed in an equation.

Input = Output

Process -> Results

Output, the results, is determined by what goes into the input. To change the output—from an average return to outperformance—you have to change the input. That is, what goes into the investment process.

Take stock screening tool as an example of input. Screeners are popular because it saves time. It’s efficient. But here’s the problem. Do you know anyone who doesn’t use a screening tool? Not many. Google stock screening, and there are 161 million results. Anyone armed with a screening tool sees what you see. What metrics do you use to screen stocks? Low P/E? High ROE? Price-to-FCF? Magic formula? Ben Graham Net-Net? The bad news is that hundreds of thousands of investors have culled through those criteria so many times that whatever is left are unlikely to be bargain anymore. Efficiency is a disadvantage when everyone wants to be efficient.

This concept applies to more than the screening tool. If your input is the same as everyone else, your output is not going to be that different from the rest. If you follow the market, read the same mainstream news, think in a similar fashion and use the same process as everyone else, it is hard to outperform in the long-term.

Imagine buying a house. You determine your budget (the price), the location, number of rooms, and so on down the priority list. But everyone else is using the same criteria to buy a house. Which means you're competing against the majority in a competitive market to look for value. How do you find value if you are looking at the same place as everybody is?

What if instead of an efficient tool like a screener, you do something inefficient? Like, go through every company starting from alphabet A to Z? That’s time-consuming. Who does that? That’s the point. No one is doing it. And that's where the potential outperformance comes from. There is no guarantee your time will be worthwhile. But there’s a higher chance of outperformance from an unconventional method than a conventional method like a screener. What about instead of using those popular metrics, you look for companies as measured by durability? Strong capital allocation skills? Companies that promote failure? Companies that have the highest employee satisfaction? That’s hard because there's no way to quantify these things. What about companies that no one would touch with a ten-foot pole? Again, it’s hard for psychological reasons. Not many people do it. But that’s how you beat the market. Outperformance comes from doing what others aren't willing to do.

If you ever look at the stocks owned by some famous investors, you’ll notice none of their portfolios look alike. Some have concentrated positions, others have a diverse portfolio; some hunt for special situations, deep value while others focused on franchise business or small caps. However, what’s interesting is not how different their portfolios are. Rather, it is the similarity that they all managed to beat the market over the long-term. These investors build their edge through originality—unconventional ways to find ideas and an investment process that can’t be easily replicated. They’re all contrarian in their own way.

Being original free you from all kinds of rules. You have the freedom to develop your own rules as long as they’re grounded on sound principles. How do you develop original ideas? For one, learn what surprises you. Read widely—most of what makes you a better investor lies outside of investing books. Cultivate second-level thinking. The more you read and think, the more ideas you gather. And the more ideas you have, the higher chance of connecting them in creative ways. Originality starts with making connections. Occasionally, some of these connections will turn into valuable insights that lead to outperformance.

In William Thorndike’s The Outsiders, he profiled eight unconventional CEOs on how they generated an extraordinary return by doing things that confound Wall Street. While the book is written more for CEOs and hedge fund managers than individual investors, it hits home an important message: To achieve exceptional performance, you have to play your own game, not rules of the game set by others. What's more, he discovered that while these CEOs all have their own unique, different approaches to their businesses, they all share a common trait—they’re independent thinkers.

https://klse.i3investor.com/blogs/JTYeo/222711.jsp